Editor’s Note

This analysis highlights a significant 19.7% surge in Japan’s domestic import retail market for 2024, driven primarily by robust inbound tourism fueled by a weak yen and increased spending from affluent domestic consumers.

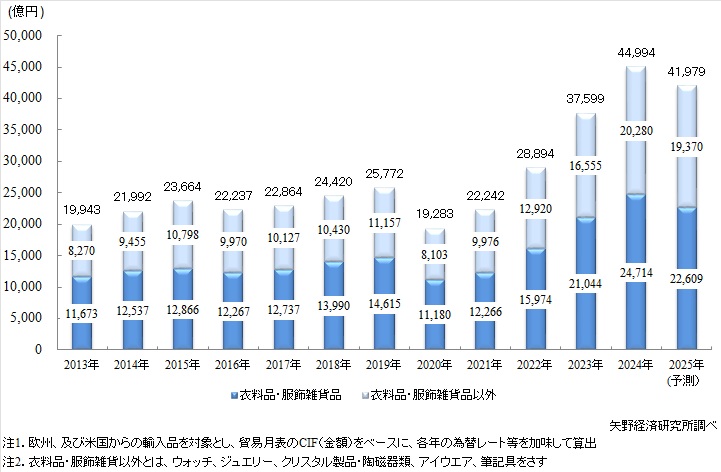

The retail market size for domestic import brands (15 major item categories) in 2024 is estimated at 4,499.4 billion yen, a 19.7% increase year-on-year. The expansion of the market in 2024 is considered to be largely contributed by the increase in inbound (visiting foreign tourists) demand against the backdrop of a weak yen, in addition to increased consumption by domestic affluent individuals amid rising stock prices.

According to statistics released by JNTO (Japan National Tourism Organization), the number of inbound visitors to Japan in 2024 reached a record high of 36.87 million, a 47.1% increase year-on-year. The retail market size of the inbound segment within the import brand market in 2024, as calculated by our company, is estimated to have increased by 181.9% compared to 2023. Since the COVID-19 pandemic, there has been a trend where shopping in Japan has become a primary purpose for inbound tourists against the backdrop of a sharply depreciating yen, leading to a situation where spending growth outpaces the increase in visitor numbers. The expansion of inbound spending in 2024 is considered to be influenced by the increase in the number of Chinese inbound tourists. The high purchasing power of Chinese inbound tourists is also reflected in the “Survey of Foreign Visitors’ Consumption Trends” published by the Japan Tourism Agency, where per capita shopping expenses significantly exceed those of other nationalities, a trend similarly confirmed through interviews with various brands. The number of Chinese inbound tourists, which had been slow to recover since the pandemic, surged by 287.9% year-on-year in 2024 (source: JNTO), which is considered to have greatly contributed to the expansion of this market size.

On the other hand, the rapid expansion of inbound demand has brought various impacts to the market. The sharp increase in inbound tourists resulted in long queues daily at popular boutiques in city centers, leading to an increase in Japanese customers who avoided shopping in crowded stores with constant entry restrictions. Furthermore, operational challenges surfaced, such as brands experiencing opportunity losses due to insufficient inventory and staff burnout from the busy period. In response to this situation, various brands have been seen taking countermeasures, such as strengthening inventory management systems and reviewing staffing arrangements.

Continued price increases for goods directly linked to cooling consumption among the middle class and younger generation.

Price increases for goods continued in 2024, due to rising costs of raw materials, labor, and transportation since the COVID-19 pandemic, as well as the impact of the sharply progressing yen depreciation.

Looking at the price increase situation among the brands covered in our survey, the average price increase in 2024 was slightly over 10%, with considerable variation ranging from 5% to 20% depending on the brand. Overall, jewelers had higher price increase rates, and, with some exceptions, more popular brands tended to have higher increases. While the magnitude of price increases was larger in 2022 and 2023 for any brand, continuous price increases since 2021 have resulted in product prices reaching levels more than 1.5 times those before the pandemic (2019).

Even for popular brands favored by the younger generation and middle class due to their “resale value,” it appears they were perceived as having reached price points that made purchase difficult. A trend spread where brands that showed strong sales performance until the first half of 2024 (January-June) experienced a slowdown in sales in the second half (July-December).

Entering 2025, changes have occurred in the consumption trends of inbound tourists. Despite the continued increase in the number of inbound visitors to Japan (source: JNTO), consumption of luxury brands is decelerating.

There are several factors for the slowdown in inbound demand, but the largest is considered to be the shift in the exchange rate towards a stronger yen trend. The tariff policies by the US Trump administration, which took office at the beginning of 2025, caused fluctuations in the stock market and a shift towards a stronger yen trend. Furthermore, concerns about the worsening Chinese economy amid continued economic stagnation have led to a significant decrease in spending on luxury goods by Chinese inbound tourists.

Another factor that can be cited is the increase in product prices. Price increases over the past few years have narrowed the price gap between domestic and international markets, diminishing Japan’s price advantage depending on exchange rate fluctuations.

In 2025, due to the slowdown in inbound demand, many brands are expected to underperform compared to their 2024 results. The negative impact is greater for major luxury brands that benefited more from inbound demand. Additionally, price increases have dampened demand from general consumers, and even among the affluent individuals supporting the market, there is a sense that consumption of goods has run its course. Excluding items with asset value, a trend of selective consumption is being observed. Although stock prices, which significantly influence the consumption trends of the affluent, have been rising since the summer of 2025, the uncertainty surrounding the future of the global economy remains a concern.

Based on the above, the retail market size for domestic import brands (15 major item categories) in 2025 is forecasted to be 4,197.9 billion yen, a 6.7% decrease year-on-year. The import market, which continued to expand against the backdrop of a sharply depreciating yen, is predicted to enter an adjustment phase from 2025 onwards.

Survey Outline

1. Survey Period: May – August 2025

2. Survey Subjects: Trading companies, manufacturers, retailers importing and selling European and US apparel, fashion accessories, watches, jewelry, crystal products/ceramics, eyewear, and writing instrument brands, as well as Japanese subsidiaries of various import brands.

3. Survey Method: Direct interviews (including online) by our specialist researchers, telephone hearing surveys, and literature research.

About the Import Brand Market

In this survey, the import brand market refers to the market size for import brands (15 major item categories), which adds 5 items to the previously calculated import brand market size (10 major item categories).

The 15 major item categories are: ① “Ladies’ Wear”, ② “Men’s Wear”, ③ “Baby Wear”, ④ “Bags & Leather Goods”, ⑤ “Shoes”, ⑥ “Neckties”, ⑦ “Scarves, Shawls, Handkerchiefs”, ⑧ “Leather Apparel”, ⑨ “Belts”, ⑩ “Gloves”, ⑪ “Watches”, ⑫ “Jewelry”, ⑬ “Crystal Products & Ceramics”, ⑭ “Eyewear”, ⑮ “Writing Instruments”. All items are imports from Europe and the United States.