Editor’s Note

This article highlights a pivotal moment for China’s jewelry sector, which has become the world’s second-largest consumer market. A key takeaway is the significant untapped potential for e-commerce, as online sales currently represent less than 5% of the total. This gap points to a major growth opportunity as consumer habits evolve.

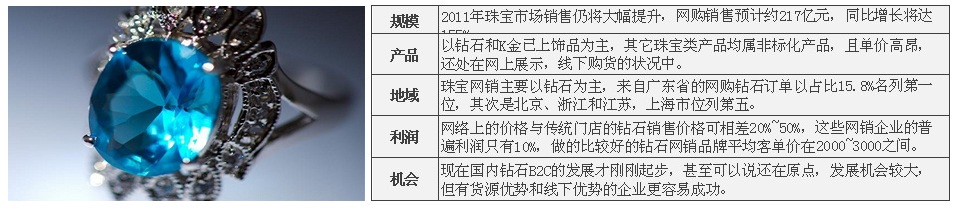

1) Scale

Data shows that China has become the world’s second-largest jewelry consumer market. However, due to the ongoing process of building a domestic social credit system, the habit of domestic consumers buying jewelry online has yet to fully form. This results in online jewelry sales in China accounting for less than 5% of total jewelry sales, indicating enormous growth potential. Industry insiders predict that jewelry market sales will continue to rise significantly in 2011, with online sales estimated at approximately 2.17 billion yuan, a year-on-year growth of 155%. In the next 3-5 years, the share of online jewelry sales is expected to reach 20%.

Zhubird (Zhubird)

B2C Website + Offline Experience Stores

This model is primarily adopted by online jewelry brands, often starting as internet companies and then expanding from online websites to opening offline experience stores. It represents a specialized jewelry sales network combining “brick-and-mortar + click.”

Representative Companies: Zhubird, Oubaili, Aido Jewelry.

Advantages: Eliminates customer doubts, allows users to experience products offline. Low prices.

Disadvantages: Requires bearing the capital risk and operational costs of establishing offline experience stores. The low profit margins from online sales may be used to offset losses incurred by the offline presence.

Diamondvip (Diamondvip)

Pure B2C Website

Representative Company: Diamondvip.

Advantages: Focuses solely on online sales, high brand value, low investment, targeted user base.

Disadvantages: Lack of physical store support, high unit prices subject to significant constraints from online consumer trust mechanisms.

Zhou Dafu (Chow Tai Fook)

B2C Website + Traditional Enterprise’s Offline Stores

Starting in 2008, facing the intense competition and commoditization in the traditional jewelry industry, original wholesalers and traditional retailers also began opening online stores. Many well-known brands also established sales platforms online. These traditional jewelry merchants partnered with large websites to develop online malls and direct sales networks, appearing in forms like recommendations and promotions.

Representative Companies: Chow Tai Fook, Lukfook, King Fook Jewelry, Chow Sang Sang, Diamond.com, etc.

Advantages: High brand recognition, guaranteed by offline physical presence.

Disadvantages: Low website traffic, relatively high prices.

Xinzuan.com (Xinzuan.com)

Vertical B2C Mall

Representative Company: Xinzuan.com.

Advantages: Diverse range of represented brands, offering consumers greater choice.

Disadvantages: The platform simultaneously connects with multiple brand merchants, facing high pressure, significant human resource consumption, and the high transparency of diamonds makes it very difficult to profit from single-channel operations.

Dangdang.com (Dangdang)

Jewelry Channel within a B2C General Merchandise Platform

Representative Company: Dangdang.com.

Advantages: High traffic volume.

Disadvantages: Low target customer conversion rate.

1) Credibility of Online Brands

Online brands can develop offline stores but will face capital risks.

2) Impact of Establishing Professional Sales Platforms on Existing Distributor Channels

Conflicts with original channels and products; consider producing exclusive online models and using some offline inventory to supplement SKUs.

3) Severe Product Homogenization, Often Manifesting as Price Wars

Diamonds are standardized products with limited room for style innovation; therefore, it’s more appropriate to avoid homogeneous competition and consider personalized customization services.

4) Weak Customer Management Systems and Information Technology Infrastructure

5) Low Professionalism Among Practitioners, High Turnover Rate; Employers Lack Binding Mechanisms

Before 2003: The Budding Period of Domestic Jewelry E-commerce

Representative B2B Platforms: 8848, 21st Century, Youzhan.com.

