Editor’s Note

This article outlines recent changes to China’s gold VAT policies, effective from November 2025. Key changes affect the tax treatment of physical gold withdrawals from the Shanghai Gold Exchange, depending on the purpose of the withdrawal.

The Ministry of Finance and State Taxation Administration of China recently announced changes to the gold market value-added tax (VAT) policies, effective from 1 November 2025 to 31 December 2027.

Members who buy and sell gold directly on the Shanghai Gold Exchange (SGE) – the so-called “first-tier” supply – remain VAT free. However, members withdrawing gold are now subject to different policies depending on their purpose: investment or non-investment.

Members withdrawing physical gold and re-selling with investment purposes are not impacted as they are still subject to the current VAT charge (at 13%) on the value-added part, while those with non-investment purposes now face higher costs when they re-distribute.

Clients who are registered with SGE members – also referred to as SGE clients – also face increased tax obligations when they withdraw gold from the SGE.

With higher costs, gold jewellery demand in China may face some headwinds; however, it may also be an additional catalyst for innovation amidst a competitive landscape.

Bar and coin demand is not directly impacted by the policy, but we may see greater concentration of gold buying through SGE members.

The Ministry of Finance and State Taxation Administration of China recently issued a few changes in the Chinese gold market tax policies, effective from 1 November 2025 to 31 December 2027. The changes are mainly related to the VAT system that is specific to the gold market. The last time there was a change in VAT that affected the gold market was back in April 2019, when VAT was lowered from 16% to 13% across the board.

The news came shortly after changes to taxation on platinum and diamonds, which also came into effect on 1 November. But the recent VAT policy change affecting the gold market is different.

To understand the changes, we need to take a step back and review the VAT policy in place until 31st October.

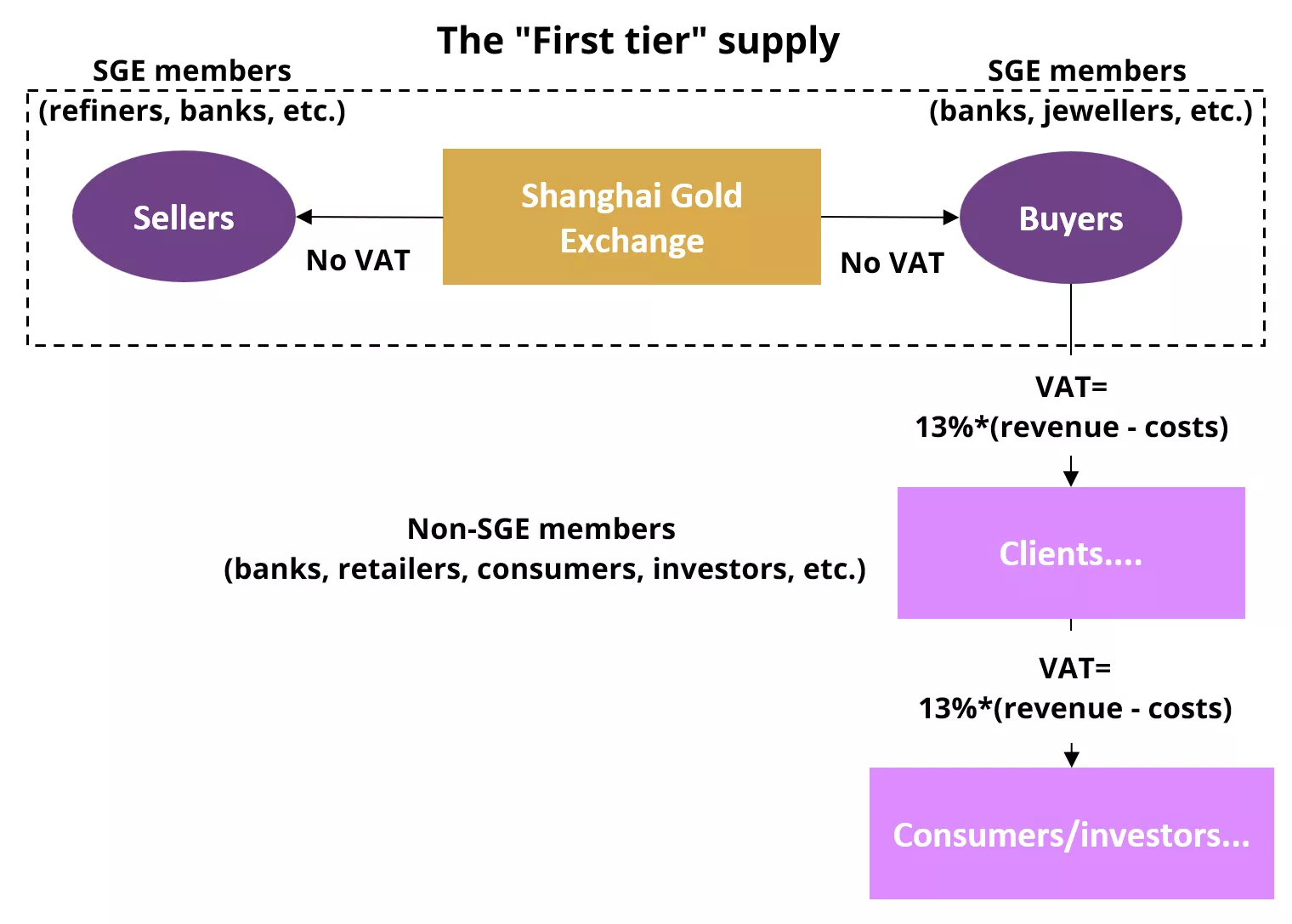

VAT is a circulation tax, meaning it is usually levied on the “value-added” part, or gross margin, at each point in the process of manufacturing, distributing and re-selling. We can break this down tier by tier:

- First tier: when SGE members/clients buy gold at the SGE from sellers, both the SGE and the purchasing members are basically exempt from VAT via the “immediate levy and refund” policy.

- Second tier: when SGE members/clients withdraw gold – to make it into branded investment products, or jewellery items – and re-sell, they pay VAT (at 13%) only on the value-added part (revenue minus costs), which is passed on to their clients.

- Third tier or further: when retailers buy these products from SGE members/clients and sell to consumers, they also pay VAT only on their value-added part, which they pass on to their customers.

The value-added part described for the second and third (and beyond) above is usually much smaller for investment products, which have low labour charges, than for jewellery products, where mark-up is determined by craftsmanship.

But now it is different. While SGE members that buy and sell gold on SGE in the “first tier” are still VAT exempt, the VAT treatment for members withdrawing gold is different, depending on their purposes.

SGE members who withdraw gold for investment purposes: The VAT treatment of SGE members who withdraw gold and re-sell it for investment purposes hasn’t changed. For example, if Bank A withdraws 1,000 yuan worth of gold from the SGE, which represents its cost, refines it into a branded bar and resells it at 1,050 yuan, which represents the sales price before VAT. In this case the applicable VAT is 13%* (1,050/1.13) – 13%* (1,000/1.13) = 5.8 yuan, raising the sale price after VAT to 1,055.8 yuan. This has not changed under the new tax reforms.

However, the input VAT tax deduction ends there. Here is what happens if Bank A sells the same product to a Client at the same price, and the Client sells this to a consumer at 1,100 yuan.

Interestingly, the tax increase would widen the differential between the purchase price of a jewellery piece (which will include VAT) and its buy-back price (which excludes VAT); this could in turn have a dimming effect on jewellery recycling.