Editor’s Note

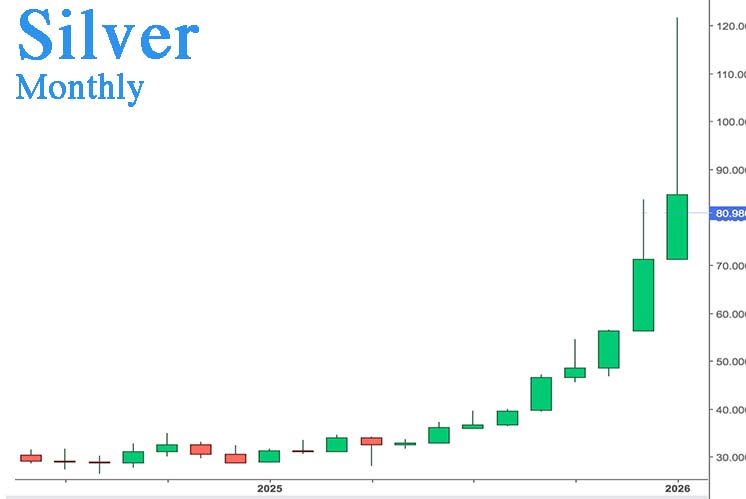

The recent extreme volatility in precious metals markets, with gold prices swinging nearly $1,000 in 24 hours and silver plummeting 33% in a single session, highlights significant price discrepancies between global trading hubs. This analysis examines the forces behind these dramatic moves and the structural factors that can lead to such stark divergences between physical and paper markets.

On Thursday in New York, gold opened the session at $5,630. The next day, it hit a low of $4,700, a difference of nearly $1,000 within 24 hours. At the same time, in Shanghai, physical gold closed at $5,209. How can such price discrepancies between different marketplaces be explained? And more importantly, how can such day-to-day volatility be justified? The price of silver fell by 33% in a single session in New York. A true market aberration, especially since the CME had just precisely limited price fluctuations, both upwards and downwards.

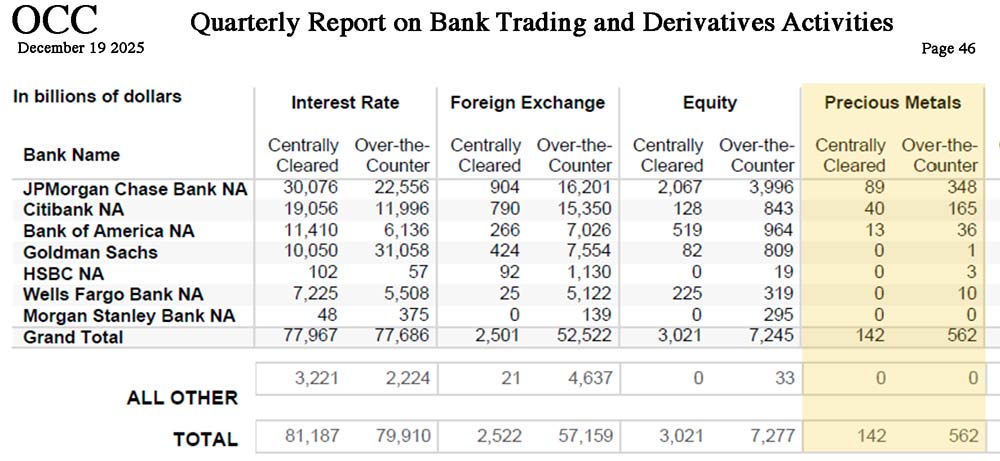

Since December 12 last year, the CME has continuously raised margin requirements, i.e., the mandatory deposit needed to play a contract. For silver, margins were $11,500, which then represented only 3.7% of the contract value, with an ounce of silver trading around $62. They were then successively raised to $18,000, then $22,000, and finally $32,500. On January 12, the CME abandoned the principle of a fixed margin in favor of a percentage of the contract value, set at 9%. Last Thursday, this percentage was abruptly raised to a total of 31.5% (16.5% + 15% maintenance), according to data published by CME Group. As for gold, margins went from 5% to 16.8% (8.8% + 8% maintenance).

Until now, the Cartel’s bullion banks managed to influence physical metal prices via the paper market by depositing only about 4% of the value of the contracts they traded. Now, with margin requirements raised to 31.5%, fewer and fewer speculators have the necessary cash to try to play the rise or fall of precious metal prices. The alchemists are turning paper into lead. And this, before — as I announced in my article of December 31 — margins are potentially raised to 100%. In such a scenario, the COMEX market would lose its uniqueness, as well as its capacity for harm in forming the true market price of precious metals. The paper market would then be transmuted into a real physical metal market. This spectacular rise in margins constitutes a strong signal: we are approaching a “Reset”, accompanied by a revaluation of gold and silver in all currencies, in other words, a synchronized currency devaluation.

The Commodity Futures Trading Commission (CFTC) is the US federal agency responsible for regulating futures markets, including those for commodities and precious metals. On December 31, representatives from JPMorgan and the Commodity Futures Trading Commission reportedly urgently requested a meeting with the heads of the Shanghai Gold Exchange to negotiate a loan of several tens of millions of ounces intended to support COMEX. This request was reportedly refused. Furthermore, the very next day, January 1, all silver shipments destined for export to the West were reportedly blocked in Chinese ports. With the enactment of new Chinese legislation, only a few companies are now authorized to obtain export licenses. In theory, the administrative burdens would involve delays of about six weeks per authorization. In any case, not a single ounce of silver reportedly left China during the month of January. In October, the London market was de facto paralyzed, after nearly defaulting on the delivery of 1,000 tons of silver acquired by India. On November 30, it was then the New York market that experienced a major incident: 7,330 silver contracts of 5,000 ounces were subject to a delivery request. Of this total, 6,816 contracts were ultimately canceled, settled in cash with a $65 million premium. Since this episode, in New York, a significant portion of the officially available-for-sale stocks (“registered”) has been reclassified into the “eligible” category, i.e., theoretically stored but not deliverable. By the end of December, 95% of delivery requests were thus settled in cash. London and New York now appear largely short of float, in other words, of silver truly available for sale. In my article “China is the Absolute Master of the Silver Market”, I suggested — without it being denied — that Chinese banks would be the true owners of a large part of the silver bars accounted for in London and New York. They lease them, but do not sell them.

In an interview on July 4, 2022, Peter Hambro, a major figure in the London Bullion Market Association, detailed the mechanisms for manipulating the price of gold through derivatives. He explained the evolution of the paper gold market in London and its fractional reserve paper gold system, from the 1980s to this day. In the logic of this massive and coordinated manipulation, the SPDR Gold Shares (GLD) ETF was launched in November 2004. The GLD is a financial product supposed to replicate the price of gold, buyable and sellable instantly, with a few clicks, from a computer. The objective of its launch was clear: to divert investors from acquiring real physical gold by offering them paper gold, purely financial and virtual. The product’s statutes even stipulate that no independent audit of the stocks can be required, nor can a request for physical delivery corresponding to the shares held.