Editor’s Note

While global diamond demand shows signs of recovery, the rebound is uneven. This article examines the diverging trends across key markets and consumer segments.

In 2025, diamond demand was up in the world’s top two markets, the United States and India. There were positive signals from many other markets too. China continued to be the exception, though manufacturers believe the country’s decline in demand may have bottomed out.

While this larger picture gives manufacturers in India a reason for optimism, there is a catch. This is not a uniform recovery; there are major variations across different segments.

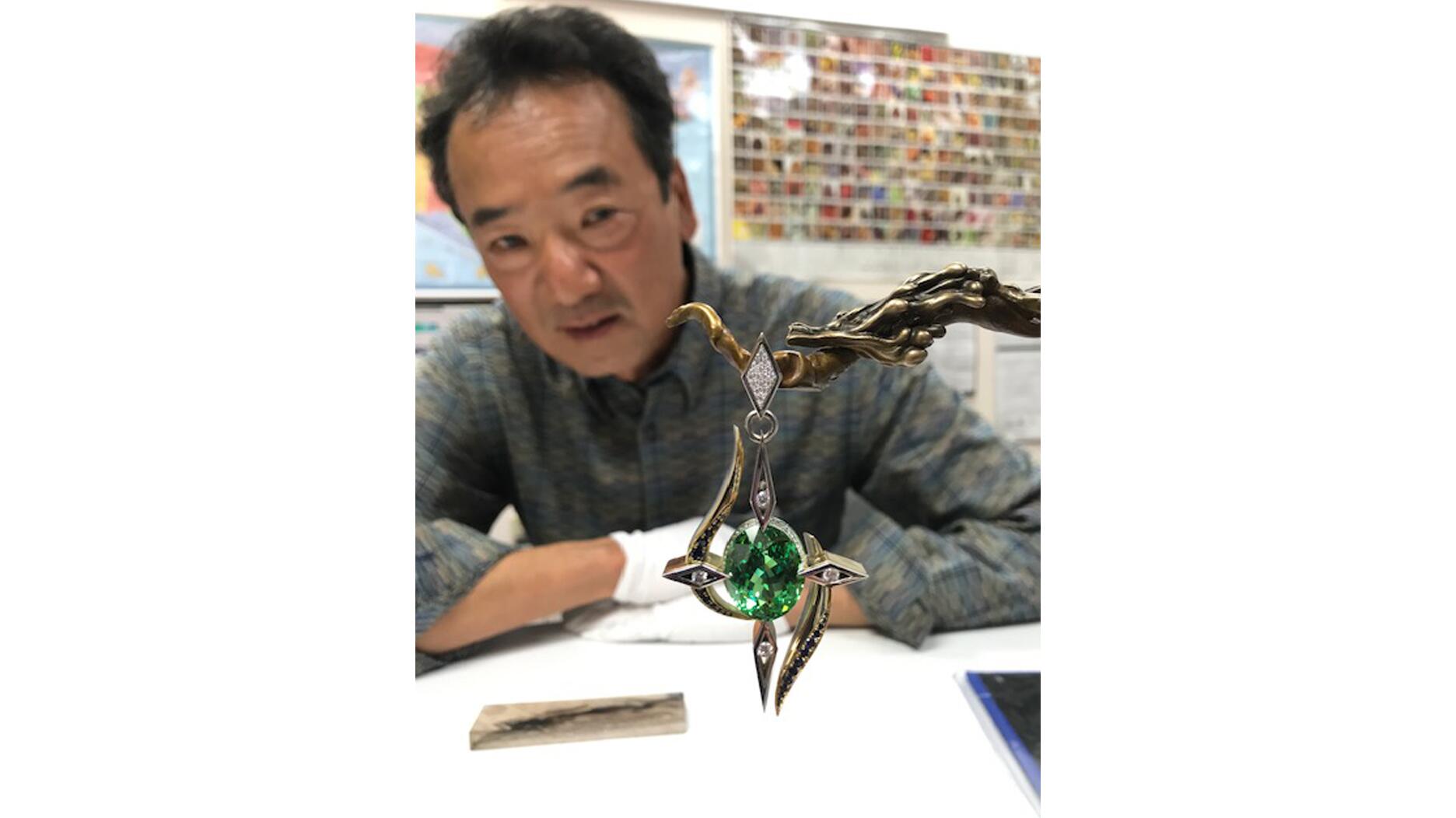

At the retail end, it is the high end that is shining, while the picture at the midstream level varies across three different segments.

Russell Mehta, managing director of Rosy Blue India, said.

He also noted that there is some improvement in the market for smaller goods (below 0.18 carats).

Mehta said.

However, the mid-tier segment of the market—meaning diamonds sized from 20 points to about 2 carats—remains “stressed and difficult” and is unlikely to see any significant change in 2026, he said.

he explained.

Tariffs: here today, gone tomorrow, back the day after. This could well be the storyline that defines the fast-changing contours of the trade in rough and polished.

Concerns over sanctions on Russian diamonds took a back seat in 2025 as tariffs and trade deals, especially the India-U.S. negotiations, dominated discourse.

In early February, it seemed that a settlement between the two countries was near and rough and polished natural diamonds and gemstones would be exempt while the tax on diamond and gemstone jewelry would return to significantly lower rates.

The news provided much-needed relief to the industry, but it was a short-lived high.

Tariffs are back and will remain at 10 percent (possibly increasing to 15 percent) for the next few months.

While that does provide relief for importers of diamond and gemstone jewelry (the import tax will be 10-15 percent instead of 18 percent), it was not immediately clear as of press time if loose natural diamonds and gemstones will still be exempt from tariffs or taxed at 10 percent.

Meanwhile, Indian diamantaires are welcoming the smaller boosts that the country’s trade deals with the United Kingdom, European Union, Oman, Australia and other countries will provide.

A relatively stable balance between supply and demand seems to be returning to the diamond pipeline. Industry analyst Pranay Narvekar believes that it would have happened earlier, but the high U.S. tariffs complicated matters.

He now expects a semblance of equilibrium to return by mid-2026.

Narvekar, however, pointed out that this is not on account of rising demand, but more tightly controlled supply.

he said, predicting that it will hover around 100 million carats for the next few years.

Global diamond production peaked in 2005, reaching almost 177 million carats.

he said.

Empirical evidence suggests the midstream also has restructured over the past few years and overall capacity is now well below the post-COVID peaks of 2022.

Many smaller players have either shifted to cutting lab-grown diamonds or have moved out of the sector due to the prolonged downturn.

Frenzied buying at unrealistic prices is a thing of the past.

Signed in Angola in June 2025, the Luanda Accord is a commitment by diamond-producing countries and key industry organizations to contribute money to the Natural Diamond Council for marketing. The agreement has gained momentum in early 2026, which means there could be a global generic marketing campaign for natural diamonds in place for the holiday season.