Editor’s Note

This article references a selection of major listed companies across various sectors, including jewelry, apparel, cosmetics, and consumer goods. The list is provided for informational context and is not exhaustive. Stock tickers are included for clarity.

Chow Tai Fook (HK01929);

Lao Feng Xiang (600612.SH);

Shenzhou International (002563.SZ);

Hailan Home (600398.SH);

Shanghai Jahwa (600315.SH);

Jala Group (603605.SH);

Feiyada (000026.SZ);

Kweichow Moutai (600519.SH);

Wuliangye Yibin (000858.SZ), etc.

The luxury goods industry encompasses numerous finely segmented product categories. The competitive faction system in China’s luxury goods industry can be categorized by product type into high-end fashion, jewelry and accessories, watches, leather goods, cosmetics, tobacco and alcohol, etc. Among these, the jewelry and accessories market is mainly participated in by Chow Tai Fook, Lao Feng Xiang, Chow Sang Sang, etc.; the cosmetics market is mainly participated in by Jala Group, Shanghai Jahwa, Yumei Group, etc.; the white spirits market is mainly participated in by Kweichow Moutai, Wuliangye Yibin, Luzhou Laojiao, etc.

According to the “Global Powers of Luxury Goods 2022” report recently released by Deloitte, which announced the ranking of the top 100 global luxury goods companies for 2022, LVMH Group, Kering Group, and Richemont Group continued to occupy the top three positions. Others entering the top ten include Chanel, L’Oréal Luxe, LVMH (Note: likely a repetition; LVMH is already top), Hermès, Chow Tai Fook, Rolex, and China’s Chow Tai Seng. The headquarters of listed companies are mainly in Europe and the United States. China (including Hong Kong) has 11 companies on the list. Besides the two Chinese companies mentioned above, there are also Lao Feng Xiang, Chow Sang Sang, Chow Tai Sang, Luk Fook, Chow Tai Fook (Note: likely a repetition), Ming Jewellery, Fosun Group, Tse Sui Luen, and Carlier Group.

Chinese consumers are one of the main driving forces in the global luxury goods market. Data from Bain & Company’s “2023 China Luxury Market: The Year of Recovery and Transition” report shows that from 2011 to 2018, China’s luxury goods industry grew at a compound annual growth rate (CAGR) of 5%; from 2018 to 2021, it grew at a high-speed CAGR of 40%. Preliminary estimates indicate that after experiencing the dual challenges of an economic downturn and the repatriation of overseas consumption, the mainland China luxury market saw sales increase by approximately 12%, reaching 475.6 billion yuan.

In China, different luxury sectors have different competitive dynamics. However, overall, the brand market structure in each luxury sector has two major characteristics: First, brand concentration is relatively high; second, foreign brands occupy a large portion of the market share, while the development of domestic Chinese luxury brands is relatively slow.

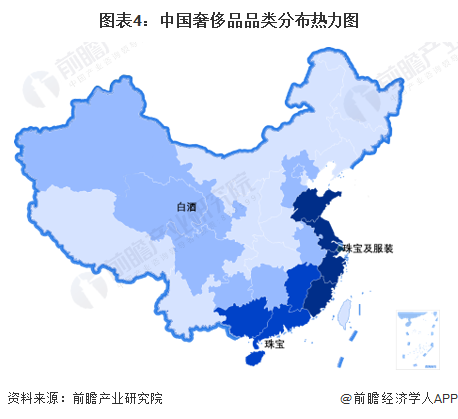

Regarding the Chinese market specifically, apart from traditional industries like white spirits, tobacco, and redwood furniture, China’s luxury goods market is dominated by foreign brands. Data from Bain’s statistics show that in various product categories of China’s luxury goods industry, the top five brands account for about half of the market share, most of which are foreign brands. Geographically, different categories of luxury goods form clusters in different provinces across the country. Overall, China’s eastern region has relatively strong luxury manufacturing capabilities. Correspondingly, it also possesses relatively strong capabilities in brand building, operation, and maintenance. China’s eastern region covers the manufacturing of luxury goods such as white spirits, jewelry, and high-end apparel. Specific participants include Yanghe Co., Ltd., Gujing Gongjiu; Chow Tai Fook, Lao Feng Xiang; Shenda, Shanghai Jahwa, etc. In contrast, participants in the luxury goods industry in China’s western and southwestern regions are mainly in the white spirits industry, with representative white spirits being Kweichow Moutai, followed by Wuliangye Yibin, Jiannanchun, Langjiu, etc. There are a small number of white spirits enterprises distributed in North China, but their products are mainly regional commercial goods and do not fall within the luxury category.

Observing the geographical distribution of Chinese luxury goods companies, listed companies in the luxury goods industry are mainly concentrated in East China and South China. These regions are not only economically developed with higher per capita income levels but also possess a large market scale and mature consumer culture, providing a solid foundation for the development of luxury goods companies. Besides East and South China, Central China also has a portion of luxury goods companies distributed. Although the quantity is relatively smaller compared to South China, the economic development and consumption upgrade in Central China are gradually revealing demand for luxury goods. With the sustained development of China’s economy and the advancement of regional balanced development strategies, it can be foreseen that the luxury goods market in Central China will gradually expand, attracting more corporate attention and investment.

Furthermore, according to Bain’s research, all luxury categories rebounded in 2023. Specifically, the cosmetics category grew steadily, with perfumes and color cosmetics showing particularly strong growth momentum; fashion, leather goods, and jewelry categories showed good recovery trends, with leather goods performing slightly weaker than the other two major categories; the watch category had the weakest recovery momentum, with varying performances among brands.

Analyzing China’s domestic luxury goods industry using Porter’s Five Forces model reveals that the domestic luxury goods growth environment currently faces relatively significant challenges. From the perspective of supplier bargaining power, China’s luxury goods industry has numerous raw material suppliers, resulting in relatively low supplier bargaining power. From the perspective of consumer bargaining power, the luxury goods industry generally has the characteristic of high pricing, and purchase frequency has a relatively strong impact on consumers’ bargaining power. From the perspective of the threat of new entrants, China’s domestic luxury goods industry is in a stage of rapid development. Taking the jewelry and accessories sector as an example, industry barriers are relatively low, with no significant technological added value, belonging to a labor-intensive industry. However, because the products themselves have relatively high value, if combined with excellent “brand narrative,” brand premium is easier to achieve, making the threat of potential entrants relatively high. From the perspective of the threat of substitutes, the threat of substitutes for China’s domestic luxury goods market is relatively the greatest. The main reason is that the domestic luxury goods market has long been led by foreign luxury brands. The consumption habits and perceptions of luxury consumers are subtly guided by foreign luxury brands in a latent shift. As substitutes, foreign luxury goods pose a relatively large threat to the domestic luxury goods market. From the perspective of competition among existing firms, currently, in various luxury product categories in China, there are a relatively large number of participants, making industry competition relatively fierce.

For more detailed industry research and analysis, please refer to the “China Luxury Goods Industry Market Outlook and Investment Strategy Planning Analysis Report” by the Forward Industry Research Institute.