Editor’s Note

This analysis of the 2024 hard luxury market reveals a clear divergence: sustained demand for jewelry contrasted with a downturn in watches, a trend underscored by recent financial reports from major industry players.

Looking back at 2024, the fortunes within the hard luxury sector diverged significantly. A somewhat blunt but largely accurate summary of the industry’s annual performance would be: “jewelry struggled upward, while watches fell incessantly.”

The latest holiday season financial report from luxury giant Richemont once again confirms this point. In the third quarter of its fiscal year 2025, ending December 31, 2024, revenue from its jewelry division rose 14% year-on-year to €4.501 billion, now accounting for 71% of the group’s total revenue and continuing to act as the growth engine. In contrast, revenue from the watchmaking division, which houses brands like Vacheron Constantin and IWC, maintained its downward trend, recording an 8% decline to €867 million for the period.

The positive aspect of this data is that the decline narrowed from the 16% recorded in the first half of the year, indicating that Richemont’s watch division has applied the brakes on its descent. However, the concerning aspect is that this division has yet to escape its difficulties in the Chinese market—its revenue decline in the region narrowed from 27% in the previous two quarters to 18% this quarter.

Looking at Kering and LVMH, the former explicitly pointed out during last year’s earnings call that its two major jewelry brands, Boucheron and Pomellato, both saw significant growth. While LVMH does not separately disclose revenue for its jewelry and watch businesses, snippets from earnings calls and senior management changes suggest that its jewelry business is outperforming its watch business. The overall revenue for LVMH’s entire Watches & Jewelry division declined by only 4% in the third quarter of last year.

Swatch Group, the Swiss watch giant with a full-price brand matrix including Breguet, Omega, Longines, and Swatch, tells an even more dramatic story—its net profit in the first half of this year plummeted by as much as 70.5%. Meanwhile, Harry Winston became one of the few brands within the group to avoid a sales decline, thanks to its stable jewelry business.

Data from the Federation of the Swiss Watch Industry (FH) further illustrates the trend. In the first 11 months of 2024, total Swiss watch exports fell by 2.7% year-on-year to CHF 23.9 billion.

In November, Hong Kong, China, and Mainland China, as crucial export destinations for Swiss watches, saw their Swiss watch import values drop by 19.7% and 26.3% respectively, becoming the markets with the largest declines.

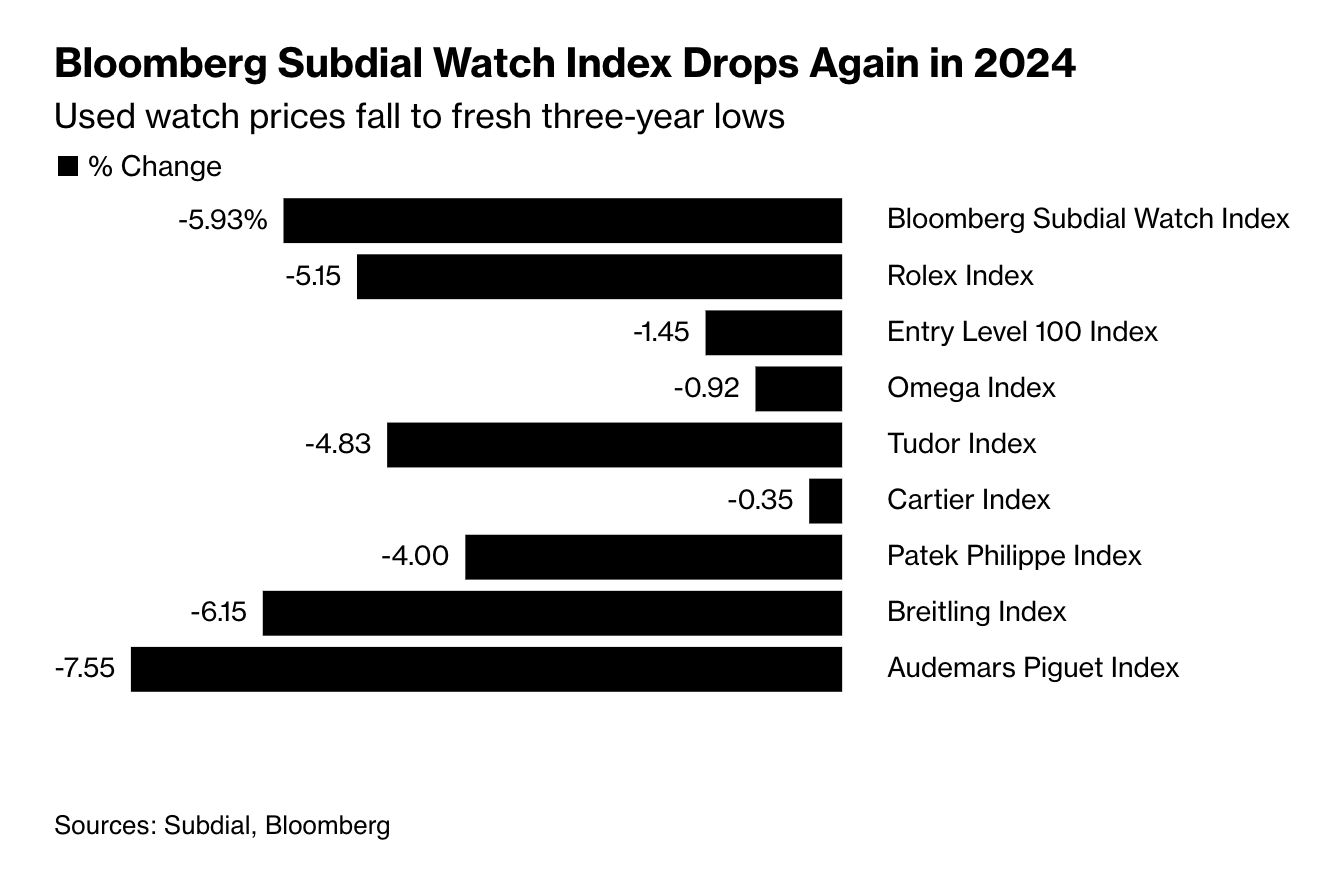

The chill from the primary market has also swept into the secondary market. According to the Bloomberg Subdial Watch Index, a joint venture between Bloomberg and the UK watch trading platform Subdial, the resale price of luxury watches fell by nearly 6% in 2024, hitting a new low since 2021. The resale price indices for popular watches from the three brands considered most investment-worthy and value-retaining—Rolex, Patek Philippe, and Audemars Piguet—fell by 5.15%, 4%, and 7.55% respectively for the full year.