Editor’s Note

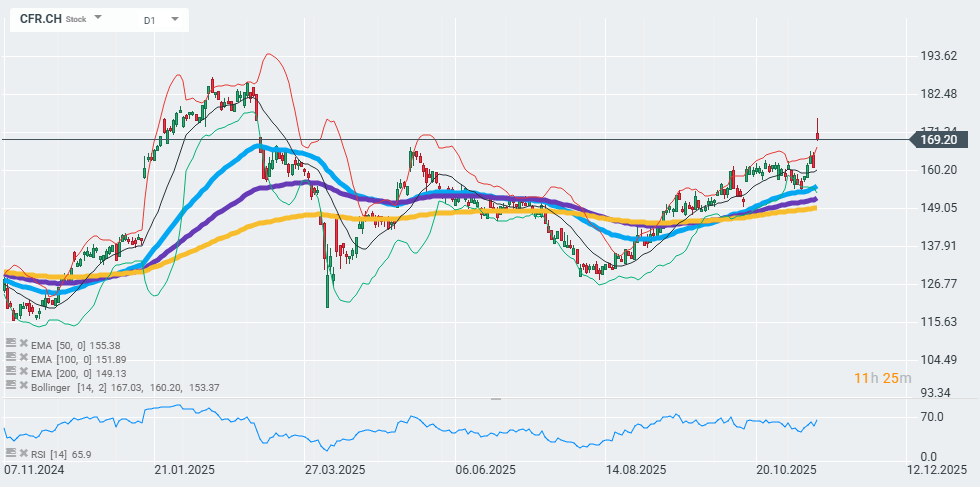

This article highlights Richemont’s strong performance, with sales growth in Q2 and Q3 positioning it as the sector’s fastest-growing company and driving a significant rise in its share price.

Richemont has presented solid results for the second and third quarters of 2025, demonstrating the resilience of its portfolio of luxury brands despite macroeconomic challenges. Sales increased by 10% at constant exchange rates (5% in nominal terms) to reach 10.6 billion euros, significantly exceeding analyst expectations (+6.94% above consensus). The most spectacular growth occurred in the second quarter, when sales increased by 14% at constant exchange rates, confirming Richemont’s position as the fastest-growing company in the luxury sector.

The Jewellery Maisons segment, which includes the brands Cartier, Van Cleef & Arpels, Buccellati and Vhernier, remains the group’s growth engine. Sales in this segment increased by 14% at constant exchange rates (9% in nominal terms) in the first half of the year, with a particularly strong boost in the second quarter, reaching 17%. The operating margin remained at an impressive 32.8%, despite the significant challenges posed by rising gold prices. The success of this segment reflects a fundamental shift in luxury consumption:

Sales growth in the Americas (+18% at constant exchange rates) and Europe (+11%) drives overall results, while the Asia-Pacific region shows signs of recovery, especially in China, Hong Kong and Macao, which returned to growth in the second quarter.

The Specialist Watchmakers segment (A. Lange & Söhne, Jaeger-LeCoultre, IWC, Panerai, Piaget, Vacheron Constantin and others) remains under pressure. Sales fell by 2% at constant exchange rates (6% in nominal terms), although a recovery was observed in the second quarter with growth of 3% at constant exchange rates. The operating margin fell sharply to 3.2% from 9.7% the previous year, as a result of a combination of unfavorable currency fluctuations, rising gold prices and US tariffs. Demand in China, Hong Kong and Macao remains weak, although some improvement was observed in the second quarter.

Net profit amounted to 1.8 billion euros, 297% higher than the previous year (compared to 457 million euros the previous year, which included extraordinary amortizations), and cash flow from operating activities increased by 48%, reaching 1.854 billion euros. The consolidated cash position was 6.5 billion euros, providing financial flexibility to continue investing in brand growth. Despite the solid results, the outlook remains cautious. Chairman Johann Rupert emphasized that:

Chinese consumers are becoming increasingly selective, a trend that could persist even after the economy has fully recovered. The gross profit margin decreased by 190 basis points, standing at 65.3% from 67.2% the previous year, reflecting the combined impact of unfavorable currency fluctuations, rising raw material prices (particularly gold) and US import tariffs, estimated at 300 million euros (approximately 349 million dollars) for the full year.