Editor’s Note

This analysis highlights the volatile interplay between geopolitical tensions and market fundamentals currently shaping oil prices. The initial support from Middle East risks, followed by a mid-week correction, underscores the market’s sensitivity to both immediate headlines and underlying supply data.

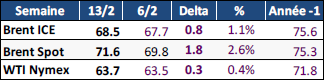

Last week, oil prices were supported at the beginning of the period by persistent geopolitical tensions in the Middle East, particularly after a US warning regarding navigation in the Strait of Hormuz.

Mid-week, however, prices fell by about $2/b. This decline resulted from a combination of both geopolitical and structural factors. On the geopolitical front, the opening this week in Geneva of a new round of negotiations between the United States and Iran on the nuclear issue helped ease immediate tensions related to Iran, thereby reducing the risk premium on oil markets. On the supply side, several sources indicate that OPEC+ is considering resuming its production increases as early as April, a decision that could be formalized at the March 1st meeting. Furthermore, the Trump administration has accelerated the granting of waivers to sanctions targeting Venezuela, facilitating the return of investments in the oil sector and opening the prospect of a restoration of pre-blockade production levels as early as the second quarter of the year (around 1 Mb/d). Finally, the latest monthly report from the International Energy Agency confirmed weaker-than-expected global demand growth for this year, as well as a significant supply surplus. These factors, combined with a sharp rise in weekly US oil inventories, reinforced downward pressure on crude prices.

For the week, Brent for May delivery increased by 1.1% to $68.5/b, while WTI rose slightly by 0.4% to $63.7/b. The Bloomberg consensus of February 13 is stable, with an estimated Brent price of $61/b for the first quarter. Market positioning data shows that speculative positions remained broadly stable over the past week but still at a significantly higher level compared to the previous year, maintaining a downside risk bias. (Fig. 1 to 3)

Last week, oil prices were very volatile, mainly due to tensions between the United States and Iran, as well as discussions surrounding the Iranian nuclear program.

Markets swung from hopes of de-escalation to fears of escalation, reacting sharply to every diplomatic or military announcement in the region.

Beyond these geopolitical tensions, several structural factors influenced the evolution of oil prices. OPEC+ first confirmed the maintenance of its production for March, an expected decision that helped stabilize market expectations. Simultaneously, the United States recorded an unexpected drop in its crude inventories, with a decline of 3.5 million barrels, which reinforced upward pressure on prices. Another major event marked the week: the conclusion of a trade agreement between Washington and New Delhi. The United States agreed to reduce tariffs on certain Indian products in exchange for India’s commitment to stop its purchases of Russian oil, a measure that also fits within the tightening of sanctions against Russia. This agreement could, in the long run, reshape global oil supply flows. Finally, Saudi Arabia lowered the price of its Arabian Light crude for Asian buyers to its lowest level since 2021 relative to the Oman/Dubai average price, confirming that the market remains in a situation of oversupply.

For the week, Brent for April delivery fell by 1.2% to $67.7/b, while WTI rose slightly by 0.2% to $63.5/barrel. The Bloomberg consensus of February 6 was revised upwards, with an estimated Brent price of $61/b for the first quarter. Finally, positioning data shows that speculators continued to buy oil contracts heavily. The weight of speculative positions on Brent and WTI reached its highest level since September, a sign of a market heavily dominated by bullish speculators (Fig. 10). In this context, analysts now believe that speculative flows should continue to weigh overall on crude prices, but with more limited upside potential and an increased risk of rapid downward corrections, unless a new major geopolitical event occurs.

Oil prices rose sharply last week, reaching their highest level in six months on Thursday. This increase is mainly explained by geopolitical tensions between the United States and Iran, which currently dominate the market.

Statements by US President Donald Trump, mentioning possible targeted military strikes against Tehran, revived fears of a major disruption to oil supply. These concerns were reinforced by military movements and the announcement of new US and European sanctions targeting Iran. The main risk for the markets remains a regional escalation likely to affect oil flows, particularly via the Strait of Hormuz through which nearly 20 Mb/d transit.