Editor’s Note

This analysis examines a strategic pivot at Chow Tai Fook, where the core business logic is shifting from direct jewelry sales to a capital-light franchise model focused on platform service fees.

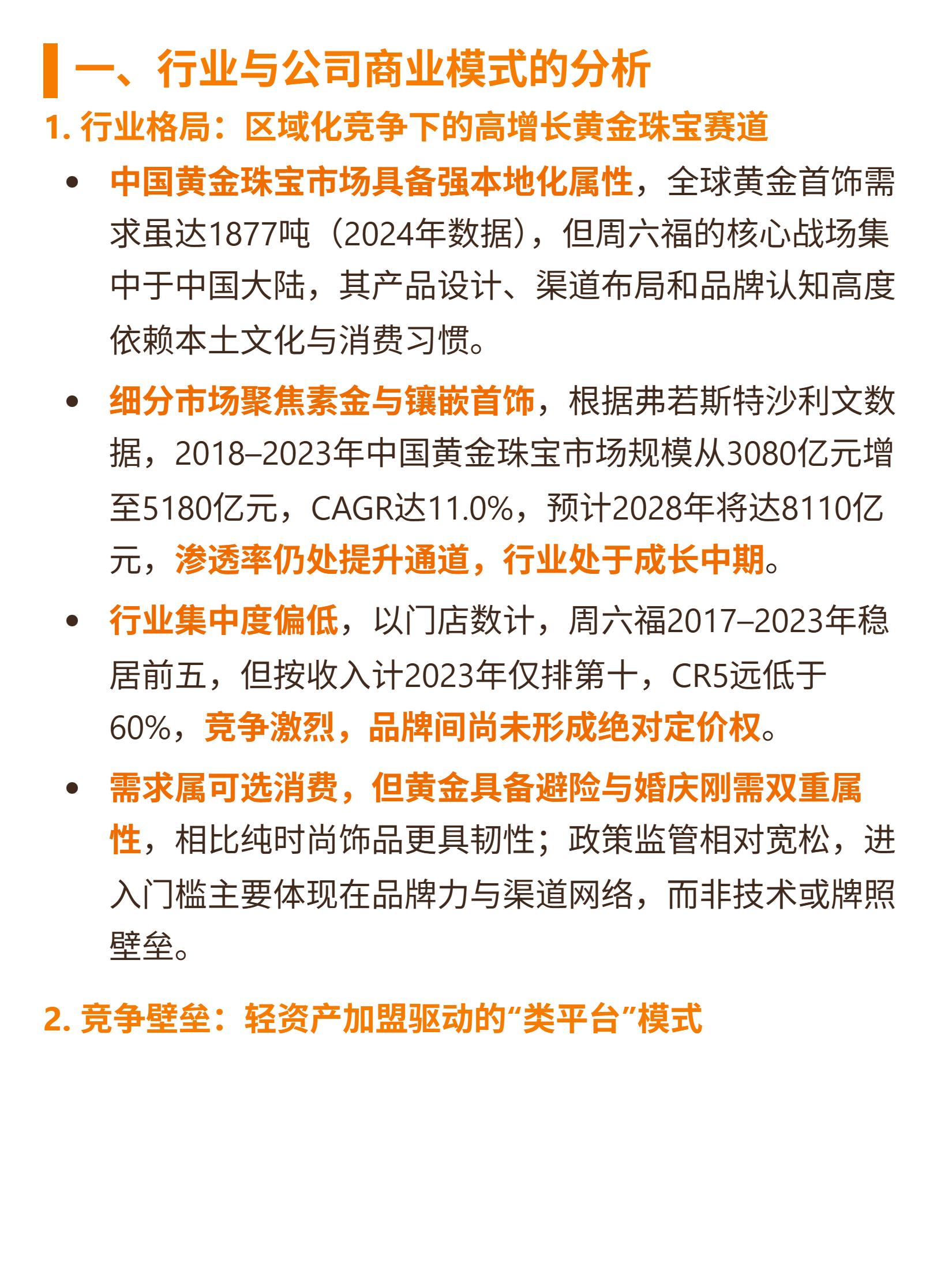

Recently, Chow Tai Fook (Saturday) has been studied, with its core logic being the shift from “selling jewelry” to a capital-light franchise model centered on “collecting platform service fees.”

