Editor’s Note

This article examines the complex dynamics between fraud prevention and transaction approval rates in Japan’s credit card industry. While enhanced security measures like EMV 3-D Secure are successfully reducing fraud, they can also impact authorization rates—a key metric for merchants. The piece highlights the ongoing challenge of balancing robust security with seamless customer experience.

While credit card fraud damage has significantly decreased, efforts to improve authorization rates are gaining attention. The Japan Credit Association recently announced that credit card fraud damage for the first half of 2025 was 31.46 billion yen, a 21.0% increase compared to the same period last year. Although the annual fraud damage amount is increasing, the April-June period saw a 10.7% decrease year-on-year. This is likely a result of the “EMV 3-D Secure (3D Secure 2.0)” system, whose implementation on e-commerce sites became virtually mandatory in April 2025.

On the other hand, it is said that after the mandatory implementation of “EMV 3-DS,” card companies have begun to lower authorization rates for individual merchants. It appears that an increasing number of e-commerce merchants are considering introducing fraud detection services to improve their authorization rates. There are also growing cases where payment gateway companies provide fraud detection services to merchants for free.

During interviews with e-commerce merchants, payment gateways, and fraud detection service vendors, multiple sources mentioned hearing that “card companies are lowering authorization rates for e-commerce merchants.”

The virtual mandatory implementation of “EMV 3-DS” has led to a decrease in fraudulent purchases. However, the liability for chargebacks that occur after passing the “EMV 3-DS” check has shifted from the merchant to the card company, a phenomenon known as “liability shift.”

As a result, for merchants with high fraud rates, card companies seem to be lowering authorization rates to avoid bearing the burden of chargebacks. When multiple card companies were interviewed, they declined to comment, stating, “We cannot disclose the details of individual merchant assessments.”

If authorization rates drop, even legitimate orders may be rejected. Cases where users cannot use credit card payments, leading to a decrease in sales, also appear to be increasing.

Merchants are now required to reduce the fraud rate on their e-commerce sites and build trust with card companies. To achieve this, introducing fraud detection tools to prevent fraudulent orders in advance is also effective.

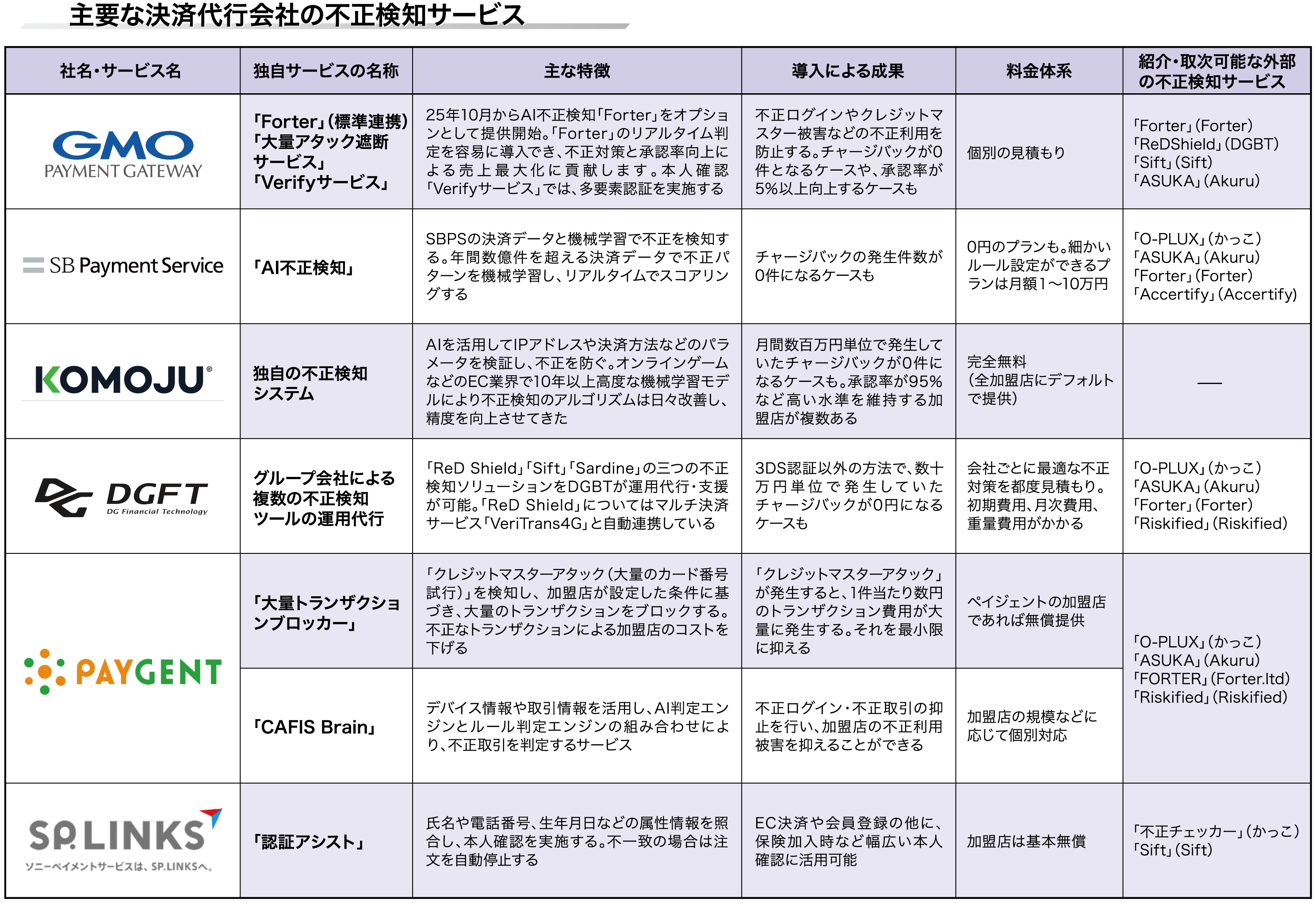

There are various fraud detection tools available, including AI-based ones like “Forter” and “Riskified,” and rule-based ones like “O-PLUX.”

There are also cases, like DEGICA’s “KOMOJU,” where fraud detection functionality is provided to merchants for free. This seems to be an attractive service for e-commerce businesses that want to improve their authorization rates while keeping costs down.