Editor’s Note

This article outlines the projected growth of Africa’s diamond market, highlighting its significant reserves and key producing nations. The data provides a snapshot of the sector’s economic trajectory from 2024 to 2033.

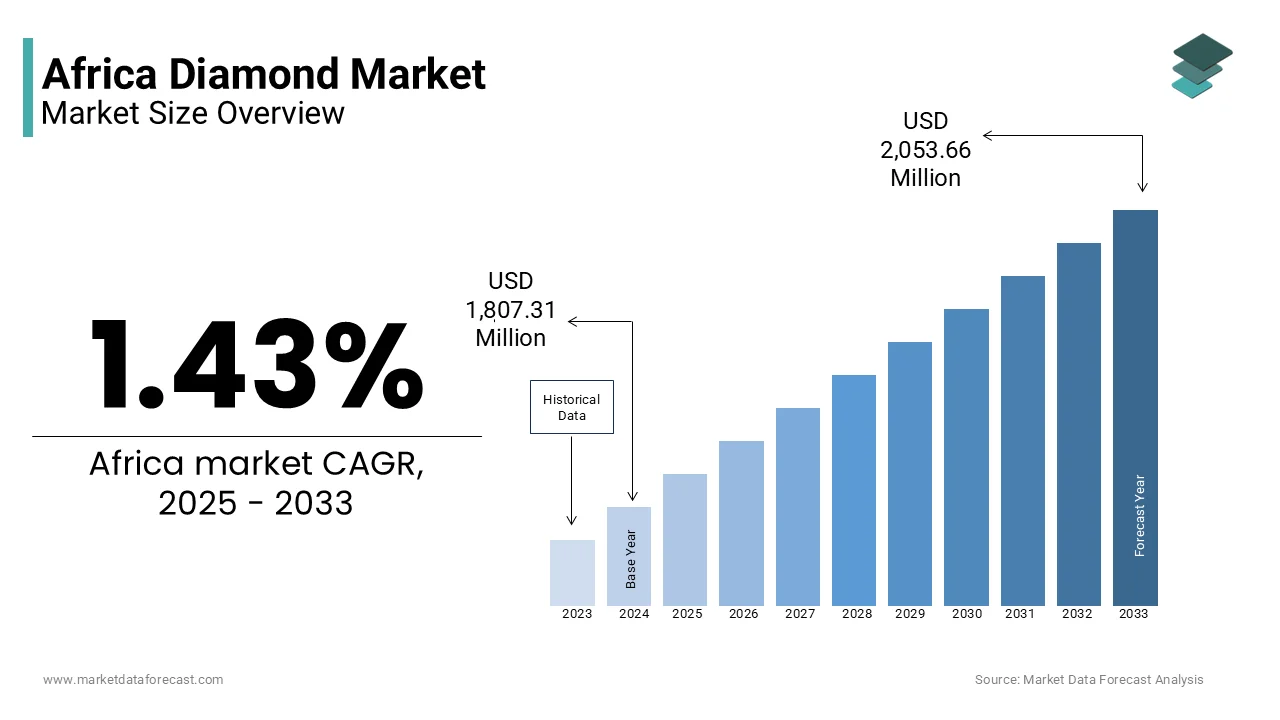

The Africa diamond market size was calculated to be USD 1.80 billion in 2024 and is anticipated to be worth USD 2.05 billion by 2033, from USD 1.83 billion in 2025, growing at a CAGR of 1.43% during the forecast period.

Diamond is one of the most historically significant and economically impactful segments of the global gemstone industry. The region is home to some of the world’s richest diamond reserves, with major production centers in countries such as Botswana, South Africa, Angola, Namibia, and the Democratic Republic of the Congo. These diamonds are primarily extracted through both large-scale industrial operations and smaller artisanal mining activities.

Africa contributes significantly to global diamond supply, with Botswana alone accounting for over a quarter of the world’s total diamond production by value. According to the Kimberley Process Certification Scheme, the continent supplied more than 50% of the world’s rough diamonds by volume in recent years. Despite this abundance, the industry has faced persistent challenges related to transparency, ethical sourcing, and economic equity distribution.

As per the African Union, the diamond sector supports millions of livelihoods across the continent, either directly through mining or indirectly via downstream industries such as cutting, polishing, and jewelry manufacturing. In addition, government revenues from diamond exports play a crucial role in national budgets, particularly for resource-dependent economies like Sierra Leone and Angola.

The market has also seen a shift toward traceability and sustainability, driven by increasing consumer awareness and international regulatory pressure. Initiatives like the Kimberley Process have been instrumental in curbing the trade in conflict diamonds, although gaps remain.

The growing global preference for ethically sourced and traceable diamonds is one of the key drivers of the Africa diamond market. Consumers, particularly in Western markets, are increasingly demanding transparency regarding the origin of their gemstones.

This trend has benefited African producers who adhere to international standards such as the Kimberley Process and the Extractive Industries Transparency Initiative (EITI). Countries like Botswana and Namibia have strengthened their reputations as responsible suppliers, attracting premium pricing and long-term contracts from major diamond buyers including De Beers and Alrosa.

Furthermore, advancements in blockchain technology have enabled greater traceability throughout the supply chain. Initiatives like De Beers’ Tracr platform allow for digital tracking of diamonds from mine to retail, reinforcing consumer confidence. This heightened emphasis on ethics and transparency is reshaping the Africa diamond market.

The growth of domestic jewelry manufacturing and retail industries, which are creating new avenues for diamond consumption within the continent, is an emerging driver of the Africa diamond market. Traditionally an exporter of raw diamonds, several African countries are now investing in downstream processing to add value before export. Local jewelers in Nigeria, Kenya, and Ghana are capitalizing on rising disposable incomes and a growing middle class that seeks luxury products reflecting cultural identity. This shift is supported by government policies promoting beneficiation—where raw materials are processed domestically rather than exported. Moreover, fashion and entertainment industries across Africa are influencing jewelry trends, integrating traditional motifs with contemporary designs.

Political instability remains a critical restraint on the Africa diamond market, particularly in regions where governance structures are weak or prone to disruption. Several diamond-rich nations, including the Central African Republic, the Democratic Republic of the Congo, and parts of Angola, have experienced recurrent civil unrest, corruption, and weak enforcement of mining laws.

These conditions create an environment conducive to illegal mining, smuggling, and exploitation, undermining formal market operations.

Apart from these, inconsistent regulatory frameworks and frequent policy shifts deter foreign investment in the sector.