Editor’s Note

The synthetic diamond market is undergoing a seismic shift, with prices collapsing due to oversupply and technological advances. This article explores the profound implications for the global diamond industry and the redefinition of value itself.

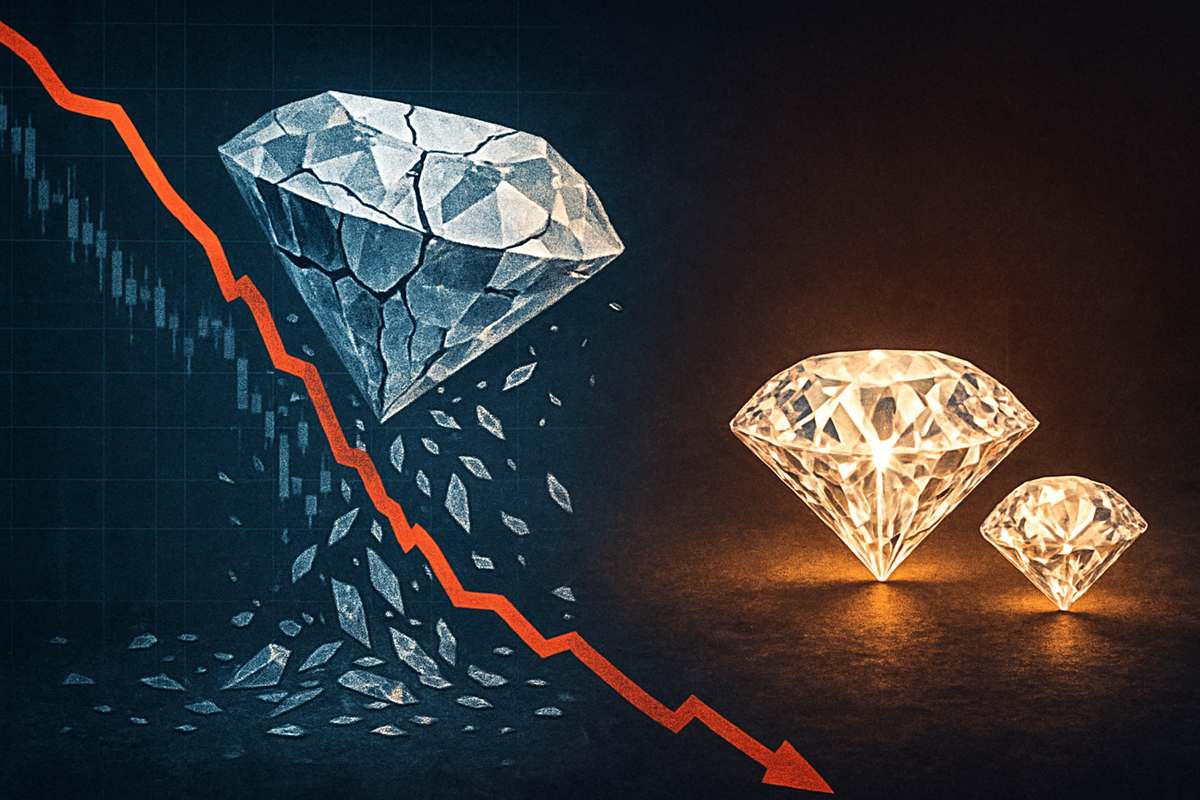

The synthetic diamond market is currently in the throes of a dramatic collapse, with wholesale prices for lab-grown diamonds plummeting by as much as 96% since 2018. This precipitous decline, largely fueled by an overwhelming oversupply and rapid technological advancements in production, is sending shockwaves through the entire global diamond industry. The immediate implications are profound, forcing a fundamental re-evaluation of value propositions, triggering fierce competition for market share, and potentially leading to significant consolidation within the lab-grown sector. While challenging the profitability of synthetic producers, this instability concurrently presents a surprising opportunity for natural diamonds, which are experiencing a renewed surge of consumer interest amidst the volatile landscape of their lab-grown counterparts.

This market upheaval signifies a pivotal moment, as lab-grown diamonds transition from near-premium alternatives to significantly more affordable, mass-market commodities. The long-term effects promise a redefined market structure, altered consumer perceptions, and strategic shifts from all key players, from miners to retailers.

The scale of the synthetic diamond market’s devaluation is stark. Wholesale prices for a one-carat lab-grown diamond, which commanded approximately $4,200 in 2018, have crashed to as low as $168 by 2025 – an astonishing 96% reduction. Two-carat stones have experienced a similar percentage decline. More recently, in the 12 months leading up to November 2024, prices for loose lab-grown diamonds saw a 20% decrease. By 2025, lab-grown diamonds are approximately 83% less expensive than natural diamonds of comparable size and quality, with some industry experts predicting further price drops of 50% to 80%, suggesting the market has yet to find its bottom.

The timeline leading to this collapse is relatively swift. The rapid expansion of manufacturing capabilities, particularly in regions like China and India, has flooded the market with lab-grown gems. This massive oversupply, coupled with continuous advancements in High-Pressure High-Temperature (HPHT) and Chemical Vapor Deposition (CVD) technologies, has made production increasingly efficient and cost-effective. These technological leaps, while beneficial for production scalability, inadvertently stripped producers of pricing power, transforming what was once a controlled luxury item into a mass-produced commodity. The relatively low entry threshold into the lab-grown market initially attracted numerous participants, leading to market saturation and intense competition, forcing companies to continually lower prices to secure sales.

Key players and stakeholders involved span both sides of the diamond divide. In the lab-grown sector, numerous producers, particularly those who invested heavily in scaling production, are now facing severe profitability challenges. On the natural diamond side, major players like De Beers (LSE: DEB) and nations forming the “Luanda Accord” (Angola, Botswana, Democratic Republic of Congo, Namibia, South Africa) are deeply affected. Consumers, whose perceptions of value and authenticity are shifting, are also critical stakeholders.

Initial market reactions have been varied but decisive. The lab-grown industry is grappling with the prospect of significant consolidation, as only the most efficient or vertically integrated grower-manufacturers may survive. There’s a growing consensus that lab-grown diamonds are being relegated to the realm of fashion jewelry, losing their competitive edge in the emotionally charged bridal and luxury markets. This shift also undermines consumer trust in synthetic gems as stores of value. Conversely, the instability in the lab-grown market has sparked a resurgence of interest in natural diamonds. The natural diamond industry, which had experienced a price slump since mid-2022, is now seeing renewed appeal. However, the success of lab-grown diamonds has also exerted significant downward pressure on natural diamond prices, which fell by approximately 40% over the past two years. In response, the natural diamond industry is implementing strategic initiatives, such as the Luanda Accord, where major producing nations have agreed to allocate 1% of annual sales revenue towards collective marketing campaigns to promote natural diamonds.

The dramatic collapse of the synthetic diamond market is creating a clear delineation of potential winners and losers across the entire diamond industry. Companies heavily invested solely in lab-grown diamond production, particularly those without vertical integration or significant differentiation, are facing immense pressure. Many smaller and less efficient producers are likely to be forced out of the market or acquired, leading to significant consolidation. Their business models, predicated on higher margins that no longer exist, are unsustainable. The perception of lab-grown diamonds as rapidly depreciating fashion accessories, rather than valuable heirlooms, further erodes their long-term market position and consumer confidence.

Conversely, the natural diamond industry, after a period of price adjustments and uncertainty, is showing signs of renewed strength. Companies like De Beers (LSE: DEB) and Alrosa are navigating this new landscape.