Editor’s Note

This article explores the rise of cultured diamonds, which are physically and chemically identical to their natural counterparts. As the industry gains formal recognition and standards evolve, these lab-grown gems are reshaping the luxury market.

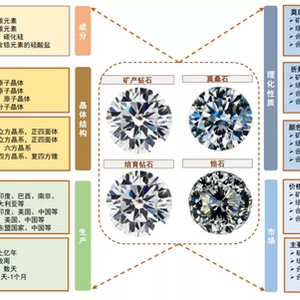

“Grown” real diamonds: the cultured diamond industry is rapidly rising. 1) Cultured diamonds are essentially identical to natural diamonds in physical and chemical properties: Cultured diamonds are crystals artificially created by simulating the natural diamond growth environment, sharing the same appearance, chemical composition, and crystal structure as natural diamonds. 2) Cultured diamonds have gained recognition from authoritative institutions: In 2020, GIA officially revised its grading standards, applying the same criteria to cultured and natural diamonds, solidifying the status of cultured diamonds as real diamonds. 3) Cultured diamonds possess strong fashion attributes and offer better value for money: Priced at 10,000-30,000 RMB per carat, only one-third the price of natural diamonds, with more controllable size, color, and shape, enabling customized and mass production to meet the fashion needs of young consumers.

Cultured diamonds are real diamonds, with physical and chemical properties identical to natural diamonds. Cultured diamonds are a new category of diamonds formed by artificially cultivating diamond crystal seeds under simulated natural diamond crystallization conditions. The high hardness, high density, and high dispersion of diamonds originate from billions of years under high temperature and high pressure deep within the earth. Cultured diamonds bring this formation process into the laboratory, using growth chambers to simulate the natural environment, “growing” diamond seeds into gem-quality diamonds as needed. Therefore, cultured diamonds, like natural diamonds, are real diamonds, distinct from diamond simulants like moissanite or cubic zirconia.

Cultured diamonds are a product of modern technological development. Unlike natural diamonds with a history of over three billion years, the first lab-grown diamond was created in 1953 by a Swedish electrical company using the High Pressure High Temperature (HPHT) method. Although only half a century old, rapid advancements in modern science have led to continuous breakthroughs in the yield and quality of cultured diamonds. Reviewing its development, it can be roughly divided into three stages:

With the new millennium, the rise of the global middle class brought changes in consumption concepts, driving the commercialization of Chemical Vapor Deposition (CVD) synthesis technology. Furthermore, actions by authoritative bodies, such as the establishment of the International Grown Diamond Association (IGDA) and the revision of definitions by the U.S. Federal Trade Commission (FTC), gradually standardized the cultured diamond industry. In 2020, the heavyweight GIA certificate officially revised its grading standards, no longer distinguishing between cultured and natural diamonds, marking a new era for the industry.

The primary technological paths for cultured diamonds are the HPHT (High Pressure High Temperature) method and the CVD (Chemical Vapor Deposition) method.

1) HPHT Method: Uses a small diamond as a seed, with graphite or diamond powder as the carbon source, adding a metal catalyst (transition metals like iron, cobalt, nickel) to reduce reaction conditions. A press provides high temperature and high pressure (1400°C+, 5.2-5.6 GPa) to simulate the natural diamond growth environment, forming an isometric crystal system.

2) CVD Method: Uses a small diamond as a seed. Methane (which already has a diamond structure) as the carbon source, hydrogen to inhibit graphite formation, and nitrogen to accelerate the reaction are introduced into a vacuum reaction chamber. Under high temperature and low pressure, an energy source (e.g., microwave beam) decomposes gas molecules to form a plasma cloud. Carbon atoms adsorb and precipitate onto a cooler, flat diamond seed plate, growing layer by layer to form an isometric crystal system.

The two technologies have their respective strengths. Generally, the HPHT method offers high efficiency and good color, while the CVD method allows for larger carat weights and superior clarity.

The value distribution in the industry chain follows a “smile curve.”

Domestic cultured diamond production primarily uses the HPHT method, largely because China has previously applied this technology to industrial diamond (diamond grit, powder, etc.) production, possessing a certain capacity foundation and technical advantage. Additionally, India, Europe, and the U.S. mainly use the CVD method and have established certain technical patent protections, with producers including Element Six and Washington Diamonds.

Midstream processing includes cutting, polishing, and other processes for loose diamonds, similar to natural diamond processing, hence they largely share processing lines. Currently, 95% of the world’s diamond processors are concentrated in India, with over 100,000 in Surat alone. Although regionally concentrated, the industry is highly fragmented due to the prevalence of small workshops and lacks motivation for consolidation; significant changes in the competitive landscape are not expected.

In recent years, brands have been vying to launch cultured diamond product lines and actively seeking cultured diamond supply. Key players include global traditional diamond giants like De Beers and Alrosa, famous jewelry brands like Swarovski and Pandora, and emerging cultured diamond brands like Diamond Foundry. The Asian market holds significant future potential. Domestically, Yuyuan Group launched its own cultured diamond brand LUSANT during the 2021 Qixi Festival. Additionally, emerging domestic independent brands like VDG Jewelry, CARAXY, and Light Mark are rapidly rising.

Overall, the cultured diamond industry’s profit margin exhibits a smile curve. Upstream rough diamond production has high technical barriers, and downstream diamond retail commands strong brand premiums; both enjoy significant profit shares in the entire chain. Midstream processors have lower technical content, a fragmented competitive landscape with severe homogenization, resulting in relatively thin profits.