Editor’s Note

This analysis from Meritz Securities highlights how geopolitical tensions are impacting global diamond markets, driving prices higher and creating potential valuation opportunities in related equities.

According to Meritz Securities, diamond prices are soaring due to geopolitical risks in Russia, and they anticipate indirect benefits for other companies. Using the UK’s Petra Diamonds, an industrial pure-player, as an example, they analyzed that even after its recent sharp stock price increase, it still presents attractive valuation.

As of March, the international diamond price is at $230.3 per carat, a 7.5% increase month-on-month compared to the end of last year. This is close to the peak of the 2010s, which was $234.8 in February 2012.

Russia is a resource powerhouse where exports of raw or semi-finished natural materials account for 69.5% of its total export value. Diamonds are one of its top export items. As of 2020, Russia holds a 29.3% share of global diamond production, making it the world’s top producer.

However, due to Russia’s invasion of Ukraine, Alrosa, a Russian diamond mining company, has been included in various Western sanctions lists. Supply concerns have caused diamond prices, which previously had small fluctuations, to become volatile. Alrosa holds a virtual monopoly on Russian diamond mines and is the world’s second-largest company by market share, responsible for approximately 30% of global rough diamond production.

Researcher Jeong pointed out the following investment points: △Among the diamond industry value chain segments—rough mining, processing, and precious metal wholesale/retail—mining companies are highly likely to fully benefit from rising rough diamond prices; △Benefits are expected to shift from Alrosa, pressured by sanctions, to other mining companies; and △Pure-players are expected to see more certain growth compared to companies heavily reliant on sales of other minerals.

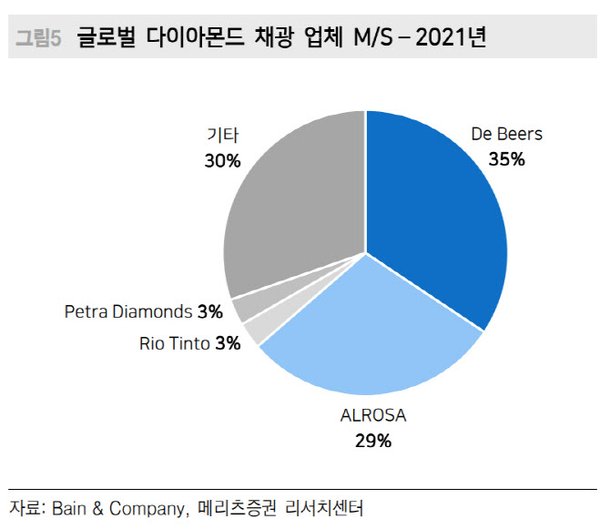

As of last year, the global diamond mining market share was De Beers (unlisted) at 35%, Alrosa at 29%, Rio Tinto at 3%, and Petra Diamonds at 3%. Researcher Jeong stated, “Rio Tinto, which has the same market share as Petra, has a significantly low diamond segment sales proportion at 0.8%, making it difficult to receive additional benefits. In Petra’s case, despite facing its first boom in 10 years, its current multiple is only 2.5 times. If Russia’s geopolitical issues are not resolved, valuation re-rating within the same theme will be prominent.”