Editor’s Note

This article highlights a positive shift in the jewelry market, with a forecasted return to growth in FY2021. The analysis by Teikoku Databank points to emerging signs of recovery after a challenging period.

Teikoku Databank conducted a survey and analysis on the outlook and future prospects of the jewelry market for fiscal year 2021.

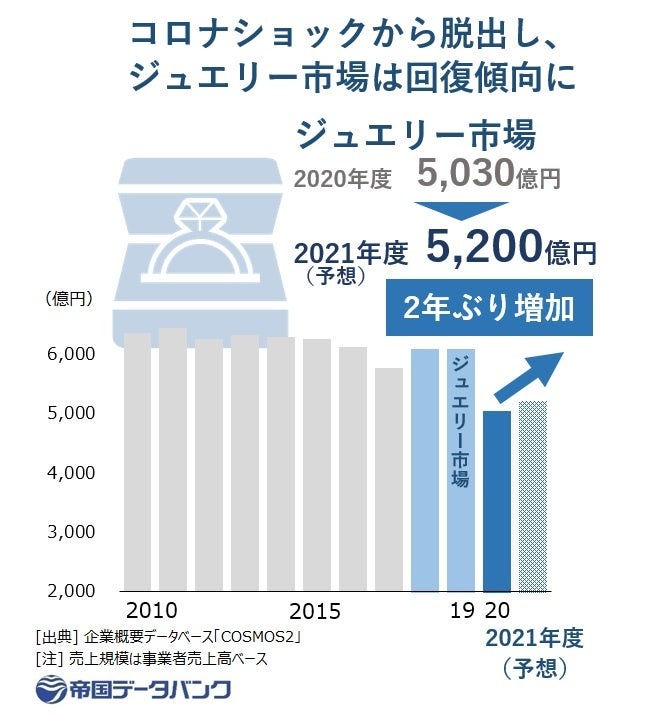

Signs of recovery are emerging in the jewelry market, which was significantly impacted by the COVID-19 pandemic. According to Teikoku Databank’s survey, the jewelry market (based on corporate sales) for FY2021 is projected to be around ¥520 billion, potentially exceeding the previous year’s figure. While this represents a nearly 20% decrease from pre-COVID-19 levels (FY2019), which benefited from robust inbound demand, the market is recovering from the severe blow suffered in FY2020.

FY2020 saw the disappearance of inbound sales, which accounted for a large portion of revenue. Due to restrictions on movement, including states of emergency, in-person sales at department stores and shopping malls were hampered, leading to a sharp drop in customer traffic. In contrast, FY2021 saw revenge spending, primarily among the middle and affluent classes. Against a backdrop of rising stock prices, sales of high-priced items were strong. The introduction of e-commerce and online sales also progressed, with customer acquisition through mail-order channels proceeding smoothly, raising expectations for further business recovery. However, the recovery was polarized, with popularity skewed towards high-end, expensive jewelry, while recovery in foot traffic for mid-to-low-priced fine jewelry, previously supported by male gift demand, remained sluggish.

Estimating the FY2021 jewelry market based on corporate performance (including forecasts) up to January 2022 reveals it will be around ¥520 billion, a 3% increase from the previous year. While this is only about half the peak level exceeding ¥900 billion seen in FY2007, business conditions show a recovery trend compared to FY2020, which saw an approximately 20% year-on-year decrease, marking the first year-on-year increase in two years.

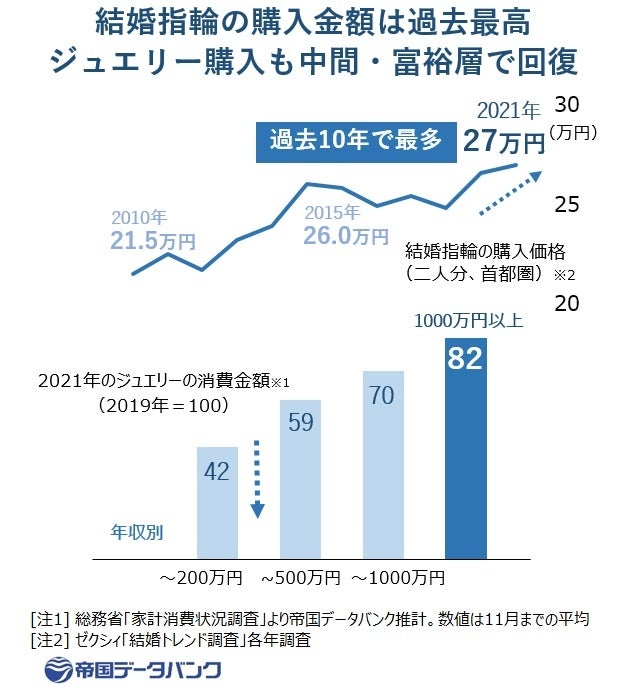

The market expansion is attributed to the recovery of “material consumption” among the upper classes due to a rebound from self-restraint. For instance, changes in preferences are observed, such as purchasing “one grade higher” for bridal accessories like wedding rings. According to Recruit’s “Zexy Wedding Trend Survey,” the average amount spent on wedding rings by couples in the Tokyo metropolitan area was ¥248,000 in 2019, but rose significantly by ¥18,000 to ¥266,000 in 2020. In 2021, it increased further to ¥270,000, the highest purchase amount in the past decade. Despite economic downturns and future anxieties during the pandemic, factors like the ¥100,000 special cash payment and leftover budgets originally intended for weddings and honeymoons boosted spending on bridal accessories.

