Editor’s Note

This article highlights a notable divergence in the diamond market, with lab-grown diamond producers in China announcing price increases even as natural diamond prices face downward pressure. The trend underscores shifting dynamics within the global jewelry industry.

While the natural diamond giant De Beers just announced price cuts, Chinese lab-grown diamond manufacturers and retailers have begun collective price hikes. Recently, Huayan Jewelry announced that starting January 1, 2025, the price of large carat lab-grown diamonds will increase by 13%; Huanghe Whirlwind also issued a price increase notice, with a comprehensive increase of around 10%. Other domestic lab-grown diamond manufacturers have also generally released signals of price increases, driving a strong performance in related A-share sectors.

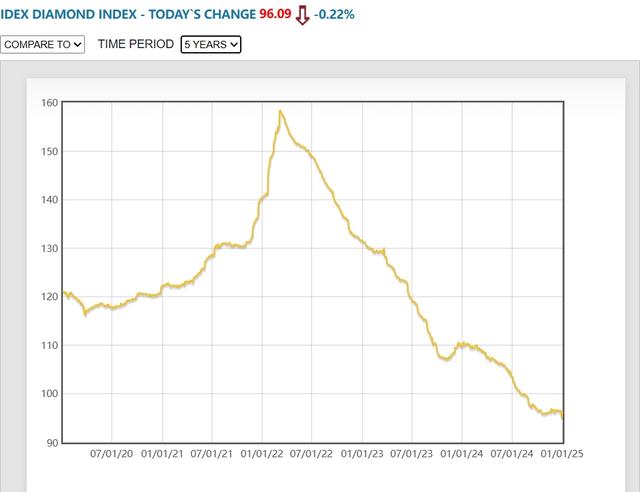

In stark contrast, in early December 2024, De Beers announced a comprehensive price cut of over 10% for diamonds. Against this backdrop, are lab-grown diamonds welcoming a new wave of popularity?

The backdrop of this round of price increases for domestic lab-grown diamonds is a previous long-term and substantial price decline. According to a September 2024 report by Meixin News, lab-grown diamond prices have fallen by nearly 90% over the past two years.

From an international perspective, the current price of lab-grown diamonds is only about one-twentieth that of natural diamonds. Lab-grown diamonds have captured the natural diamond market with low prices, benefiting a large number of consumers. Paul Zimnisky, a well-known international diamond industry analyst, stated that lab-grown diamonds already account for 20% of global diamond jewelry sales ($89 billion).

However, because the growth rate of market share is far outpaced by the rate of price decline, the profits of upstream enterprises are being severely eroded.

Taking the leading enterprise Liliang Diamond as an example, in the third quarter of 2024, the company’s net profit attributable to the parent company was 28.6596 million yuan, a year-on-year decrease of 68.39%. In comparison, at the peak performance in the second quarter of 2022, the company’s net profit attributable to the parent company once reached 138 million yuan.

In fact, judging from financial reports, the scale of the company’s lab-grown diamond business has still been growing since 2022. In 2022 and 2023, the operating costs of the company’s lab-grown diamond business were 80.64 million yuan and 107.71 million yuan respectively, accounting for 24.24% and 29.63% of the total operating costs. In the first half of 2024, operating costs were 69.71 million yuan, a year-on-year increase of 50.2%, with the proportion increasing to 31.75%.

Considering that the production cost of lab-grown diamonds themselves is unlikely to rise significantly, the increase in operating costs can, to some extent, reflect the growth in output.

However, the company’s revenue has not grown accordingly. The operating revenue of the lab-grown diamond business for the full year of 2022, 2023, and the first half of 2024 was 389 million yuan, 228 million yuan, and 166 million yuan respectively, with year-on-year growth rates of 97.12%, 41.46%, and 61.63%. Although 2024 showed a significant rebound compared to 2023, it has not yet recovered to the level of the same period in 2022.

Correspondingly, the gross profit margin level of the company’s lab-grown diamond business has already dropped from around 80% in 2021-2022 to around 50%.

Adding to the downturn in the industrial market, Liliang Diamond’s net profit attributable to the parent company has now fallen back to the level before the lab-grown diamond boom in 2020.

