Editor’s Note

This analysis of the global mining sector reveals an industry at a crossroads, navigating powerful structural shifts while managing persistent operational and social challenges. The divergence in company performance underscores that strategic adaptation is now the critical determinant of success.

The global mining industry is facing a scenario of profound transformation, driven by mega-trends such as urbanization, the energy transition, and technological evolution, while simultaneously confronting challenges of geographical concentration, price volatility, and new social and environmental demands, according to a study by the international consultancy PwC that analyzed the 2024 results of the world’s top 40 mining companies.

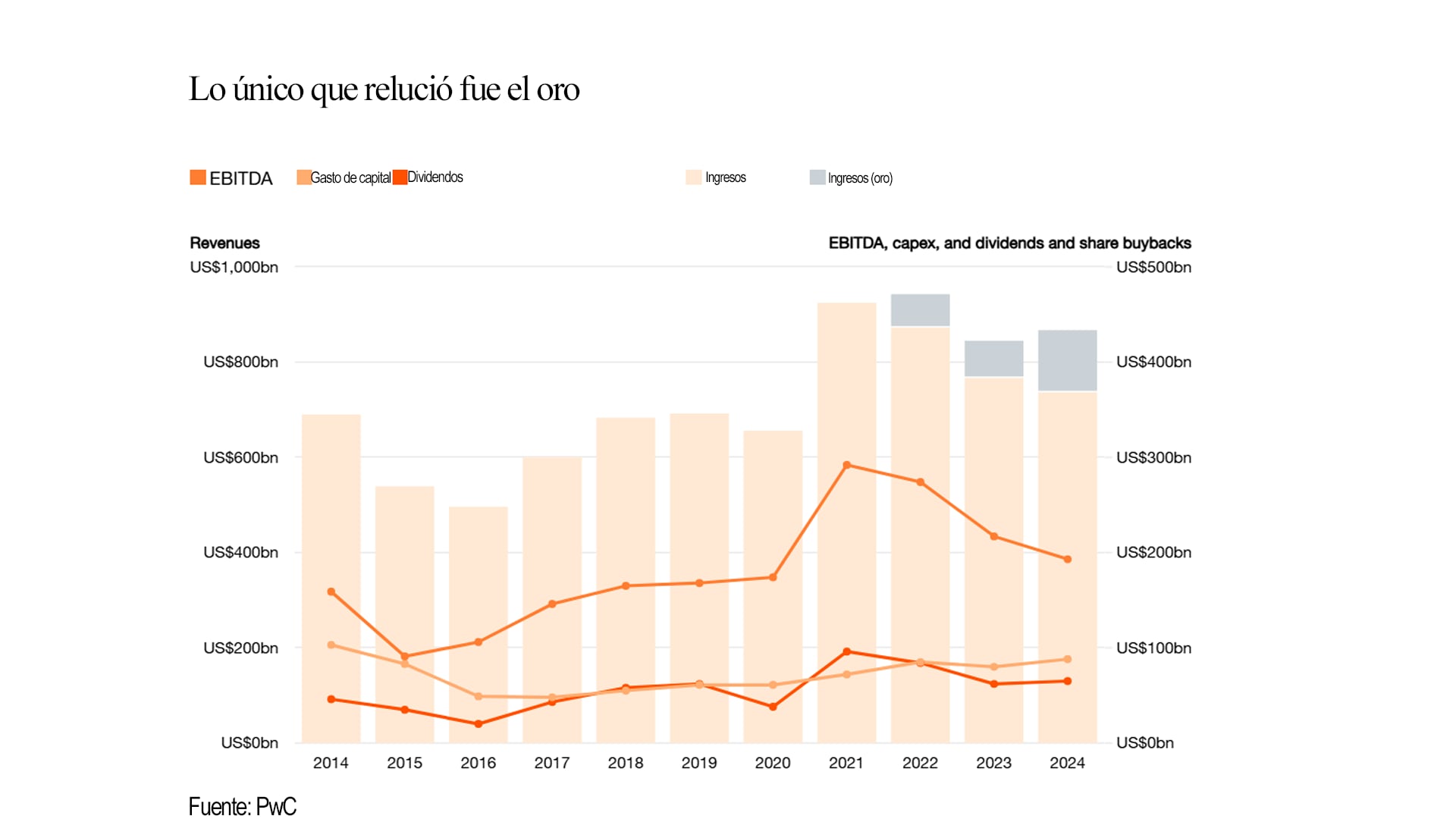

A basic finding of the study, which involved mining experts from the consultancy across all regions of the world, is that in such an environment and excluding those dedicated to gold, miners saw their revenues fall by 3% and their EBITDA (earnings before interest, taxes, depreciation, and amortization) fall by 10%.

