Editor’s Note

This article provides a foundational overview of automotive accessories, defining them as products that complement a vehicle’s core functions. It outlines their broad application across vehicle types and their diverse roles in enhancing convenience, protection, and driving performance.

Automotive accessories are a group of related products used to complement or extend the basic functions of a finished vehicle. They are widely adopted across various vehicle types, including passenger cars and commercial vehicles. Their applications are diverse, ranging from improving convenience during daily driving, maintaining the vehicle’s interior and exterior environment, protecting cargo, to assisting with visibility and operability while driving. They are utilized not only by individual users but also in commercial and fleet vehicles as elements supporting operational management and vehicle maintenance, with the characteristic of being designed for aftermarket installation.

Key product characteristics of automotive accessories include vehicle compatibility, durability, and ease of installation and replacement. To withstand the in-vehicle and external usage environments, they require resistance to temperature changes, vibration, and dirt, and are designed for long-term use. Additionally, it is crucial that they comply with regulations and safety standards while having a structure that minimally impacts the existing vehicle. The product portfolio is segmented by application, allowing for selection based on specific usage purposes.

According to QYResearch’s survey report, the automotive accessories market is classified into the following major segments, with detailed analysis of market trends and growth potential in each field:

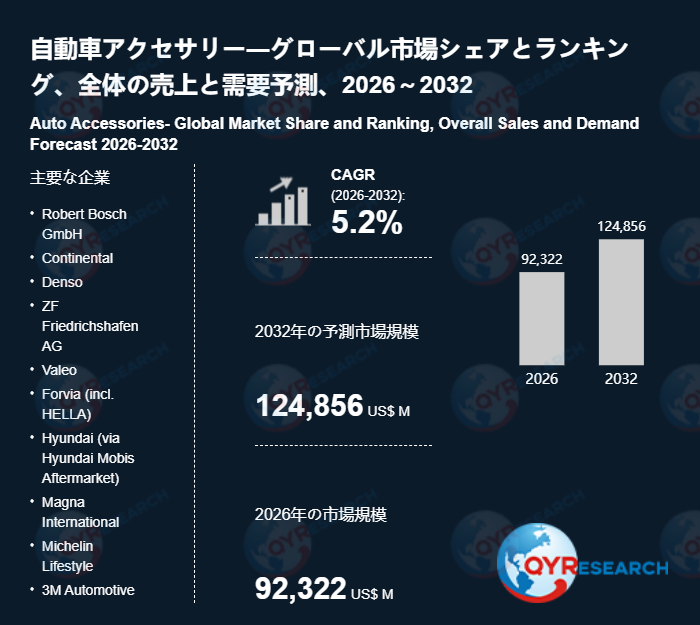

Key companies in the automotive accessories market include: Robert Bosch GmbH, Continental, Denso, ZF Friedrichshafen AG, Valeo, Forvia (incl. HELLA), Hyundai (via Hyundai Mobis Aftermarket), Magna International, Michelin Lifestyle, 3M Automotive, Garmin, Pioneer Corporation, Momo Srl, Thule Group, Pep Boys, O’Reilly Auto Parts, U.S. Auto Parts Network, CAR MATE MFG, Covercraft Industries, Lloyd Mats, Pecca Group Berhad, Stanley Black & Decker (Automotive segment).

The automotive accessories market is segmented as follows:

By Product: Interior Accessories, Exterior Accessories, Electronic Accessories, Safety Accessories, Others.

By Application: Passenger Car, Commercial Vehicle.

The report provides a detailed explanation of market size, growth rates, and demand trends for the following key regions/countries:

North America: United States, Canada.

Europe: Germany, France, United Kingdom, Italy, Russia, Rest of Europe.

Asia Pacific: China, Japan, South Korea, Southeast Asia, India, Australia, Rest of Asia Pacific.

Latin America: Mexico, Brazil, Rest of Latin America.

Middle East & Africa: Turkey, Saudi Arabia, UAE, Rest of Middle East & Africa.

This report serves as essential information for companies to understand the latest trends and future outlook of the automotive accessories market and to support strategic decision-making.

