Editor’s Note

This analysis examines the escalating trade and investment measures between the US and China, arguing that recent actions—including stricter export controls—represent a decisive and enduring shift in the international trade order, moving beyond cyclical tensions toward a new structural reality.

Examining the major trends in the US-China conflict, the tit-for-tat trade measures have not subsided but rather intensified through the first Trump administration and the Biden administration. From September 2024 to January 2025, during the final phase of the Biden administration, the exchange of trade and investment measures between the US and China escalated, including stricter export controls. While detailed in section (2) “Trade Policies of Major Countries/Regions,” the US side introduced measures such as significant hikes in tariffs on Chinese imports, investment restrictions on China in semiconductors, AI, and quantum fields, and strengthened export controls on semiconductor manufacturing equipment and AI memory. In response, China strengthened export controls on items related to antimony, super-hard materials, and drones, and banned exports of gallium, germanium, and antimony to the US. In December 2024, it implemented the Dual-Use Items Export Administration Regulations, which introduced US-style re-export controls and strengthened end-user management (Chart III-4).

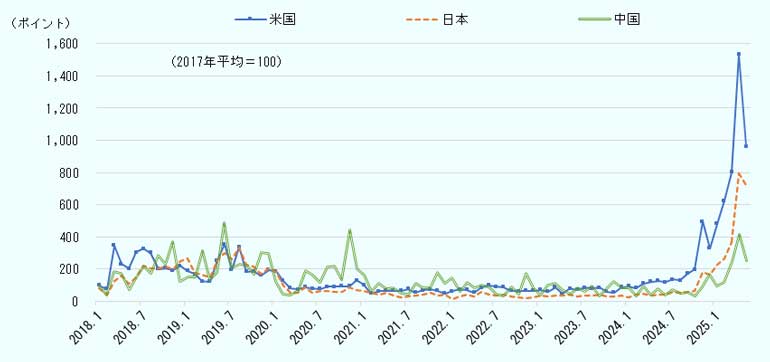

As of July 2025, the global trade order faces unprecedented and severe uncertainty. The “Trade Policy Uncertainty (TPU) Index,” a measure of trade policy uncertainty, began to rise gradually in Japan and the US from January 2025 when the second Trump administration took office, reaching record highs in April (Chart III-1). In China, it has also reached levels comparable to 2019 and 2020. In June 2025, the OECD pointed out that high tariffs and trade policy uncertainty are major factors suppressing global economic growth. It analyzed that expanding trade barriers, difficulty in predicting policies, and declining institutional trust are dulling corporate investment decisions and making supply chain restructuring difficult.

One major source of this uncertainty is the United States. “America First” trade policies are rising, centered on that country. The US has successively implemented measures including the largest tariff hikes in over 100 years, screening of inbound investment and restricting outbound direct investment, protecting and favoring domestic industries, and strengthening sanctions against China (see Section 1, Item 2 of this chapter). These are moves that negate the “rules-based free and fair trade system” led by the US itself through WTO agreements and economic partnership agreements, significantly undermining existing rules and institutions.

Richard Baldwin, a professor at the Swiss business school IMD, points this out. Furthermore, he predicts a scenario where the global trend of protectionism continues. He states that this series of tariff measures is not merely a tit-for-tax imposition with China as seen during the first Trump administration, but “a more destructive, structural attack on the world trading system itself.” According to his commentary, tariffs are not being used as a tool of economic policy but as a performance for (American citizens’) political dissatisfaction and sentiment. He suggests that US tariff barriers could redirect exports destined for the US to third countries. Increased inflows into third-country markets could trigger a “chain of protectionism,” causing new countermeasures and tariff barriers.

On the other hand, he presents an optimistic scenario of the revival of the international trade order and renewed growth in world trade through “re-globalization” excluding the US, expressing hope. That is, since the US share of world trade is less than 15%, if the countries and regions accounting for the remaining 85% defend trade rules, the free trade system could be maintained. In his scenario, major trading countries and regions, including Japan, the EU, China, the UK, South Korea, and India, would take on the role of decentralized leaders championing free trade and upholding a rules-based trade order.

According to the database of “Global Trade Alert (GTA),” operated by the Swiss non-profit St. Gallen Endowment for Prosperity Through Trade, which monitors and reports policy intervention measures affecting world trade and investment, the number of harmful measures introduced globally in 2024 reached 3,505 (Chart III-2). This is flat compared to 2023, confirming a trend of remaining at a high level. From January to May 2025, the number was 1,274, a slight increase compared to the same period the previous year.

Of the harmful measures introduced in 2024, subsidies (excluding export subsidies) accounted for 1,967 items, or 56.1% of the total, followed by export-related measures including export restrictions and export subsidies at 441 items (12.6%), government procurement regulations at 276 items (7.9%), trade-related investment measures at 194 items (5.5%), and tariff-related measures at 178 items (5.1%). Government subsidies continue to be the most frequently deployed, as in the previous year. By country, the US deployed the most at 716 items, followed by Brazil (321), Germany (292), China (276), and India (234). In terms of the number of times harmed by other countries’ harmful measures, China was the highest at 1,224 times. Additionally, Germany (1,080), France (1,040), Italy (1,034), the UK (1,013), and the Netherlands (1,004) each exceeded 1,000 times.

Countries deploying harmful measures against China are led by the US (416 items), followed by emerging economies like Brazil (121), India (116), Russia (85), Turkey (46), Indonesia (20), and European countries like Germany (99), Italy (53), and France (46). Examining harmful measures against China by industrial sector, basic metals like iron and steel account for 15.5% of the total, the highest. Adding metal products brings it to 21.2% of the total. This background is believed to be related to China’s overcapacity problem. Despite a declining trend in economic growth rate due to factors like a worsening real estate market in China, production of items like steel is increasing, strengthening the trend of cheaply exporting surplus not consumed in the domestic market overseas. Also, while the steel overcapacity problem was evident in the mid-2010s, caution is now being shown regarding overcapacity in advanced industries like electric vehicles (EVs) and semiconductors.

Countries concerned about the influx of cheap Chinese products are initiating anti-dumping (AD) and countervailing duty (CVD) investigations against Chinese products. According to the WTO Trade Remedies Portal, the number of AD investigations against China in 2024 reached a record high of 152, 2.4 times the previous year. The number of CVD investigations also reached 25, 2.1 times the previous year, the second-highest level after 2018 (Chart III-3).

In the conflict between the two superpowers, the US and China, the deployment of trade and investment-related measures by both countries intensified from the second half of 2024. Furthermore, since the inauguration of the second Trump administration in January 2025, the administration, advocating “America First,” has rapidly rolled out unprecedented trade measures, such as imposing additional tariffs on imports from the entire world, regardless of whether they are adversarial or friendly nations.