Editor’s Note

This article highlights a critical policy debate in India, as outlined in a recent SBI report. The central question—whether gold should be treated as a commodity or as a form of money—has significant implications for investment and economic strategy. The current focus on reducing demand may need to evolve toward frameworks that better harness gold’s potential financial value.

A report by the State Bank of India (SBI) states that India now needs a clear gold policy to determine whether gold is ultimately a commodity or money, and how consumers perceive it. Currently, India’s gold policy is primarily focused on reducing gold demand and recycling existing stock. The report explains that gold does not directly contribute to capital formation, but if monetized correctly, it could positively impact future investments.

The report says there is a significant difference in how the East and West view gold. In Western countries, gold is seen as public property. In contrast, in Eastern countries like India, Japan, Korea, and China, gold is still held as private property in homes, safes, and jewelry.

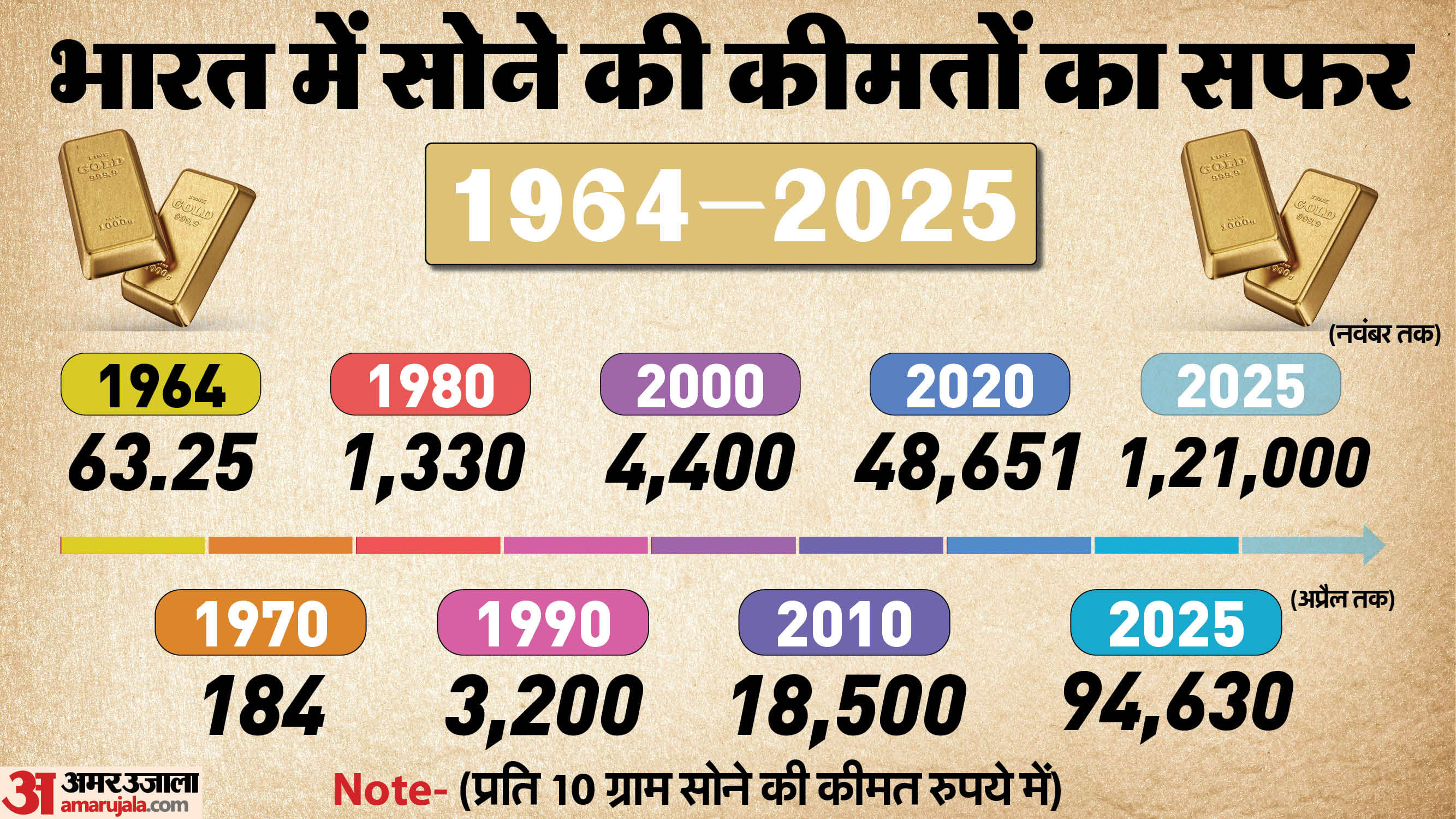

Gold prices in India have recorded a tremendous surge since independence. In 1947, gold was just 88 rupees per 10 grams, while now its price has reached about 1.24 lakh rupees. This is an increase of approximately 1,400 times.

Now consumers have started viewing gold not just as jewelry or coins, but as a better option for investment. Over time, new instruments like Sovereign Gold Bonds, Gold ETFs, Digital Gold, and Gold Mutual Funds have become popular instead of physical gold. These options are secure, offer tax benefits, and can be easily bought or sold when needed. This means gold is now not just a tradition for consumers, but a smart and easy investment.

Comparing India and China, SBI said that China’s central bank holds a reserve of about 2,300 tonnes of gold, while the Reserve Bank of India (RBI) has about 880 tonnes of gold.

China has a formal policy on gold, while in India’s case, no such clear policy exists.

In China, on average, every household has less than 10 grams of gold, with a target to reach 20 grams. In contrast, Indian households have an average of more than 25 grams of gold.

In China, domestic gold policy is linked to current account trends, while in India, policy is made as per need.

China has a clear direction on gold policy, even if it has not been made public, while in India, no formal policy has been formulated in this direction so far.

China’s commercial banks play an active role in almost every stage of gold production and supply chain. In India, the participation of the banking sector is limited; they are mainly confined to financing the gem and jewelry sector, exporters, and gold deposits.

The report states that China is the world’s largest gold producer, where testing facilities are rapidly developing. In contrast, India’s domestic gold production is limited. During FY 2025, 1,627 kilograms of gold were mined. However, recent reports from the Geological Survey of India (GSI) have indicated large gold reserves in Madhya Pradesh, Odisha, and Andhra Pradesh.

Additionally, China’s position is strong internationally as well. It is a member of the London Bullion Market Association (LBMA). India is not yet a member. Despite this, India is one of the world’s largest gold jewelry exporters.