Editor’s Note

This article highlights a significant growth trajectory for the global jewelry manufacturing and precious metal processing equipment market, projected to nearly double in value over the next decade. The data underscores a robust and expanding sector driven by technological advancement and sustained demand.

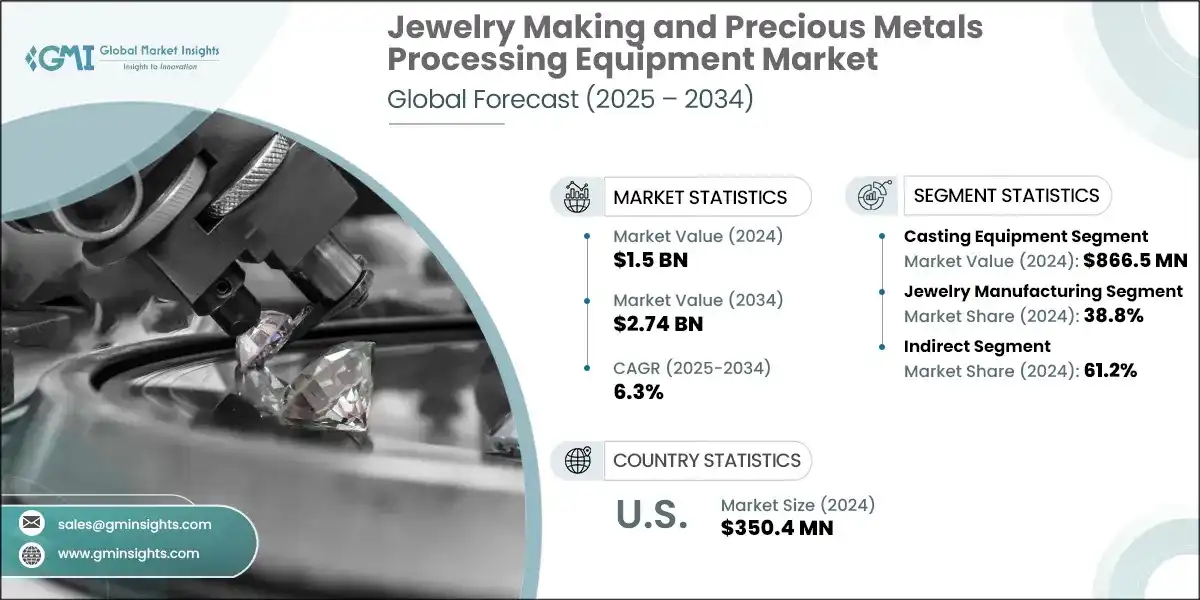

According to a recent study by a global market intelligence firm, the global jewelry manufacturing and precious metal processing equipment market was valued at USD 1.5 billion in 2024. The market is projected to grow from USD 1.57 billion in 2025 to USD 2.74 billion by 2034, representing a compound annual growth rate (CAGR) of 6.3%.

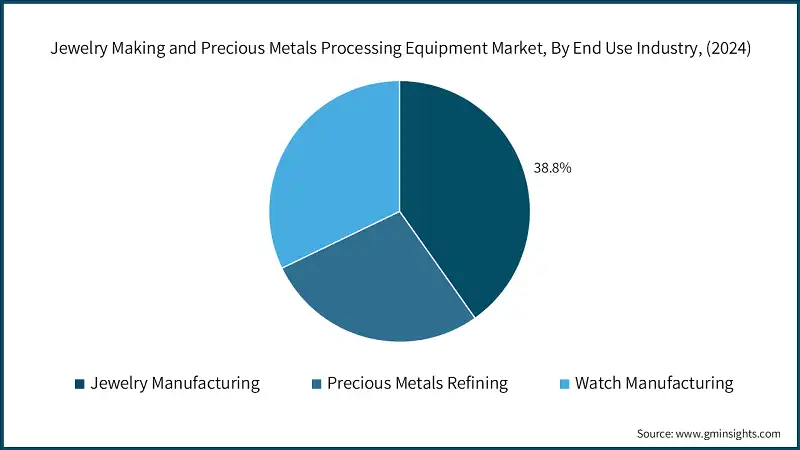

The precious metal processing equipment and jewelry manufacturing sectors are experiencing rapid growth due to several factors. The most significant driver is the increasing demand for high-quality and personalized jewelry. Individuals, particularly younger users and affluent members in developed and emerging economies, increasingly prefer accessories that reflect their identity, lifestyle, or culture. There is a growing need for small-scale production with high precision, leading manufacturers to adopt advanced technologies for accurate designs.

