Editor’s Note

APM Monaco, the Hong Kong-based jewelry brand, is reportedly considering a stake sale or IPO, with TPG aiming for a valuation of at least $2 billion. This move highlights the brand’s strategy to leverage current momentum in the jewelry market.

According to Bloomberg citing informed sources, Hong Kong-based jewelry brand APM Monaco is exploring options to sell a stake or pursue an initial public offering (IPO), drawing widespread attention in the capital markets. Investment firm TPG has hired advisors to advance both sale and IPO plans early next year. The sources added that TPG expects the company to achieve a valuation of at least $2 billion in a final transaction. APM currently operates approximately 500 stores globally.

In 2019, a consortium led by TPG acquired a 30% stake in APM. Other participants included the investment platform China Synergy, jointly established by TPG and CICC Capital, and the European private investment fund Trail Capital. In 2021, APM submitted IPO documents to Hong Kong regulators but ultimately did not proceed. Sources indicated the group also privately solicited interest from potential buyers but made no final decision.

TPG’s renewed push for an IPO exit may be eyeing the strong performance of jewelry brands in the Hong Kong stock market. Since its IPO in June 2024, Lao Pu Gold’s (老铺黄金) stock price has surged eightfold, propelling its market cap into the hundred-billion Hong Kong dollar club. This has not only caught investors’ attention but also established it as a dark horse in the global luxury market.

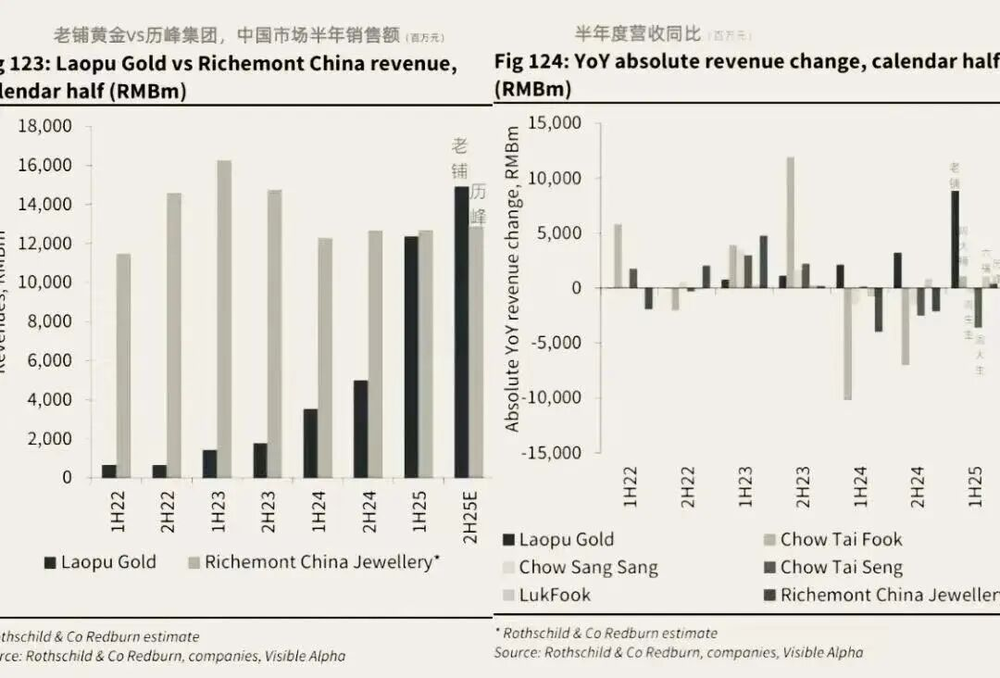

International financial institution Rothschild’s latest report points out that the Chinese domestic high-end gold brand Lao Pu Gold is projected to surpass Richemont’s jewelry business revenue in China for the first time in 2025. Considering Richemont’s portfolio includes top luxury brands like Cartier, Van Cleef & Arpels, Buccellati, Vacheron Constantin, and Montblanc, this outcome has garnered significant attention in the global luxury industry.

One challenge for APM’s listing is market skepticism about its heritage. Founded by Ariane Prette in 1982, APM started as an ODM (Original Design Manufacturer) providing design and production services for European jewelry retailers. In 1992, under the initiative of the founder’s son, Philippe Prette, production was moved to China. In 2012, APM officially launched its eponymous jewelry brand, focusing on youthful, accessible luxury jewelry.

Despite claiming Monaco origins, its headquarters are in Hong Kong, production is in China, and China is its largest market. In 2020, 57.2% of APM’s total revenue came from China, with other Asia-Pacific regions contributing 19%, and Europe and America only 23.8%.

Furthermore, APM’s silver jewelry is at a market disadvantage. Positioned as accessible luxury and seen as the next Pandora, silver is APM’s primary raw material. However, similar to Pandora, which has suffered significant losses in the Chinese market as consumer fatigue with fashion trends and silver’s lack of investment value set in, APM faces similar risks and has even higher dependence on the Chinese market.

Meanwhile, the jewelry market is not immune to the broader luxury sector’s polarization trend, where top-tier brands excel while mid-market and accessible luxury brands face pressure. APM, as an accessible luxury jewelry brand, lacks high-end value endorsement and struggles to maintain an advantage in the fast-fashion jewelry cycle, making its positioning awkward.

More complex is the emergence of distinct market trends in China in recent years. Under the “New Chinese Style” trend, consumers are re-embracing traditional aesthetics, perceiving a cultural gap with international brands. The ancient-method gold trend led by Lao Pu Gold has created widespread ripples. Chinese consumers’ longstanding preference for gold, coupled with the rise of ancient-method gold, is upgrading the entire gold jewelry industry.

In this environment, APM’s advantages in international and fashionable design are significantly weakened. Competitors like Missoma, Monica Vinader, and HEFANG are numerous, and requirements for product differentiation are continuously increasing.

According to its prospectus, APM’s revenue showed an upward trend from 2018 to 2020, recording HKD 1.44 billion, HKD 1.837 billion, and HKD 1.92 billion, respectively, with net profits of HKD 190 million, HKD 290 million, and HKD 152 million. The brand later disclosed that revenue growth slowed to 16% in 2023, with China’s contribution dropping to 55%. It currently has 230 stores in mainland China.

Notably, APM still retains its ODM business, which remains a stable income source for the group, contributing HKD 200 million in revenue in 2020.

The global jewelry market has transformed over the past five years, and APM needs a thorough self-review. To move to the next level, it may need to shed its ODM imprint. Transitioning from a product-driven to a brand-driven business for exponential growth requires sufficient determination to cut the safety rope behind it.