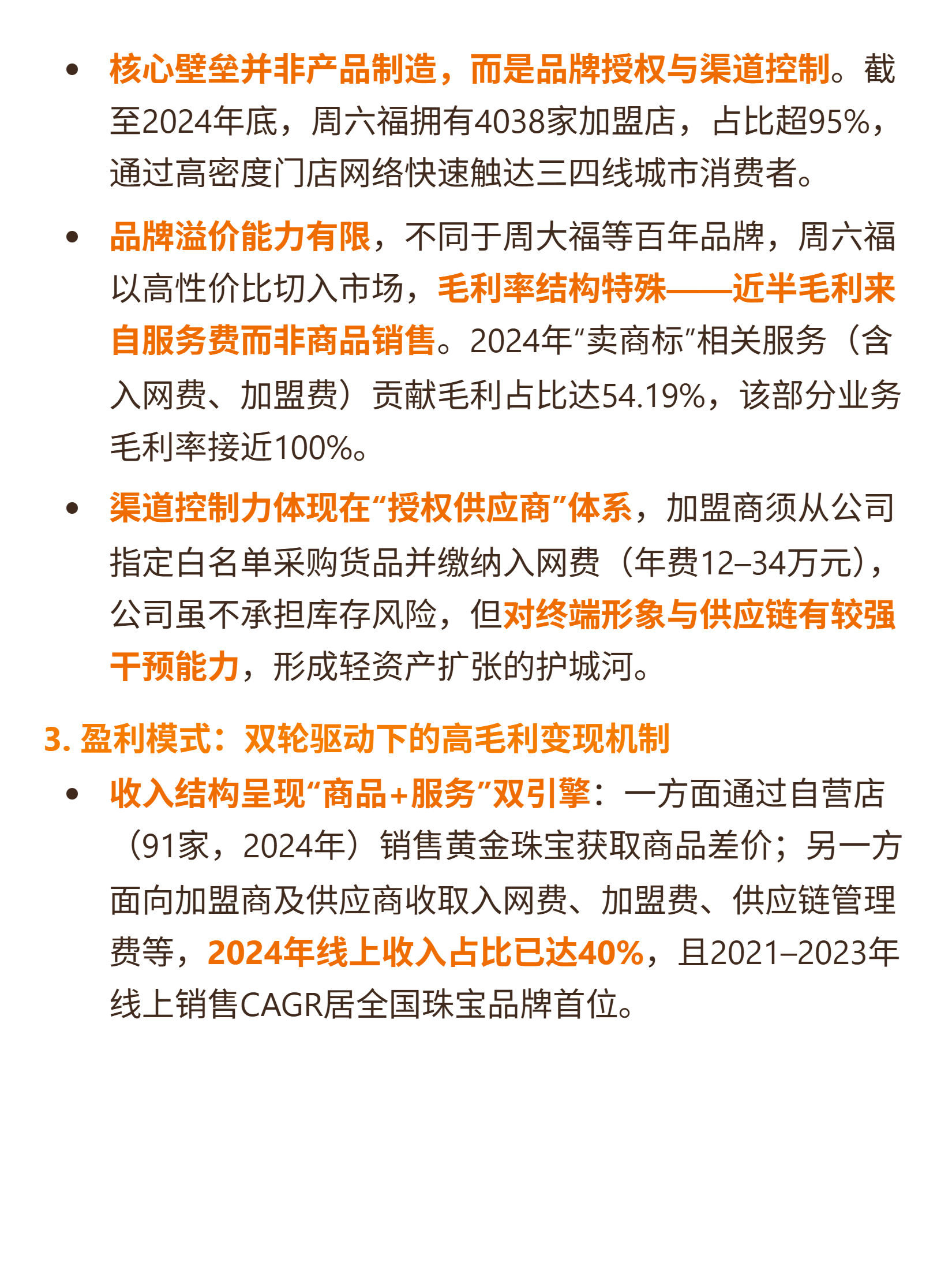

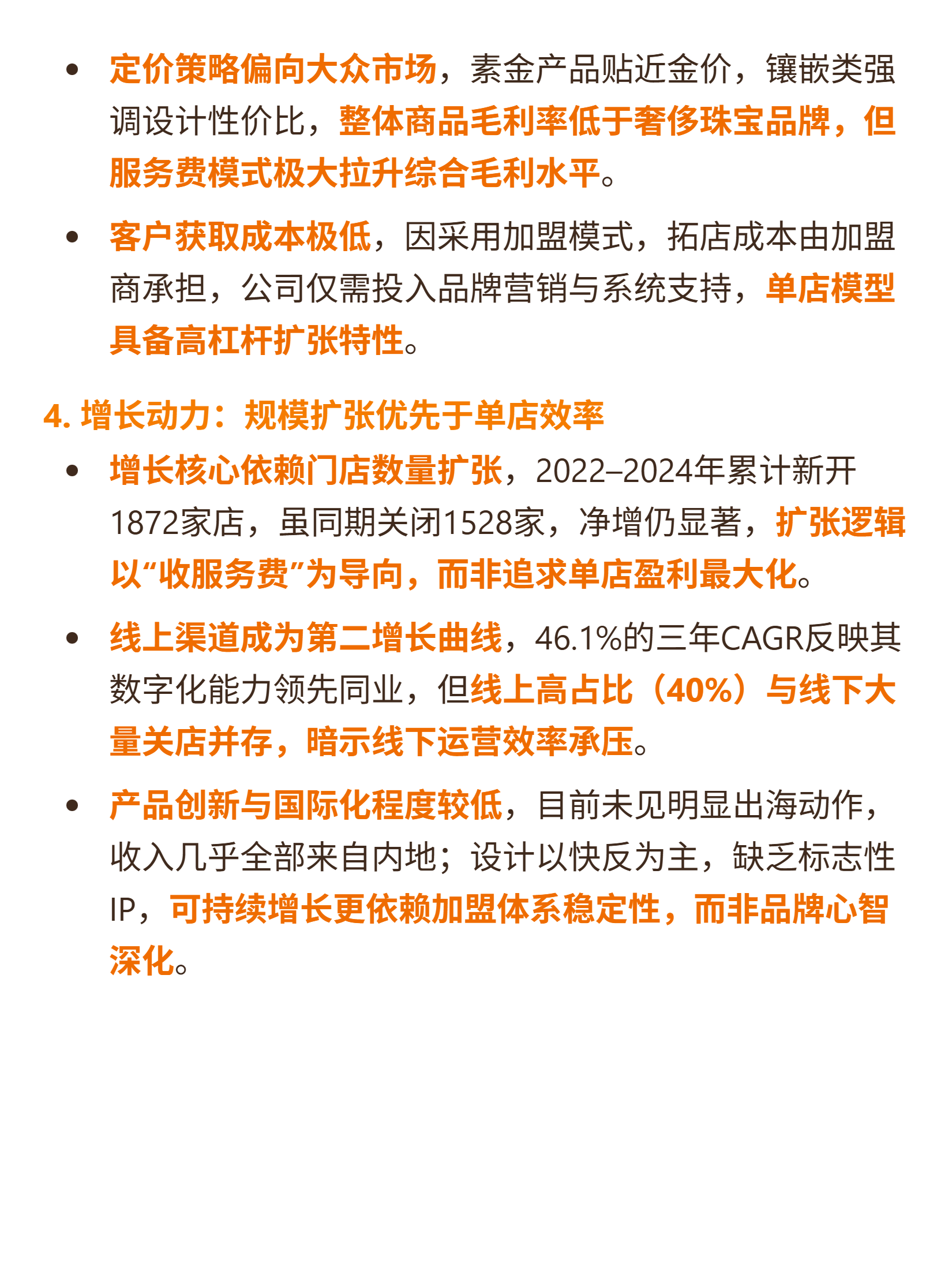

Over 95% of its stores are franchised. Revenue is driven by a dual-engine model of “product sales + service fees.” Service fees (including network access fees, franchise fees, and supply chain management fees) contribute nearly half of the gross profit (54.19% in 2024, with a gross margin close to 100%). Products primarily consist of high-value-for-money plain gold and inlaid jewelry. In 2024, online revenue accounted for 40% of total revenue, with an online CAGR of 46.1%, ranking first in the industry.

