Editor’s Note

This analysis highlights the steady growth trajectory of the global abrasives market, driven by demand from high-precision manufacturing sectors like electric vehicles and aerospace. The shift toward synthetic materials underscores an industry focus on performance and reliability in advanced machining applications.

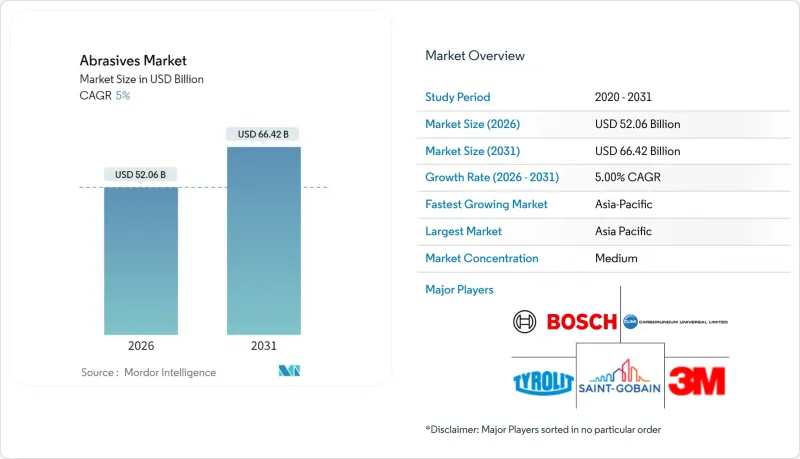

The abrasives market is projected to grow from USD 49.58 billion in 2025 to USD 52.06 billion in 2026, and is expected to reach USD 66.42 billion by 2031, registering a CAGR of 5.0% from 2026 to 2031.

The sales momentum reflects increasing demand for high-performance materials capable of maintaining tight tolerances on advanced CNC equipment, particularly in the machining of electric vehicle (EV) and aerospace components. Synthetic grades continue to gain orders as they offer reliable hardness and thermal stability, while bonded types are positioned as mainstays for high-temperature grinding. Rapid industrialization in Asia, the shift towards precision electronics, and the rise of post-processing needs in additive manufacturing (3D printing) all reinforce the growth foundation of the abrasives market. Competitive rivalry is intensifying, and as regulatory bodies tighten standards on particulate matter and volatile organic compounds (VOCs), major incumbents are refining their product portfolios around environmentally friendly chemical compositions. Meanwhile, niche manufacturers are expanding their share in specialized areas such as diamond-based superabrasives.

The demand for advanced aircraft alloys and lightweight EV powertrains is leading manufacturers to increasingly specify cubic boron nitride (CBN) and diamond wheels, which maintain their form even during high-speed machining. Tier-1 suppliers are optimizing machining lines using vitrified CBN and ceramic abrasives, achieving reduced cycle times and extended dresser intervals in the processing of E-Axles, rotor shafts, and battery housings.

With the proliferation of robots on assembly lines, a uniform surface finish unattainable by manual grinding is increasingly required, driving continued growth in the abrasives market.

Steel service centers, pressure vessel plants, and contract machinists have upgraded grinding stations to ceramic abrasive belts. This has enabled up to a 40% increase in cut rates while reducing power consumption. Reduced downtime from belt changes contributes to improved Overall Equipment Effectiveness (OEE), a metric increasingly valued under lean production systems. Special topcoats, such as VSM TOP SIZE, mitigate heat discoloration on stainless steel workpieces, allowing higher feed pressure without thermal distortion. Such productivity gains support faster order processing, making premium ceramic grades indispensable in cost-sensitive, high-volume production environments.

Synthetic diamond and CBN crystals are grown under pressures and temperatures exceeding geological conditions, making the capital intensity of reaction vessels significantly higher than traditional fused alumina lines. Single-head CNC grinding machines configured for diamond wheels require precision spindles and closed-loop cooling systems, driving up acquisition costs. While these tools offer long life and low cost per part, small to medium-sized machine shops in price-sensitive economies still tend to postpone upgrades. Vendors are piloting lease models and consumable credit programs, but financing constraints limit widespread adoption.