Result: Enterprises and third parties lacked experience, failing to effectively solve issues like electronic payment, credit mechanisms, logistics, and after-sales. The general consumer lacked awareness of online shopping, and penetration rates were also relatively limited.

2004-2006: The Rapid Expansion Period of China’s Jewelry E-commerce

In 2004, the US company Blue Nile went public on NASDAQ, announcing the success of the diamond jewelry e-commerce model.

During this period, Taobao’s three-year free strategy and Eachnet’s price reduction strategy lowered the barrier to entry for C2C e-commerce, attracting a large number of users to participate. Jewelry products became hot-selling items on C2C auction websites.

A large number of e-commerce jewelry websites were established, and online diamond sales quietly emerged. Many jewelry enterprises and companies also built their own professional websites.

Result: Influenced by domestic public consumption concepts, the idea of “online shopping” for jewelry products was not widely recognized or accepted. Most websites built by jewelry enterprises with “huge investments” existed merely as information publishing tools. Jewelry websites did not achieve e-commerce functionality nor bring actual economic benefits to jewelry enterprises.

Post-2007: Domestic Jewelry E-commerce Enters a Period of Intense Competition and Rational Development

External Environment: From 2007 to the end of 2009, Chinese internet users had grown to 384 million, with the 14-29 age group accounting for 70% of the structure. With the development of the wedding market and the rise of the national GDP index, the demand index of domestic consumers increased, fostering investor attention to the jewelry industry and indirectly extending the industry’s growth cycle. In the next 3-5 years, jewelry sales volume will still have significant room for growth.

Internal Development: Early diamond merchants like Zuokaya and Zhubird, who started on Taobao, have now, through long-term accumulation, established their own independent B2C sites, and even offline stores. They have now stabilized their footing across different channel sites. Traditional channel distributors began to value the B2C model. In the recent two years, a large number of jewelry network brands have emerged in Shanghai, Zhejiang, Beijing, and Guangdong.

1) Conversion Rate:

The ratio of the number of buyers who actually purchased goods to the total number of shoppers entering the store within a certain period. Merchants need to promote this conversion through marketing processes or means, turning more in-store shoppers into actual buyers.

2) Taobao Brands:

This concept first appeared in the clothing field. Many original brands gathered on Taobao initially started because designers’ personal hobbies led them to create online brands, unexpectedly gaining great popularity on Taobao. Later, some self-owned brands in toys and cosmetics also emerged. These brands established on Taobao are called “Taobao Brands.”

3) Third-Party Payment (Tool):

Refers to an independent third-party institution with contracts with major banks, possessing certain strength and credit guarantee, providing a transaction support platform. In transactions through third-party payment platforms, after the buyer selects a product, they use the account provided by the third-party platform to pay for the goods. The third party notifies the seller of the payment arrival for shipping; after the buyer inspects the goods, they can notify payment to the seller, and the third party then transfers the funds to the seller’s account.

4) Online Group Buying:

The behavior of organizing consumers with the same purchase intention through internet channels to conduct bulk purchases from manufacturers. Relying on the network, it can organize netizens with the same purchase intention to conduct group purchases from manufacturers, transforming the previously passive buyer’s right into an active one, changing the weak position in consumer behavior. It not only maximizes cost savings but also occupies a relatively active position in the purchasing and service process, offering higher security and better service.

5) Overseas Purchasing Agent:

Refers to individuals or purchasing agents helping domestic consumers buy goods from overseas. Overseas purchasing agents are mainly divided into two types: one is private purchasing agents, the other is enterprise purchasing agents. The former generally opens online stores on C2C websites like Taobao to provide purchasing services for customers; the latter are mostly professional domestic and foreign shopping websites.

6) Mobile E-commerce:

Refers to e-commerce conducted using wireless terminals such as mobile phones, PDAs, and palmtop computers for B2B, B2C, or C2C. It combines the Internet, mobile communication technology, short-distance communication technology, and other technologies, enabling people to conduct various commercial activities anytime, anywhere, achieving online and offline shopping and transactions, online electronic payments, and various transaction activities, business activities, financial activities, and related comprehensive service activities.