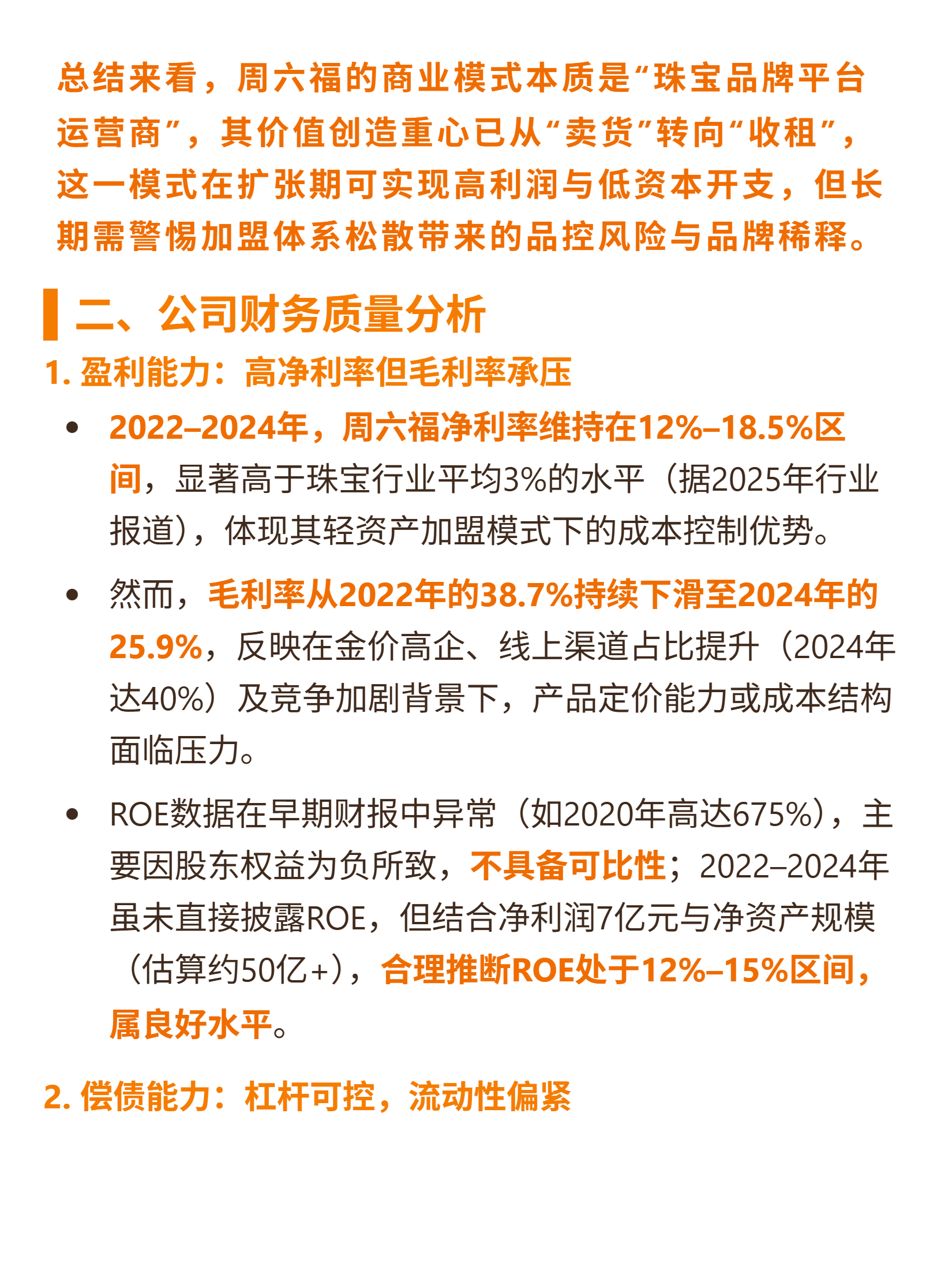

From 2022 to 2024, revenue increased from 3.1 billion to 5.719 billion (CAGR 35.8%), and net profit grew from 575 million to 706 million (CAGR 10.8%). The net profit margin ranged from 12% to 18.5% (significantly higher than the industry average of 3%). However, the gross margin declined from 38.7% to 25.9% (impacted by high gold prices and the increasing proportion of online sales). In 2024, dividends paid amounted to 645 million, nearly equivalent to the full-year net profit.

Growth relies on store expansion (1,872 new stores cumulatively from 2022 to 2024) and online channels. However, the franchise model warrants caution regarding product quality control risks. While high dividends enhance shareholder returns, they may weaken the reinvestment capacity for new store expansion post-IPO. The continuous decline in gross margin requires attention to the sustainability of the “volume-for-price” strategy.

The above covers company and industry analysis along with financial data analysis from the past five years.