In fact, the average EBITDA margin for non-gold miners fell from 24% in 2023 to 22% last year. Meanwhile, gold miners benefited from record precious metal prices, with their revenues growing 15% and their EBITDA improving by 32% “thanks to operational leverage.”

The report clearly shows this divergence: by distinguishing the revenues of miners between gold and non-gold for the years 2022 to 2024, it shows that while for the former EBITDA grew steadily, from about USD 40 billion in 2022 to nearly USD 100 billion in 2023, that of other miners fell from nearly USD 450 billion in 2022 to about USD 370 billion in 2024.

The study analyzed global mining based on the “Domains” or uses of different minerals: what things are produced (Make) or built (Build) with them, their contribution or not to mobility (Move), energy generation (Fuel & Power), food (Feed), and care (Care).

Each of these domains, it says, depends on products extracted from the earth, whose demand varies according to transformations in the global economy. The geographical concentration of mineral reserves and production adds a layer of complexity: some countries dominate the supply of critical resources, creating risks and opportunities in the configuration of new supply chains and national strategies.

For example, it highlights that in the energy “domain,” despite the growth of renewable sources, coal represented 35% of electricity generated in 2024, while nuclear energy, dependent on uranium, contributed 10%.

Furthermore, mining provides essential minerals for renewable energy storage and transmission technologies. In mobility, platinum group metals (PGMs) have been key in reducing combustion engine emissions, but their prominence could decline as transportation electrifies. On the other hand, demand for lithium, cobalt, phosphate, nickel, and manganese has increased with the development of batteries for electric vehicles.

Food also depends on mining. Population growth and urbanization increase the demand for fertilizers; phosphate is essential for producing phosphorus-based fertilizers, fundamental for cereal and vegetable crops. Potassium salts, for their part, improve drought resistance and are vital for crops such as wheat, corn, soybeans, and rice.

In health, mining contributes much more than gold and silver for dental fillings. Titanium, cobalt, PGMs, and nickel are used to manufacture surgical tools, implants, prosthetics, and medical equipment. Uranium is crucial for the production of medical radioisotopes used in imaging equipment such as MRI and CT scanners.

Urban construction requires steel (from iron ore, manganese, and metallurgical coal), copper, aluminum, zinc, tin, and nickel. Aggregates such as lime for cement, stone, clay, and sand are essential in infrastructure like roads, bridges, and buildings. In manufacturing, almost all goods contain mining inputs: gold is used in luxury jewelry, stainless steel in appliances and industrial machinery, and various metals are used to manufacture airplanes, space technology, and defense systems.

Some minerals have a single “domain,” while others, such as iron and –even more so– copper, are multidimensional, as they are applied in all possible areas.

Another warning is that in a geopolitically turbulent world, the “risk of concentration” is increasing, associated with natural or human factors that cause the supply of certain minerals to depend on one country or a handful of countries.

In this regard, PwC specifies that China is responsible for more than 50% of the production of 18 minerals and holds more than 10% of the reserves of another 35. It is followed by the United States, which produces more than 50% of 7 and has more than 10% of the reserves of another 12. The processing of many minerals is also concentrated in China, even in those where it is not the main producer.

An extreme case is that of rare earths, in which the Asian giant holds 69% of production and 92% of processing, giving it enormous bargaining power, as evidenced in the conflict over the “reciprocal tariffs” announced by Donald Trump on April 2. Two days later, China initiated a system of controls and permits for the export of 7 of those 17 elements and published a “control list” of 15 companies to which it would not supply rare earths, 14 of which were U.S. defense and security sector companies.