Editor’s Note

This article highlights the projected growth of the global diamond jewelry market, driven by cultural traditions and rising affluence in emerging economies.

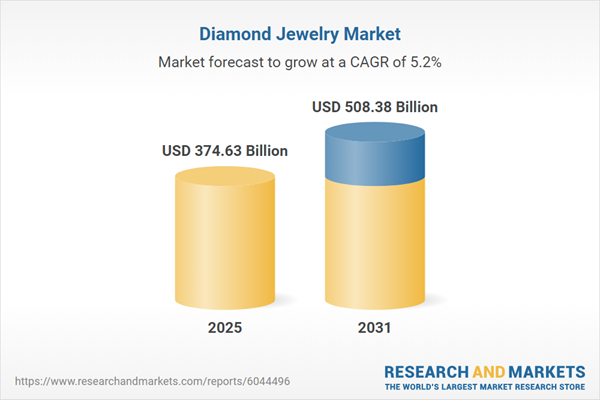

The Global Diamond Jewelry Market is projected to grow from USD 374.63 billion in 2025 to USD 508.38 billion by 2031, registering a CAGR of 5.22%. This sector comprises decorative personal adornments, such as rings, necklaces, and earrings, that feature cut and polished diamonds set within precious metals. Growth is primarily driven by the enduring cultural importance of bridal jewelry and rising disposable incomes in emerging economies, which fuel aspirational luxury consumption. Furthermore, the perception of high-quality diamonds as a tangible asset for wealth preservation continues to bolster demand among affluent buyers seeking appreciation. According to the Natural Diamond Council, the average price of natural diamond jewelry rose by 2.7% to $2,360 in 2024, reflecting resilient consumer valuation despite broader economic fluctuations.

The escalating consumer demand for lab-grown diamonds is fundamentally reshaping the global market by offering a price-accessible alternative that aligns with evolving value perceptions. This surge is particularly evident in the fashion and entry-level engagement segments, where buyers increasingly prioritize carat size and optical quality over geological origin. The segment’s rapid expansion is compelling major retailers to pivot their inventory strategies to accommodate this new revenue stream, effectively democratizing access to larger stones.

Simultaneously, the rising popularity of branded and customized jewelry collections acts as a stabilizing force, securing engagement from high-net-worth individuals who view heritage pieces as investment-grade assets. Established luxury houses are capitalizing on this trend by expanding their high-jewelry offerings, which continue to command premium pricing despite broader inflationary pressures.

Conversely, the broader supply chain faces contraction adjustments; the Gem and Jewellery Export Promotion Council (GJEPC) reported that in 2024, gross exports of cut and polished diamonds from India declined to $15.9 billion for the fiscal year ending March 2024, reflecting the ongoing calibration between natural supply and shifting global demand.

A significant obstacle hindering market expansion is geopolitical instability, which disrupts global supply chains and complicates ethical sourcing protocols. Sanctions on major diamond-producing nations and strict tracking mandates increase compliance costs and create logistical bottlenecks for manufacturers.

Additionally, macroeconomic headwinds, including inflation and slower economic growth in key consumer markets like China, dampen discretionary spending power, thereby restricting potential volume growth in the near term. As the cost of living rises and economic uncertainty prevails, consumers in these primary regions increasingly deprioritize discretionary luxury expenditures. This shift in spending behavior is especially damaging in China, a traditionally high-volume market, where economic stagnation reduces the appetite for high-ticket adornments. Consequently, retailers are compelled to adopt conservative inventory strategies, which creates a ripple effect down the supply chain, reducing orders for manufacturers and suppressing overall trade volumes.

The direct impact of these economic constraints is evident in recent trade performance metrics, illustrating a sharp contraction in market activity.

This significant reduction in export value underscores how sensitive the market is to broader economic health, as diminished purchasing power in critical regions directly restricts the industry’s ability to sustain revenue growth.