As of 2025, synthetic abrasives accounted for 66.35% of the abrasives market, underpinned by user preference for uniform crystal morphology leading to predictable wear patterns in production processes. While alumina remains the dominant abrasive, silicon carbide is suitable for non-ferrous metal processing, and CBN for hardened steel machining. Novel nano-polycrystalline diamonds under development by Sumitomo Electric promise superior fracture toughness, preparing the abrasives market to handle nickel-based superalloys with low wheel wear rates. Natural garnet maintains a foothold in waterjet and blasting operations due to its recyclable bulk media and enhanced site safety from low free silica content, making it an attractive choice for infrastructure refurbishment projects.

The shift towards synthetic products indicates compatibility with automated feeding systems requiring strict control over particle size distribution, a parameter more easily achieved through engineered manufacturing processes. While supply stability is improving with expanded fused alumina production capacity in Asia, fluctuating power tariffs can impact production costs. Manufacturers aiming for environmental labels are investing in renewable energy-powered arc furnaces and closed-loop water cooling systems to maintain share in regulated regions. Consequently, the abrasives market continues to elevate quality standards even in high-volume segments.

Bonded abrasives, accounting for 47.55% of sales revenue in 2025, reflect their role in cutting, grinding, and finishing operations in automotive, aerospace, and general machinery factories. Resin and vitrified matrices provide thermal stability during deep-cut operations, achieving consistent tolerances on crankshafts and turbine blades where metallurgical integrity is critical. Advances in sol-gel alumina and engineered pore structures have improved chip evacuation, enabling higher metal removal rates without the risk of burning.

Coated abrasives, while lower in tonnage, are widely utilized in finishing and deburring. Diverse backings, from flexible films to fiber discs, optimize performance on contoured surfaces and hard-to-reach areas. Superabrasives, though currently niche, are growing at double-digit rates, supporting the future direction of the abrasives market. Additive manufacturing plants specify diamond pads and CBN mandrels for thin-walled titanium parts where conventional wheels clog quickly. Suppliers like Imerys offer tailored fused alumina and sol-gel particles that extend dresser intervals, enhancing the superiority of bonded abrasives while bridging the performance gap with superabrasives.

The abrasives market report is segmented by Material (Natural Abrasives and Synthetic Abrasives), Type (Bonded Abrasives, Coated Abrasives, Superabrasives), Abrasive Grain/Raw Material (Alumina, Silicon Carbide, etc.), End-user Industry (Metal Fabrication & Processing, Automotive & Aerospace, etc.), and Region (Asia-Pacific, North America, Europe, South America, Middle East & Africa).

In 2025, the Asia-Pacific region accounted for 55.40% of global purchase volume, reflecting China’s massive machining base and India’s accelerating infrastructure build-out. Government incentives for domestic EV battery manufacturing and electronics assembly are stimulating further local demand. Japan and South Korea are leveraging advanced diamond semiconductor research, creating new downstream applications for superabrasives, such as slicing large-area diamond wafers. These factors collectively sustain Asia’s leadership position, encouraging multinationals to localize mixing and pressing operations.

North America maintains steady growth in aerospace, medical, and additive manufacturing sectors. Tightening regulations on VOC and particulate emissions are driving a shift towards garnet blasting media and water-based coolants, promoting product portfolio sophistication.

In Europe, the emphasis on sustainability and circular economy principles has led suppliers like Saint-Gobain to introduce recycled bond systems to reduce carbon intensity. While Germany’s precision machinery cluster accelerates superabrasive adoption, Southern Europe focuses on consumption for construction-related blasting and cutting discs. South America, the Middle East, and Africa, though still smaller in scale, are recording robust growth alongside industrial advancement. Shipyards in Brazil and petrochemical projects in the Gulf region indicate a diversifying end-user base. Local machining partnerships are helping global brands penetrate these regions, strengthening the global coverage of the abrasives market.