Overseas, the decline in lab-grown diamond prices has already led many companies into difficulties. In October 2023, WD Diamonds, the second-largest lab-grown diamond company in the United States, filed for bankruptcy protection; in August 2024, Lusix, a colored diamond company that had received a $90 million investment from LVMH, announced a debt of $27 million and sought debt reduction.

Recent active price increases by lab-grown diamond companies are undoubtedly good news for an industry that has been excessively “inwardly competitive,” but in the fierce market competition, how long the price increase can be sustained remains to be seen.

Some practitioners in the international market are not optimistic. Paul Zimnisky recently predicted that lab-grown diamond prices may still experience declines similar to those in 2023 in 2025, and 2023 was the year with the most severe price drops.

The website “Business Insider” quoted the view of Cormac Kinney, CEO of diamond trading company Diamond Standard, stating this. In his view, “The value of a timepiece will always only be a small part of the value of a real gemstone.”

In addition to substantial price declines and expanding production capacity, the technological route dispute within the lab-grown diamond industry may also pose potential risks to some companies.

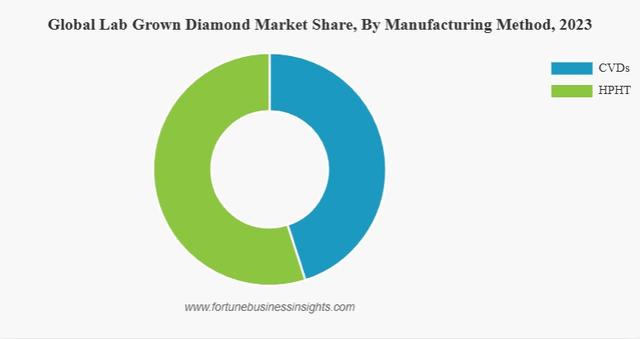

Lab-grown diamonds are mainly divided into two technological routes: HPHT (High Pressure High Temperature) and CVD (Chemical Vapor Deposition).

Currently, larger domestic lab-grown diamond companies, such as Zhongnan Diamond, Huanghe Whirlwind, Zhengzhou Huayan, and Liliang Diamond, mainly use HPHT technology, accounting for 80%-90% of domestic lab-grown diamond production capacity.

Companies like Zhengzhou Sino-Crystal, Shanghai Zhengshi, Hangzhou Chaoran, and Ningbo Lijing are mainly deploying CVD technology.

Internationally, lab-grown diamond production capacity is mainly CVD technology, with India, the United States, and Singapore being the main producing countries.

In terms of diamond quality, HPHT technology has better colorlessness, but the drawback is the difficulty in synthesizing large-sized diamonds; CVD technology produces diamonds with higher purity and larger sizes, but they are prone to carry color tones. Furthermore, because CVD technology requires smaller, lower-priced equipment and has faster synthesis speeds, it holds a certain advantage in cost.

Under conditions of extreme “inward competition,” cost may become a crucial competitive advantage. A report by the well-known consulting agency Fortune Business Insights shows that as of 2023, HPHT technology accounted for over half of the global market share, but due to CVD technology’s lower energy consumption and faster production time, it will show higher growth rates in the coming years.

This is not good news for domestic leading lab-grown diamond manufacturers and retailers. Huanghe Whirlwind mentioned in its 2024 interim report that since the second half of 2022, the company’s lab-grown diamond products have been impacted by new CVD lab-grown diamond products, with market sentiment continuing to decline, posing significant challenges to the company’s production management and sales management capabilities.

Moreover, as the production capacity of domestic CVD companies like Zhengzhou Sino-Crystal has not yet been fully released, the industry may face more intense competition in the future.

In addition to differences in product quality and cost, another challenge faced by HPHT technology lies in the discourse power competition in market promotion.

To maintain product prices, natural diamond producers have been trying to emphasize the distinction between natural and lab-grown diamonds in product identification methods. Although domestic regulations have generally recognized the status of lab-grown diamonds, diamonds produced by HPHT technology still have differences in some properties.

Because HPHT lab-grown diamonds absorb trace metal elements during the growth process, they possess magnetism and conductivity, which natural diamonds and CVD diamonds generally do not have. Therefore, some natural diamond and CVD diamond sales outlets use magnetic testing pens to distinguish HPHT diamonds, affecting consumer psychology.