Editor’s Note

This report provides a comprehensive analysis of the advanced materials industry, covering historical data from 2021-2024 and offering a detailed forecast for 2026-2033. The 100-page document is designed to equip stakeholders with critical insights for strategic planning in this evolving sector.

Report ID: GVR-4-68040-854-7

Number of Report Pages: 100

Format: PDF

Historical Range: 2021 – 2024

Forecast Period: 2026 – 2033

Industry: Advanced Materials

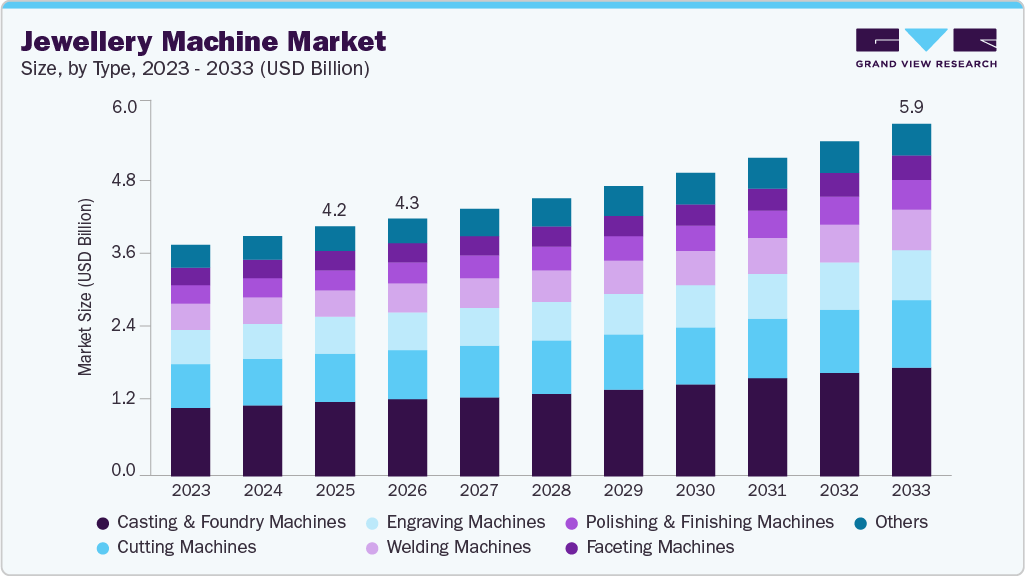

The global jewellery machine market size was estimated at USD 4,211.3 million in 2025 and is projected to reach USD 5,946.0 million by 2033, growing at a CAGR of 4.6% from 2026 to 2033. The jewellery machine industry is driven by rising demand for precision, consistency, and faster production in jewellery manufacturing.

- Asia Pacific dominated the jewellery machine industry with the largest revenue share of 40.7% in 2025.

- The jewellery machine industry in India is expected to grow at a substantial CAGR of 5.7% from 2026 to 2033.

- By product, the casting & foundry machines segment is expected to grow at a considerable CAGR of 5.1% from 2026 to 2033 in terms of revenue.

- By end use, the artisans & small workshops segment is expected to grow at a considerable CAGR of 5.1% from 2026 to 2033 in terms of revenue.

- By mode of operation, the fully automatic segment is expected to grow at a considerable CAGR of 5.0% from 2026 to 2033 in terms of revenue.

- 2025 Market Size: USD 4,211.3 Million

- 2033 Projected Market Size: USD 5,946.0 Million

- CAGR (2026-2033): 4.6%

- Asia Pacific: Largest market in 2025

Growing consumer preference for intricate designs and customized pieces is pushing manufacturers to adopt advanced cutting, engraving, and faceting machines. Automation also helps reduce material wastage, which is critical when working with high-value metals and gemstones.

Another key driver is the rapid modernization of jewellery workshops, especially in emerging markets. Artisans and small workshops are gradually shifting from manual tools to semi-automatic and fully automatic machines to improve productivity and meet large orders. Expanding organized retail jewellery chains are also investing in modern equipment to maintain uniform design standards. In addition, supportive government initiatives for manufacturing and skill development are strengthening market growth.

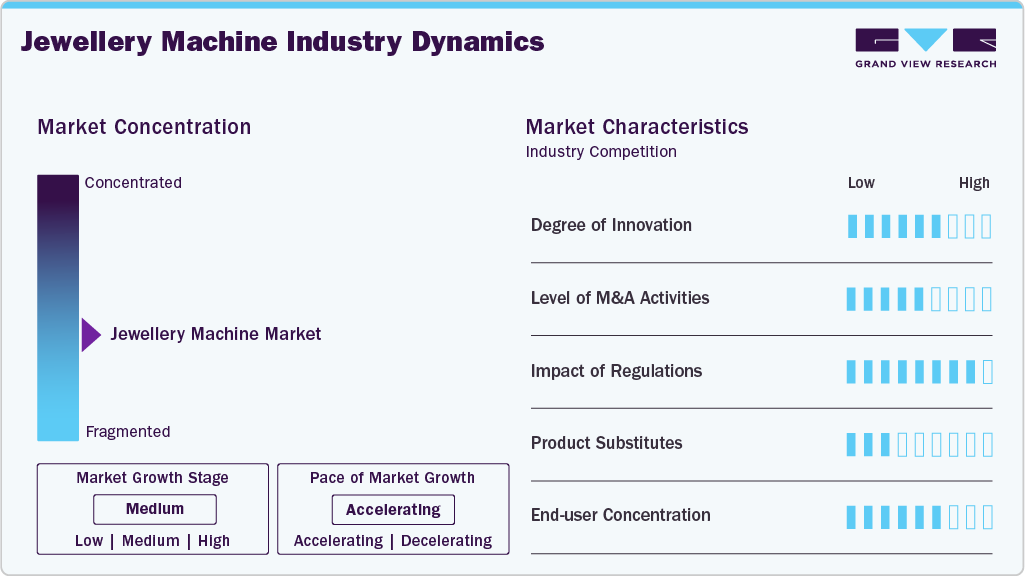

The jewellery machine industry shows a moderately fragmented industry structure, with a mix of global technology providers and a large number of regional and local manufacturers. No single company dominates the market, as demand varies widely based on jewellery type, scale of operation, and level of automation. Established players compete through advanced features and automation, while smaller firms focus on cost-effective and customized machines.

The market shows a steady level of innovation focused on precision, automation, and ease of use. Manufacturers are integrating digital controls, CAD/CAM compatibility, and laser-based technologies to support complex jewellery designs. Energy efficiency and reduced material loss are also key innovation areas. Product upgrades are largely incremental, driven by practical workshop needs rather than disruptive changes.