Editor’s Note

This report highlights the projected growth of the global diamond jewelry market, driven by shifting consumer demographics and a rising emphasis on ethical sourcing. The enduring symbolic value of diamonds continues to resonate, particularly with younger generations.

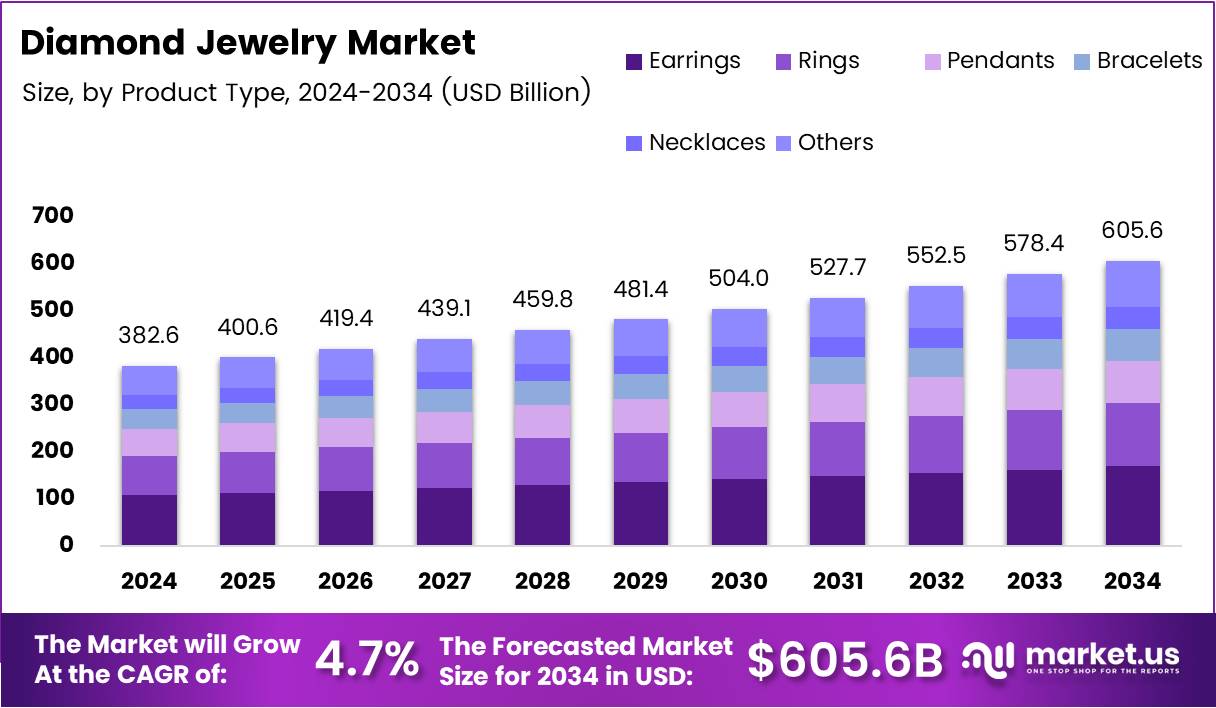

The Global Diamond Jewelry Market size is expected to be worth around USD 605.6 Billion by 2034, from USD 382.6 Billion in 2024, growing at a CAGR of 4.7% during the forecast period from 2025 to 2034.

The Diamond Jewelry Market is a segment within the broader luxury goods industry, driven by evolving consumer preferences and high emotional value. Known for symbolizing love, status, and tradition, diamond jewelry continues to attract attention from millennials and Gen Z. The rise in ethical sourcing and lab-grown alternatives has also reshaped this market.

The market has witnessed steady demand for engagement rings and high-end pieces. According to Brides, the average diamond carat weight for an engagement ring in the U.S. is about 1 carat, indicating continued consumer interest in classic, moderate-sized stones. This reflects purchasing patterns rooted in tradition and budget consciousness.

In recent years, lab-grown diamonds have surged in popularity. As reported by revediamonds, they are typically 30-40% cheaper than natural diamonds. This cost advantage appeals especially to younger buyers who prioritize both sustainability and value. As a result, lab-grown options are expanding the market’s customer base.

Meanwhile, luxury diamond jewelry continues to perform well. According to fox10tv, sales of high-end diamond jewelry in the U.S. remain strong in 2025, with overall jewelry sales increasing by 5.2%. This highlights consistent demand despite economic shifts and inflationary pressures.

Government involvement in regulating gemstone sourcing and trade compliance is increasing. Countries are focusing on ethical sourcing, traceability, and import/export duties, which impacts market entry strategies. These regulations aim to ensure transparency, boosting consumer confidence and promoting long-term sustainability in the diamond supply chain.

Investments in mining innovation, blockchain-based tracking, and synthetic diamond production are accelerating. Public and private sectors are collaborating to drive local manufacturing and reduce dependency on foreign supply chains. This move supports job creation and value chain efficiency in key regions such as India, the U.S., and Africa.

