Editor’s Note

This article cites official data showing record-breaking gold, silver, and jewelry consumption in China for 2025. Readers should note a minor discrepancy between the reported year-on-year growth rate and a direct calculation based on absolute values, a common occurrence in statistical reporting due to factors like rounding or revisions. The core trend of robust growth remains clear.

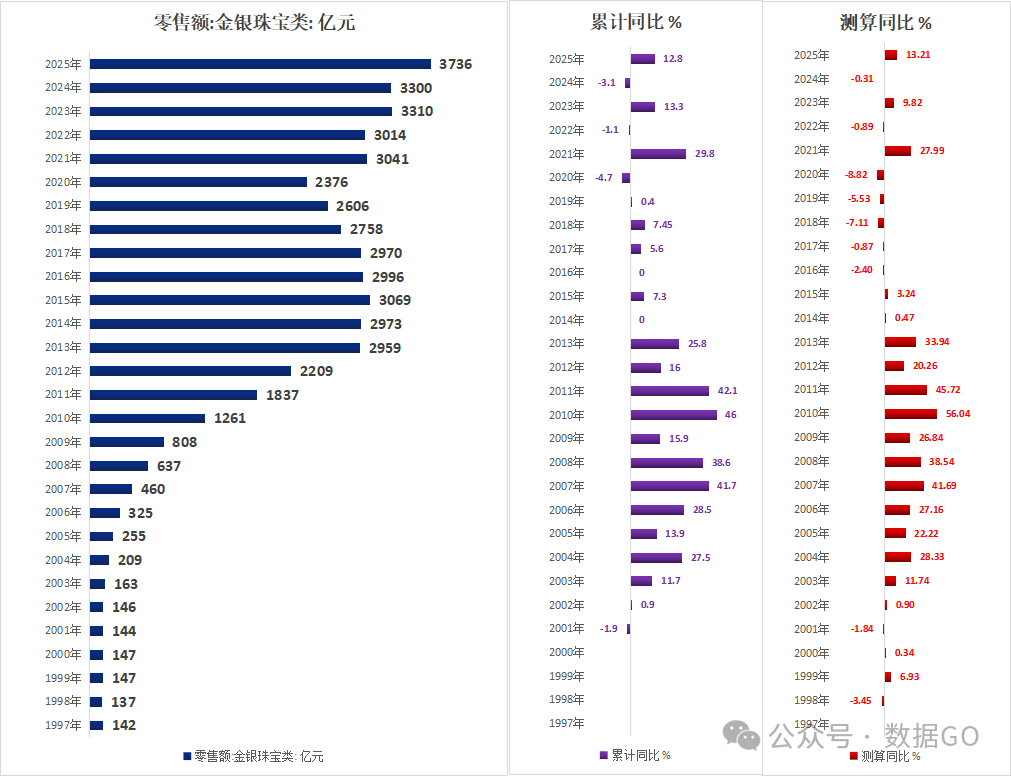

According to data from the National Bureau of Statistics, gold, silver, and jewelry consumption in China’s total retail sales of consumer goods reached 373.6 billion yuan in 2025, hitting a record high with a year-on-year increase of 12.8%. If compared directly by absolute value, the increase is 13.21%, showing a certain discrepancy from the published figure.

Analyzing from the three dimensions of retail sales, cumulative year-on-year growth, and estimated year-on-year growth, the gold and jewelry industry exhibits a clear long-term growth trend. However, influenced by macroeconomic factors, the pandemic, gold prices, and other elements, it shows distinct cyclical fluctuation characteristics, returning to a high-growth trajectory in 2025.

Retail sales were only 14.2 billion yuan in 1997, reaching 373.6 billion yuan in 2025, representing approximately a 26-fold increase over 28 years. The overall trend shows a stepwise rise, which can be divided into four phases:

Low base, steady growth. Sales increased from 14.2 billion to 80.8 billion yuan, with an average annual compound growth rate of about 15%. The consumer market was gradually cultivated, and gold jewelry transitioned from a “luxury item” to a mass consumer good.

Growth accelerated significantly. Sales exceeded 120 billion yuan in 2010 and reached 304.1 billion yuan in 2021, a 1.4-fold increase over 11 years. In 2011, retail sales hit 183.7 billion yuan (year-on-year growth exceeding 45%), marking the peak growth rate for the industry. This was driven by rising household incomes, a surge in wedding demand, the prominence of gold’s investment attributes (rising gold prices), and the rise of e-commerce channels.

Growth slowed or even slightly declined. Sales were 301.4 billion yuan in 2022 (down 0.9% from 2021), 331.0 billion yuan in 2023 (up 9.8%), and 330.0 billion yuan in 2024 (a slight decrease of 0.3%). Affected by the lingering impact of the pandemic, the pace of economic recovery, gold price volatility, and slow recovery of consumption scenarios, the industry entered a stage of stock competition.

Return to high growth. Retail sales reached 373.6 billion yuan (a year-on-year increase of 13.21%), setting a new historical record. This indicates the industry quickly emerged from the adjustment period, driven by restored consumer confidence, gold price trends, holiday consumption (Spring Festival/wedding season), and product innovation (ancient method gold, cultural and creative jewelry).

Cumulative Year-on-Year (Purple Line): It was -3.45% in 1997, positive in most subsequent years. In 2020, impacted by the pandemic, it dropped to -4.7% (historical low), rebounded to 29.8% in 2021 (revenge spending), fell back to -4.1%, 13.3%, and -3.1% from 2022 to 2024, and rose to 12.8% in 2025, highly consistent with the retail sales trend.

Resident consumption upgrading is fundamental. Gold and jewelry possess both “consumption attributes (weddings/festivals)” and “investment attributes (hedging/anti-inflation)”, providing dual support for demand and strong long-term growth resilience for the industry.

The pandemic (2020) was the biggest disruption, directly causing declines in both retail sales and growth rates. The weak recovery from 2022 to 2024 was influenced by multiple factors including macroeconomic conditions, consumer willingness, and gold price volatility. The high growth in 2025 stemmed from economic recovery, restored consumer confidence, and product/channel innovation (live-streaming e-commerce, cultural and creative jewelry, etc.).