Editor’s Note

This analysis highlights a significant geographic shift in the luxury retail sector, identifying the Middle East—driven by the UAE and Saudi Arabia—as a new epicenter of growth and resilience amid global economic headwinds.

Luxury retail is undergoing a geographic reset. While global markets deal with macro slowdown, inflationary pressure, and shifting consumer priorities, the Middle East-particularly the UAE and Saudi Arabia-is emerging as the world’s most resilient and opportunity-rich luxury hub. The region’s rapid wealth creation, powerful tourism economy, large youth demographic, and cultural appetite for premium lifestyles have positioned the Gulf as the next strategic battleground for global luxury brands.

The outcome is clear: luxury is no longer just flowing eastward toward China-it is swinging southeast toward the Gulf.

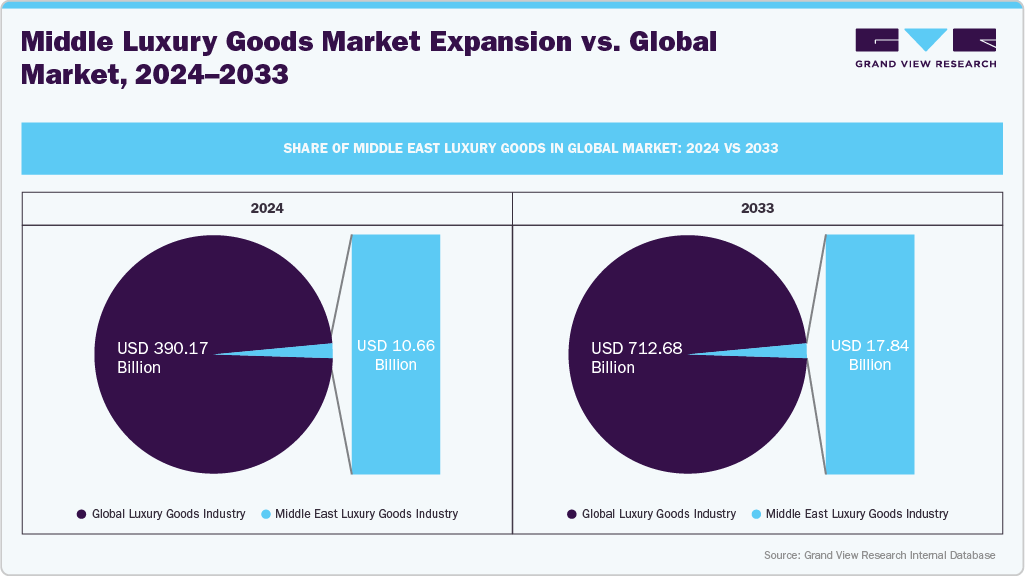

According to Grand View Research, the Middle East luxury goods market is expected to reach USD 10.66 billion by 2024. But this figure captures only the surface of a much larger transformation. Beneath the topline growth is a powerful shift reshaping the region’s luxury landscape-fueled by a surge in high-net-worth households, record-breaking tourism inflows, the rise of a young digital luxury consumer, and an accelerated appetite for premium fashion, fine jewelry, beauty, and lifestyle experiences. The Gulf is no longer just buying luxury; it is becoming one of the world’s most influential engines of luxury demand.

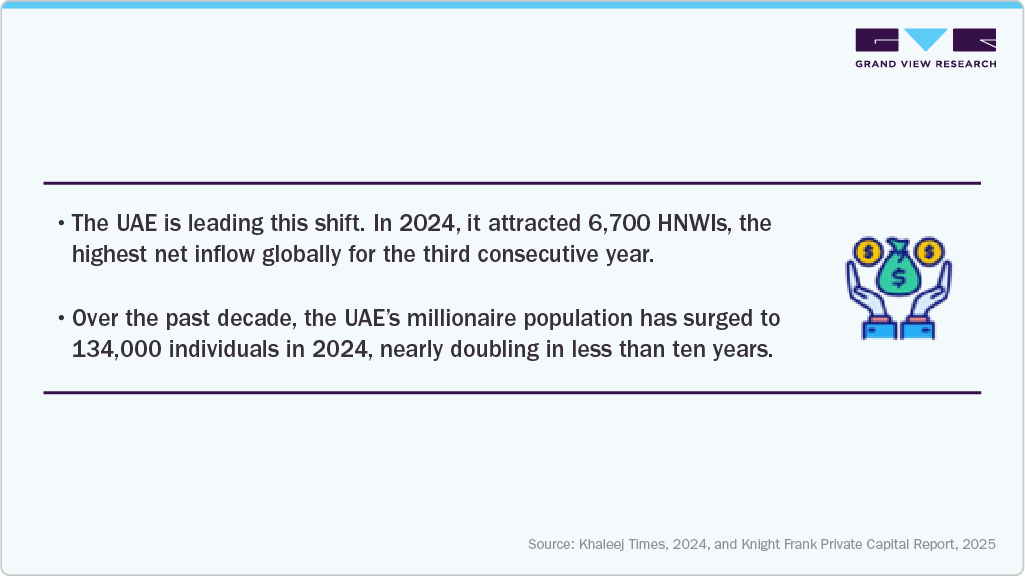

The most transformative force behind the Middle East’s luxury acceleration is the unprecedented growth in its high-net-worth and ultra-high-net-worth populations. Unlike most global markets-where millionaire migration has slowed or reversed-the Gulf is experiencing a net inflow of wealth at a scale unmatched anywhere in the world.

For brands, the implications are profound:

Consistent Demand Outperformance: HNWIs in the Gulf maintain luxury spending even during global downturns, making this region a hedge against volatility in China, Europe, and the U.S.

Higher Average Transaction Values: Shopping behaviors in the Middle East tend to skew toward high-ticket purchases, driven by gifting culture, event-driven buying, and a preference for premium and ultra-luxury SKUs.

Early Adoption of Flagship Concepts: Wealth concentration enables the successful launch of haute couture salons, private client programs, artisanal experiences, and high-jewelry exhibitions that may struggle in other regions.

Regional Influence on Global Trends: Gulf-based HNWIs are increasingly shaping global luxury demands through travel retail, personal shopping experiences in Europe, and cross-market spending patterns.

Tourism has become one of the most powerful accelerators of luxury retail in the Middle East, fundamentally reshaping demand dynamics across fashion, jewelry, beauty, and premium accessories. Dubai alone welcomed 17.15 million international visitors in 2023, positioning it among the world’s most visited luxury shopping destinations. Saudi Arabia is witnessing an even sharper rise, recording 30 million international arrivals in 2024 and surpassing 100 million total visitors ahead of its Vision 2030 timeline. This influx of global travelers directly translates into high-value retail spending, with Saudi Arabia generating SR 153.6 billion (US$41 billion) in inbound tourist expenditure in 2024. Tourism has now grown to contribute 11.5% of Saudi Arabia’s GDP, underscoring its strategic importance in the country’s non-oil diversification efforts.

For luxury brands, these tourism dynamics create a uniquely potent demand engine. High-spend international visitors-particularly from Europe, China, India, and affluent neighbouring Gulf countries-drive strong conversion rates for premium categories such as watches, fine jewelry, couture fashion, fragrances, and leather goods. Mega retail destinations like the Dubai Mall, which attracts over 100 million visitors annually, serve as global showcases and high-volume sales channels.