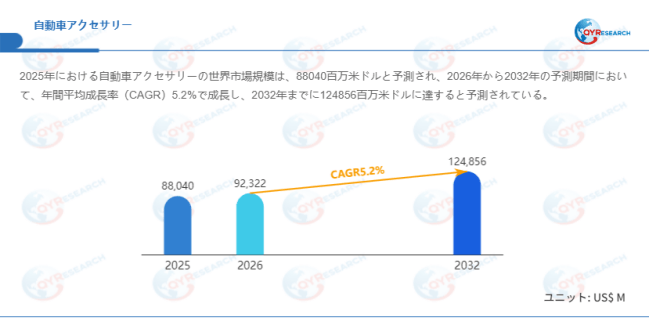

According to a new market research report published by QYResearch, “Auto Accessories – Global Market Share and Ranking, Overall Sales and Demand Forecast, 2026-2032”, the global automotive accessories market size is expected to expand steadily from approximately USD 88.04 billion in 2025 to USD 92.322 billion in 2026. It is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% during the forecast period, reaching USD 124.856 billion by 2032.

1. Sophistication of Demand Structure through Technological Integration

With the progress of integration between IoT, artificial intelligence, and vehicle systems, the role and demand structure of automotive accessories are changing. Consumer expectations for advanced functional experiences in vehicles are driving demand in areas such as in-vehicle infotainment components, Advanced Driver-Assistance Systems (ADAS)-compatible sensors, and smart dashcams. In the Japanese market as well, the positioning of automobiles is shifting from mere transportation tools to high-functional information terminals, and this change is supporting the advancement of automotive accessories.

2. Sustained Demand Driven by Customization Trends

The expansion of consumer segments, particularly among younger generations, and changes in aesthetic sensibilities are diversifying purchase motivations for automotive accessories. In addition to exterior decorative items, interest in interior accessories that enhance comfort and practicality is also growing. In the Japanese market, there is strong demand for customization based on daily use, such as floor mats and storage-related products. Automotive accessories maintain a certain market appeal as a means of expressing individuality through a vehicle’s appearance and user experience.

3. Stability of the Aftermarket

In the automotive accessories market, aftermarket products hold an important position due to price flexibility and a wide range of choices. In Japan, the large stock of owned vehicles and the presence of a certain number of older vehicles lead to continuous demand for replacement and repair accessories. Furthermore, the development of e-commerce platforms and specialized sales channels is advancing the trend of manufacturers and suppliers directly approaching consumers, supporting market stability and flexibility.

1. Demand for Dedicated Accessories Accompanying Electrification Progress

As the adoption of electric vehicles (EVs) progresses in the Japanese market, demand for automotive accessories tailored to the unique usage environment of EVs is becoming apparent. In addition to charging-related equipment and auxiliary devices, interior and exterior accessories aimed at optimizing cabin space and improving operability could become new growth areas. Automotive accessories are expanding their functional roles alongside the advancement of electrification.

2. Penetration of Intelligence and Connectivity

The advancement of autonomous driving technology and the evolution of in-vehicle systems are creating demand for more highly integrated automotive accessories. In the Japanese market, ADAS-related accessories that interact with the vehicle, V2X communication modules, and smart cockpit-related products supporting immersive in-cabin experiences are gaining attention as high-value-added fields. In these areas, reliability and system compatibility become key competitive factors.

3. Supporting Demand Accompanying the Expansion of Light Electric Vehicles

As market entry of small electric vehicles, including light electric vehicles, progresses, vehicle model diversification is accelerating in the Japanese market. Consequently, demand is expected for interior/exterior accessories optimized for specific models, compatible charging solutions, and intelligent-related kits. For automotive accessory suppliers, this presents an opportunity to build touchpoints with new customer segments.

1. Resource Constraints and Core Competency Challenges

As electrification and intelligence advance, Japan relies on overseas procurement for some critical resources, making supply stability a challenge. Furthermore, the trend towards software-defined vehicles demands software and algorithm capabilities even in automotive accessories, but Japan faces constraints in talent acquisition and organizational flexibility.

2. Cost Structure Pressure

The Japanese automotive accessories industry has traditionally relied on efficient manufacturing systems as a source of competitiveness. However, cost pressures are increasing due to global supply fluctuations and volatility in raw material prices. Price fluctuations in materials like rubber and polymers directly impact product profitability, making sustained investment under price competition difficult.

3. Changes in the Global Competitive Environment

Overseas players, particularly from China, are rapidly increasing their presence in electrification and intelligence fields and are building supply systems with cost competitiveness in the automotive accessories sector as well. Additionally, uncertainty in the international trade environment poses a medium- to long-term risk factor for Japan’s automotive and related accessories industry.