Advanced technologies such as laser cutting and vacuum casting for CNC machining enhance manufacturing, minimizing material waste to the greatest extent. As manufacturing speeds increase, product quality also improves. Automation and computer-aided design software like CAD/CAM programs, along with 3D printing technology, have seen improvements with faster prototyping and product customization. These technologies help reduce labor costs and enable designers to create complex designs with consistent quality.

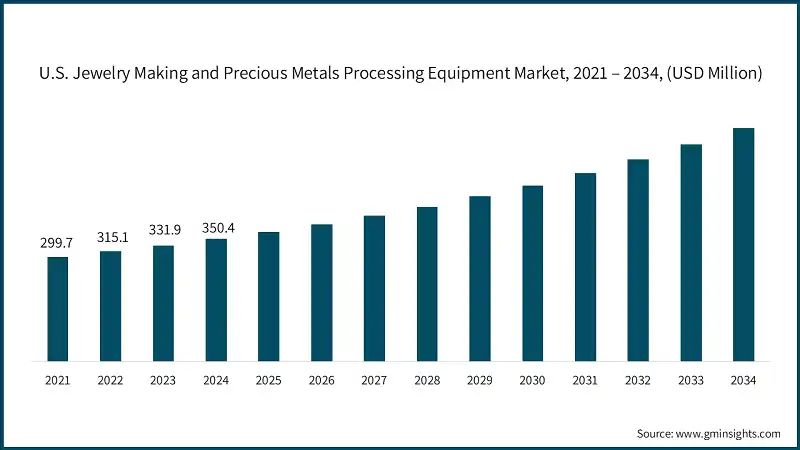

The Asia-Pacific (APAC) region leads the market, driven by its strong manufacturing base, highly efficient human resources, and high demand from domestic and international markets. India, China, and Thailand are renowned for producing large quantities of jewelry and bracelets. The region benefits from low labor costs, government incentives for investment, and cultural values favorable to jewelry expenditure.

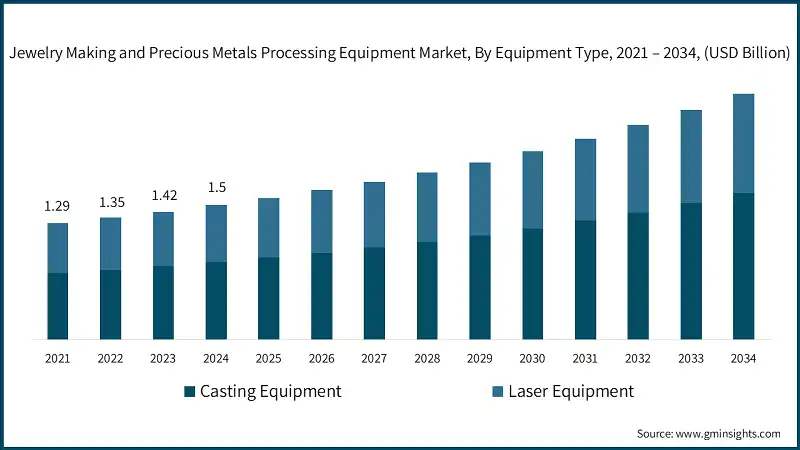

Casting machinery is the most widely used technology as it is the core of jewelry production. Casting enables manufacturers to produce complex designs at low cost and high volume, making it suitable for both commercial jewelry and handmade pieces. This technology applies to most types of precious metals and alloys and continues to evolve with advancements like vacuum and centrifugal casting machines. These processes minimize material loss and improve the quality of the final product. Due to manufacturers’ emphasis on scalability and precision, casting equipment remains a massive investment area for this sector.

Market Leader: Rio Grande (Market Share: 11.6%)

Top Competitors: Durston Tools Ltd., Gesswein Inc.