High-value consumption, centered on the affluent, is also robust. Jewelry consumption in 2021 among middle and affluent classes with annual incomes over ¥10 million saw only a slight decline compared to other income brackets. Although not reaching pre-COVID levels, money that would have been spent on leisure and travel, combined with stock market gains, flowed into high jewelry as “material consumption,” strengthening the trend of rising purchase prices.

Consequently, overseas brands specializing in high jewelry captured more of this 2021 trend towards luxury. LVMH Moët Hennessy Louis Vuitton of France, the luxury group owning U.S. jewelry giant Tiffany, reported double-digit year-on-year revenue growth for the full year 2021, exceeding pre-COVID performance. The watch and jewelry division showed remarkable growth, with the Japanese market also performing strongly, achieving double-digit growth from October onwards. Swiss high jewelry manufacturer Financière Richemont, which owns Cartier and Piaget, also performed well with a 30% year-on-year increase in the October-December quarter.

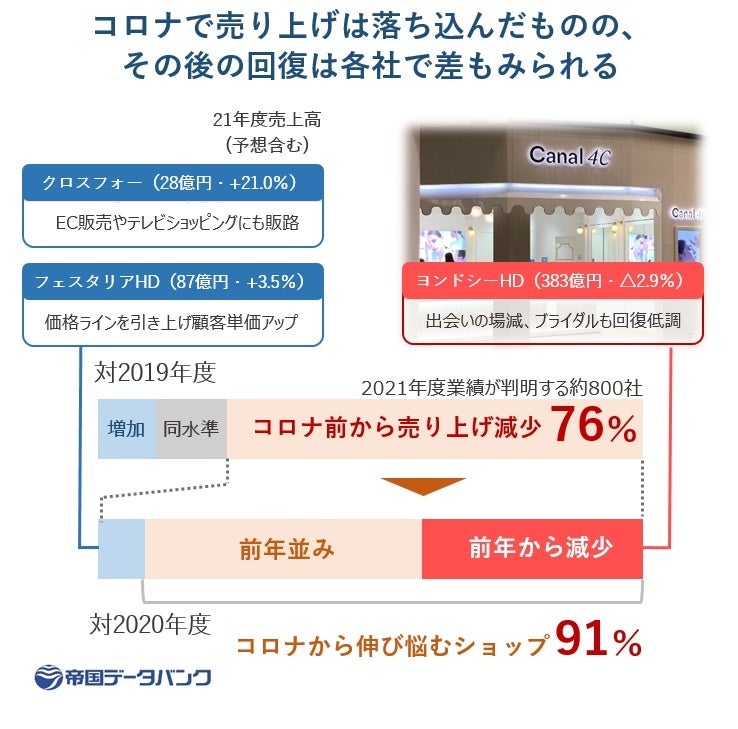

On the other hand, domestic jewelry shops handling more accessible fine jewelry are seeing relatively slower sales recovery. Among jewelry shops with confirmed FY2021 performance, 70% reported decreased sales compared to pre-COVID levels. Furthermore, 90% of these were forced into revenue decline or maintaining the status quo. While Festaria Holdings, which raised its price lines anticipating price polarization and saw a roughly 20% increase in average selling price, and Crossfor, which “focuses on non-contact sales channels” like online shopping and TV shopping, recovered sales from the previous year, many others are struggling to adapt to reduced foot traffic and changing purchase trends due to COVID-19.

Yondoshi Holdings, behind the jewelry brand “Canal 4℃,” revised downward its consolidated earnings forecast for the period ending February 2022 due to the loss of meeting opportunities during the pandemic and

Many jewelry shops also reported that while sales of silver products during the Christmas season increased year-on-year, overall performance did not fully recover. To cope with the shrinking domestic market, many had previously focused on lower-priced segments with expected sales volume, such as men’s gift accessories and bridal jewelry, and are now forced to reconsider their strategies.

Currently, there are many positive developments, such as strong performance during the December bonus and Christmas sales seasons. However, concerns are rising about another demand chill due to the rapidly spreading Omicron variant, with voices expressing anxiety about the future. Some companies are also uneasy about the upcoming Valentine’s Day and White Day sales trends. Furthermore, there is concern that as “experience consumption” like leisure and travel recovers after movement restrictions ease, the material consumption seen in FY2021 will become more selective, leading to worries that

The significant share once expected from inbound (foreign visitors to Japan) purchases before COVID-19 is now difficult to achieve, making capturing domestic middle and affluent classes an immediate challenge.

Amid this, efforts to recover slumped in-store sales are advancing through the creation of sales spaces via “online-offline integration.” Online consultations via video calls from stores and systems allowing orders from websites are becoming widespread. Digitization has expanded mail-order departments and brought benefits such as

Additionally, a pearl specialty store in Tokyo newly launched live commerce targeting China, which received high反响 and showed promising results, with

Whether jewelry shops can seize new opportunities born from the pandemic, such as developing new online businesses, is likely to be a key factor for their future.