Editor’s Note

The recovery of China’s travel retail sector highlights shifting consumer habits and the growing integration of online and offline shopping. As detailed in the latest industry white paper, this evolution is reshaping the duty-free landscape and fueling broader economic momentum.

As the domestic tourism market continues to recover, China’s travel retail industry is accelerating its return to a growth trajectory. Recently, as a representative enterprise in China’s travel retail industry, China Duty Free Group (CDFG) officially released the “2024-2025 CDFG Consumption White Paper” (hereinafter referred to as the “White Paper”). Data shows that China’s GDP has returned to healthy growth after a phased adjustment, with policy effects and expanding domestic demand jointly stabilizing consumer confidence, providing solid ground for the travel retail industry. Meanwhile, with changing consumption habits, the new consumption loop of “online ordering + offline experience” is redefining the spatial and temporal dimensions of duty-free shopping.

The White Paper shows that thanks to the combined forces of international tourism recovery, policy support and market opening, the rise of emerging markets, and digital transformation, industry vitality continues to be unleashed. In 2024, the global duty-free and travel retail market size reached USD 74.13 billion, a year-on-year increase of 3%, recovering to 85.8% of the 2019 level.

Image source: “2024-2025 CDFG Consumption White Paper”

Simultaneously, China’s GDP has returned to healthy growth after a phased adjustment. Policy effects and expanding domestic demand have jointly stabilized consumer confidence, providing solid development ground for the domestic travel retail industry. Especially with the deep advancement of the Hainan offshore duty-free policy and the downtown duty-free shop policy, the growth of domestic and international tourism and the increase in inbound consumption are continuously driving the expansion of the domestic market.

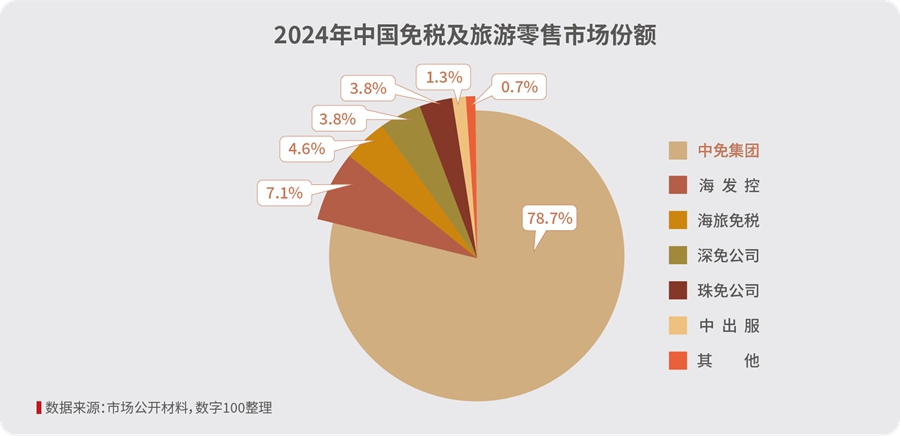

With the recovery of the domestic market, the trend of resource integration in China’s travel retail industry has become increasingly apparent. The aggregation effect of leading enterprises continues to be prominent, and industry concentration shows a steady upward trend. The White Paper shows that, driven comprehensively by advantages in omni-channel layout, supply chain, member value management, capital, and technology, CDFG continues to consolidate its leading position in the industry with a 78.7% market share. By synergizing efforts around flagship store economy, new product launches, full-domain marketing, and service upgrades, it has built a multi-level, strong-experience “duty-free + culture & tourism” consumption new ecosystem, achieving higher-quality development over the past year together with numerous partners.

Image source: “2024-2025 CDFG Consumption White Paper”

Using “duty-free+” as a pivot, CDFG is upgrading duty-free shopping spaces into cultural and tourism destinations that are visitable, playable, and shareable. By actively responding to consumer shopping expectations, CDFG’s user base has achieved breakthrough growth. The White Paper shows that by June 2025, the number of CDFG members had exceeded 45 million. On the basis of stable overall growth and healthy structural adjustment, CDFG’s member group exhibits three new characteristics: a solid foundation in both mass and high-luxury segments, men becoming an important growth pole for high-end consumption, and the increasing pulling power of the silver-haired population.

