Editor’s Note

The luxury sector is navigating a complex year marked by divergent stock market trends and business performance. While analysts describe 2025 as a pivotal “make or break” period, many anticipate a stronger second half. This analysis examines the underlying dynamics and what lies ahead for the industry.

The luxury sector is poised to close a mixed year in terms of both stock market performance and business activity. However, UBS believes the worst is over and expects an acceleration in the second half. Deutsche Bank, for its part, refers to it as a “make or break” year.

Luxury is about to turn the page on a mixed 2025 in the stock market. Or more precisely, in two phases.

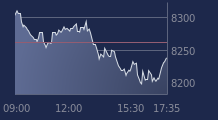

The trajectory of LVMH‘s stock, often considered the key barometer of the sector due to the diversity of its businesses, attests to this. By the end of June, the share price of the world’s number one in the sector was down 30% for the entirety of 2025. The subsequent rebound has been all the more spectacular.

The stock has recovered 44% since the end of June and is now trading close to breakeven for 2025 (-1.2%).

The luxury sector experienced a complicated first half, continuing the trend from the latter part of 2024. The low point was reached in the second quarter when LVMH reported a 9% drop in comparable revenue for its flagship “Fashion & Leather Goods” division.

The sector was penalized by a series of headwinds, including economic uncertainty caused by the Trump administration’s tariffs and unfavorable trends (at least in the spring) in the US markets, which weighed on demand. As François-Henri Pinault, then CEO of Kering, reminded in May, consumer spending in the United States is highly correlated with the health of Wall Street, regardless of the consumers’ “social class.”

Hope re-emerged around September when the first encouraging signals were recorded, particularly in the United States, based notably on credit card data.

The third-quarter earnings season then reinforced this renewed optimism. LVMH, Kering, but also Italian Salvatore Ferragamo and Swiss Richemont, owner of Cartier and Van Cleef & Arpels, significantly exceeded expectations. These groups soared on the stock market following their publications (+12.2% for LVMH, +8.7% for Kering, +13.3% for Salvatore Ferragamo).

For Bank of America, the activity reported by luxury companies in the third quarter sent “first positive signals,” notably with a return to positive growth in “Asia ex-Japan” (and thus in China).

Will 2026 be the year of the long-awaited renewal for the sector? UBS certainly seems to think so.

The Swiss bank is approaching next year with a less cautious stance and believes “the worst is behind us.” It anticipates a rebound in the sector’s comparable growth to 5% after a 1% decline in 2025, while the average operating margin would rise to 21.3%, up half a percentage point.

Admittedly, the recovery is still in its early stages. And the new introductions by luxury groups will only bear most of their fruit in the second half of 2026, according to the institution.

UBS believes the bulk of the acceleration will occur in the second half of 2026. This is due to “the usual time lag in the fashion industry between the debut of artistic directors on the runway” and the ramp-up of sales for new collections, notes the bank.

Since these first shows took place in the second half of 2025, “the effective arrival of new products in stores” will happen “probably in the first half of 2026,” it continues.

After two years of decline, volumes are expected to rise again thanks to this creative momentum, with UBS forecasting 3% growth in 2025.

By region, the Swiss bank anticipates growth increases of 6% for the Chinese “cluster” (domestic and overseas luxury spending), 7% for Americans, and 6% for Europeans.

UBS also estimates that the dominance of understated luxury (the famous “quiet luxury” in English), with its minimalist aesthetic, could waver.