Editor’s Note

This article examines the sharp rise in the U.S. average effective tariff rate, which has increased nearly eightfold since the start of 2025, according to data from the Yale University Budget Lab. The surge follows the implementation of new tariffs and retaliatory measures.

According to the Yale University Budget Lab, the U.S. average effective tariff rate was 2.4% as of January 2, 2025. This figure rose to 18.6% on August 7, when the retaliatory tariff surcharges were activated—a near eightfold increase.

This is, needless to say, the result of a series of Trump tariffs being levied, including sector-specific tariffs on items like automobiles (25%) and steel/aluminum (50%), as well as the 10% baseline tariff plus country-specific retaliatory surcharges.

Imposing tariffs on imported goods raises import prices. If companies pass on the increased procurement costs to retail prices, the inflation rate will rise. Higher retail prices lead to consumer reluctance to buy, suppressing consumption.

If companies do not pass on the costs and instead absorb the cost increases by reducing their own profit margins, corporate performance will deteriorate, potentially leading to hiring freezes or job cuts.

New tariffs are still to be imposed on sectors such as semiconductors and pharmaceuticals. Tariff rates are more likely to increase than decrease. Even if agreements are reached in tariff negotiations with major countries, the fact remains that tariffs have been raised, as seen in the effective rate mentioned at the outset.

Despite this, the markets, particularly the stock market, are optimistic. The S&P 500 and Nasdaq Composite indices, major U.S. stock indices, have hit record highs. Although the New York Dow closed below its December high of 45,014 dollars on the 15th, it briefly touched 45,203 dollars during the session, also setting a new intraday record.

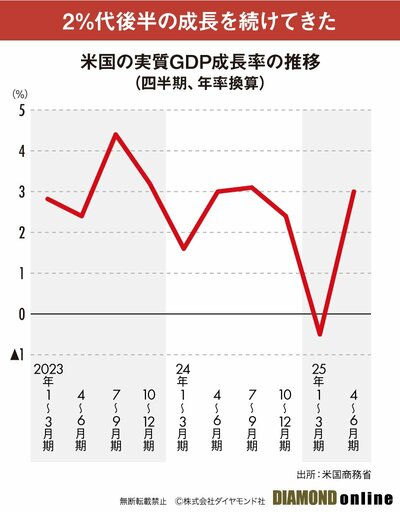

Looking at the trend in real GDP growth, the U.S. economy contracted at an annualized rate of 0.5% quarter-on-quarter in Q1 2025, falling into negative growth due to a surge in imports from pre-tariff front-loading demand (an increase in imports lowers the growth rate). However, partly due to a rebound from that, growth returned to around 3% in Q2 with a 3% increase, similar to levels seen in previous years.

However, the impact of Trump tariffs is beginning to show in employment. When the July employment statistics were released, the increases in non-farm payrolls for May and June were significantly revised downward.

While monthly gains exceeded 100,000 from January to April, they have since fallen below that level: 19,000 in May, 14,000 in June, and 73,000 in July. Employment has cooled since President Trump announced the introduction of retaliatory tariffs in April.

On the other hand, looking at inflation trends, the situation has not yet led to a sharp price surge due to tariff hikes. However, the rate of increase is gradually creeping upward.

The year-on-year increase rate for the overall Consumer Price Index bottomed out at 2.3% in April 2025 and rose to 2.7% by July. The year-on-year increase rate for the core index (excluding food and energy) remained at 2.8% from March to May before rising to 3.1% in July.

The Federal Reserve shifted to interest rate cuts starting in September 2024 but has kept the policy rate on hold since January 2025. While the Fed’s mandate is price stability and maximum employment, the market has largely priced in a resumption of rate cuts starting in September, in response to the cooling employment.

With the retaliatory tariff surcharges activated on August 7, the full impact of the tariffs is just beginning. To what extent will this affect the U.S. economy, prices, and monetary policy?

The Diamond editorial department conducted a survey of five U.S. economic experts on the outlook for the economy, prices, and monetary policy trends under the Trump tariffs.