Consumer behavior is also shifting toward personalized and custom-designed jewelry. As disposable income rises, especially in emerging markets, customers are willing to invest more in meaningful and unique pieces. This change is opening opportunities for D2C (direct-to-consumer) diamond jewelry brands and online retailers.

The rise of omnichannel retailing has further pushed growth. Brands that blend digital convenience with offline luxury experiences are seeing improved conversions. Augmented reality (AR) and AI are being used to personalize buyer journeys, making the diamond jewelry shopping process more interactive and engaging.

The Global Diamond Jewelry Market is projected to reach USD 605.6 Billion by 2034, growing from USD 382.6 Billion in 2024 at a CAGR of 4.7%.

In 2024, Earrings led the product segment with a 43.2% market share, driven by their versatility and widespread demand.

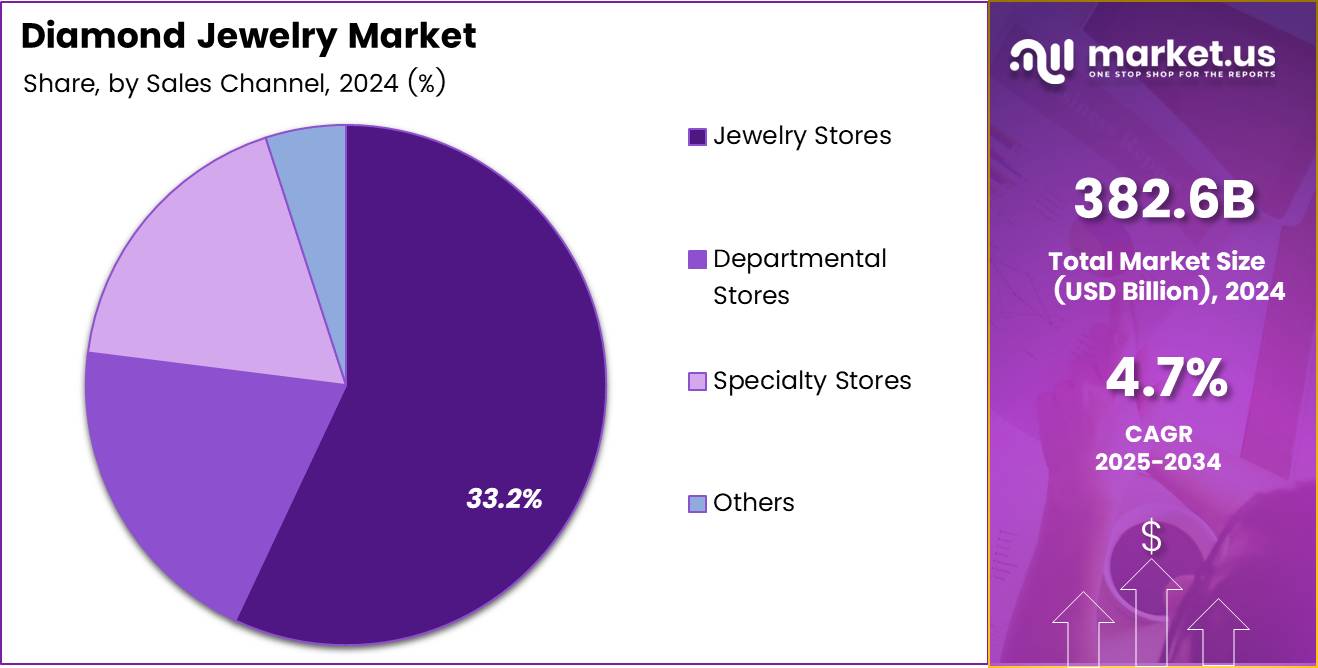

Jewelry Stores dominated the sales channel in 2024 with a 33.2% share, supported by in-store experiences and customer trust.

Women were the largest end-user group in 2024, holding a 61.3% share, influenced by cultural norms and self-purchasing trends.

North America led the regional market with a 44.2% share valued at USD 169.1 Billion, driven by high consumer spending and demand for luxury goods.

Earrings lead with 43.2% share, reflecting their popularity in daily and occasional wear.

In 2024, Earrings held a dominant market position in the By Product Type Analysis segment of the Diamond Jewelry Market, with a 43.2% share. This dominance is largely attributed to their versatility and high demand across age groups and regions, especially for gifting and fashion purposes.

Rings followed closely behind, maintaining significant popularity due to their symbolic value in engagements and weddings. Pendants continued to hold consumer interest as lightweight, everyday options.

Bracelets and Necklaces also showed a steady performance in the market, often marketed as statement pieces. Meanwhile, the ‘Others’ category encompassed a niche segment that includes innovative and custom-made jewelry, which caters to specific buyer preferences and emerging trends.

Jewelry Stores top with 33.2% share, proving their trusted role in luxury shopping.

In 2024, Jewelry Stores held a dominant market position in the By Sales Channel Analysis segment of the Diamond Jewelry Market, with a 33.2% share. Their continued success is driven by the in-store experience, trust in authenticity, and personalized customer service.

Departmental Stores also held a notable share, benefiting from their accessibility and product variety. Specialty Stores carved out a loyal customer base with tailored collections and design exclusivity.