Editor’s Note

This article examines Titan’s strategic shift into the lab-grown diamond market, exploring the internal data and changing consumer trends that prompted the move after a prolonged period of public skepticism from its leadership.

For nearly six quarters, Titan’s stance on lab-grown diamonds was remarkably consistent. Quarter after quarter, even as analysts pushed the narrative of LGDs as the next big disruption in Indian jewellery, management refused to play along.

As far back as Q1 FY25, Titan’s leadership was clear that whatever noise existed around lab-grown diamonds was not showing up where it mattered most: inside their stores. The management said they were actively tracking customer behaviour across Tanishq, CaratLane, Mia, and Zoya, and yet they were “not seeing material inquiries.” What they were hearing instead was something far more defensive than aspirational.

Customers were not asking for lab-grown diamonds; they were asking whether the diamonds Titan sold were natural. Some went so far as to demand certification that what they were buying was “entirely natural.” In other words, LGDs were entering the conversation not as a product customers wanted, but as a source of anxiety they wanted reassurance against.

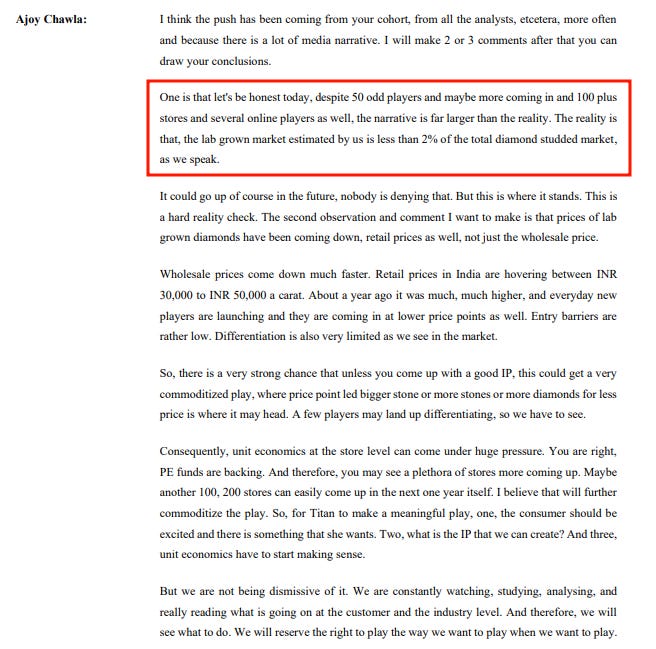

By Q1 FY26, Ajoy Chawla, the CEO of Titan, would explicitly frame the disconnect by saying that despite “50-odd players,” over a hundred stores, and multiple online platforms, the “narrative is far larger than the reality.” Titan’s own estimate placed lab-grown diamonds at less than 2% of the overall diamond-studded market. This, he called, a “hard reality check.”

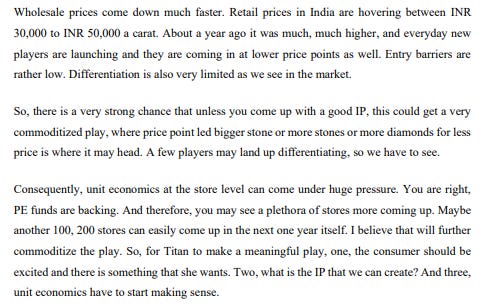

The barriers to entering this business were low, and there wasn’t much to differentiate one LGD seller from another. There was plenty of capital chasing the opportunity—private equity money was fuelling aggressive store rollouts. It wouldn’t take much, they suggested, for another 100 or 200 LGD stores to pop up across the country.

But this was exactly why Titan was hesitant.

The falling prices, the low barriers to entry, the ease with which new players could replicate the model—management saw all of this as a warning, not an invitation. Without some kind of proprietary edge, they argued, lab-grown diamonds would turn into a commodity business where the only pitch is “bigger stones for less money.” In a market like that, brand doesn’t count for much, and margins come under pressure quickly.

Titan was clear that it had no interest in entering just for the sake of being there. If the company was going to participate, three things had to line up:

Titan also made a point that often gets overlooked: the consumer herself was confused.

Management described customers as uncertain i.e. they are curious about lab-grown diamonds, willing to experiment, but also worried about whether these stones would hold their value. First-time diamond buyers were especially hesitant. For many Indian households, the first diamond purchase happens somewhere in the ₹70,000 to ₹1 lakh range, and at that price point, the idea of diamonds as a store of value still matters a lot.

Given all of this, Titan’s answer for most of the last year and a half has been patience. Management was upfront about it—they were in “wait and watch” mode. Analysts pushed repeatedly, sometimes bluntly, asking what exactly was stopping Titan from entering a segment where margins appeared healthy, and competitors were scaling quickly. The answer, each time, was not that Titan could not enter, but that it would not do so prematurely.

So the question now is: What changed? Are customers finally asking for lab-grown diamonds in a way they weren’t before? Has Titan figured out how to make this business defensible—or have they decided that doesn’t matter as much as they said it did? And if none of their three conditions have actually been met, why move now? Is this opportunity, or is it the worry that staying out costs more than going in?