Image source: “2024-2025 CDFG Consumption White Paper”

As China’s travel retail market transforms towards high-quality development, structural changes in consumer groups have become a core signal of industry transformation. The traditional logic of “wide coverage” is gradually being replaced by “precise” niche operation. Based on core dimensions such as consumption contribution, category preference, age stratification, and geographical distribution, CDFG has deconstructed its core customer groups into nine major sub-categories. Each niche carries clear demand labels, accurately covering consumption demands in different scenarios, outlining a diverse picture of travel consumption: 31-45-year-old “Refined Self-Indulgers” from first- and second-tier cities focus on high-end skincare; high-net-worth “Luxury Lifestyle Enthusiasts” prefer watches and jewelry; “Town Elites” from third- and fourth-tier cities are pragmatic and pursue quality; 31-50-year-old male “Wine Connoisseurs” are keen on high-end wines; 21-35-year-old “Tech Enthusiasts” focus on tech products; 16-30-year-old Gen Z “Fashionable Wellness Advocates” follow makeup trends; 60+ “Silver-haired Premium Enjoyers” prioritize health consumption; 26-45-year-old “Sports Enthusiasts” choose professional equipment; foreign travelers favor Chinese characteristic goods.

Image source: “2024-2025 CDFG Consumption White Paper”

The distinct consumption preferences of the nine customer groups not only provide precise “user navigation” for CDFG’s category planning, marketing activities, and service optimization but also drive the entire travel industry to leap out of the traditional “mass-market” model and enter a new stage of “precise reach, deep operation” niche cultivation, injecting more segmented and vibrant growth momentum into consumption upgrading.

In recent years, domestic brands have achieved brand premium breakthroughs in the travel retail market through product innovation and cross-border collaborations. The pursuit of “Guochao” (China-chic) goods by young consumer groups is changing the long-term pattern dominated by international brands in the travel retail market, forming new value growth points. With changing consumption habits, the increase in experiential elements such as immersive displays and art installations is also upgrading duty-free shopping from product consumption to content consumption. Transforming from product suppliers to lifestyle content providers has become a long-term value that travel retail operators cannot ignore. The White Paper shows that the boundaries between online and offline channels in travel retail are blurring. Innovative measures such as AR/VR technology applications and online-exclusive SKUs are building a new consumption loop of “online ordering + offline experience.” This integration not only improves conversion efficiency but also redefines the spatial and temporal dimensions of duty-free shopping.

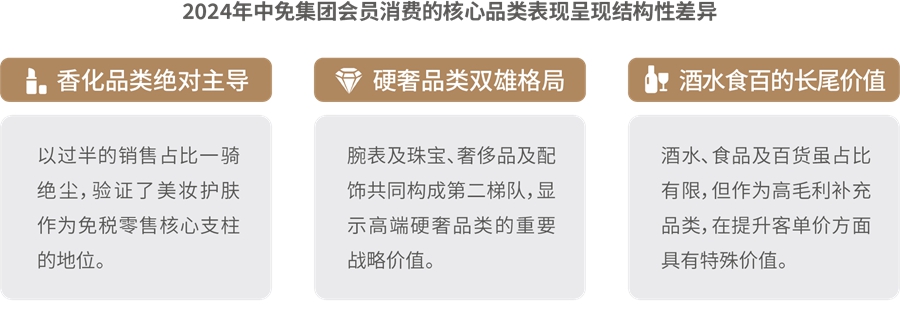

In terms of core category consumption dimensions, makeup and fragrance show bright growth, with foreign tourists, male customer groups, and domestic trendy brands becoming important growth points for the category. In luxury goods and accessories, the consumption structure is diversifying, with significant growth in the ultra-high-end market and stable demand in the affordable luxury segment. In watches and jewelry, category differentiation is significant, with the jewelry category showing year-on-year growth and watch demand exhibiting prominent regional characteristics. In wines and spirits, the market is expanding and upgrading, with significant stratification in categories and consumer groups, and complementary channel development, showing the parallel characteristics of scale expansion and structural upgrading. In food and general merchandise, the market is steadily expanding with distinct niche characteristics. Gen Z and the silver-haired population are triggering new emotional and health consumption changes.

Image source: “2024-2025 CDFG Consumption White Paper”

On one hand, policy dividends continue to be released. The countdown to Hainan’s island-wide customs closure operation by the end of 2025 has begun, and downtown duty-free shop pilots are expanding to more core cities, opening up incremental space for the market. On the other hand, consumption demand shows characteristics of stratified upgrading. The differentiated needs of different customer groups give rise to structural opportunities in categories. The “diversified demand-driven” model will make the development of the domestic travel market more resilient.

Currently, CDFG has formed a product matrix covering all categories including luxury goods, fragrance & cosmetics, tobacco & alcohol, etc., with over 360,000 SKUs, and successfully introduced more than 200 new brands in 2024, exclusively launching over 500 global limited-edition products across 19 series. In the future, CDFG will take the digital-intelligent ecosystem as its core focus, deepening the integration of “duty-free + culture, commerce, sports, tourism, and wellness”—combining art exhibitions, sports events, and celebrity performances for joint marketing to create immersive consumption experiences. Simultaneously, it will continue to be customer-centric, conveying the brand value of “Bringing You the Beauty of the World” through stratified operation, supply of scarce goods, and omni-channel services, promoting high-quality development of the industry.