Editor’s Note

The diamond industry faces a pivotal moment as shifting consumer preferences and the rise of lab-grown alternatives challenge traditional market dynamics. While high-value auctions capture attention, underlying trends signal a need for adaptation across the supply chain.

A new generation of customers and synthetic gemstones are presenting suppliers with new challenges.

The diamond market is undergoing a transformation. Changes in the environment demand a rethink from producers and suppliers. While record sales (just in April, $71.2 million was achieved for diamond earrings at a Sotheby’s auction in Hong Kong) make international headlines, global demand for diamond jewelry fell for the first time in six years in 2015 to $79 billion due to the strong dollar and slowing growth in emerging markets like China.

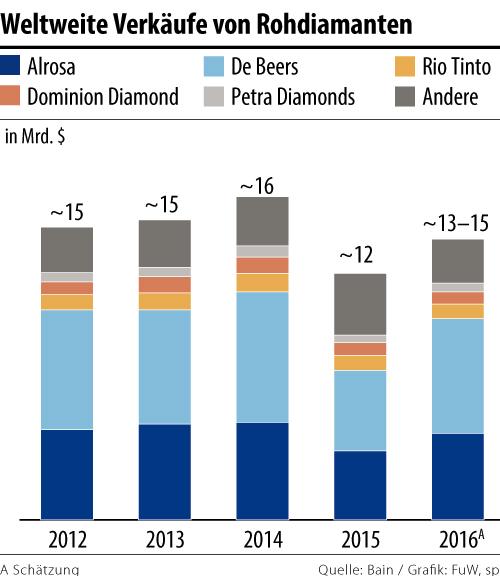

After the price of rough diamonds consequently fell by 15% in the same year, major suppliers like Alrosa and De Beers reduced their production volumes and increased their own inventories. The sale of rough diamonds subsequently decreased by 24%.

After the weak phase in 2015, the industry recovered last year. Prices stabilized, and diamond intermediaries and processors replenished their purchasing volumes. Consequently, sales increased by around 20% in the first half of 2016.

The US remained the growth engine of the diamond industry, with middle-income customers in particular driving rising profits for American jewelers. In China, however, travel restrictions to Hong Kong and Macau led to a decline in shopping tourism. This negatively impacted the local diamond business. Japan and Europe ultimately benefited from the decline in demand from China, recording increased purchases in euros and yen in 2015. Overall, rising incomes in emerging markets like India boosted diamond consumption.

Founded in 1888 in South Africa, the world’s largest diamond producer and trader, De Beers, based in Luxembourg, held a monopoly position for over a century. With the launch of the “A Diamond Is Forever” advertising campaign, the company, now led by Anglo American, established the diamond ring in 1948 as a symbol of (eternal) love. Since then, the market has changed dramatically.

Millennials, those born between 1980 and 2000, are the largest potential customer group since the baby boomers (their number in China, India, and the US was already estimated at 900 million in 2015). In 2016, they already invested $26 billion in diamond jewelry – more than any previous generation.

Nevertheless, they are causing headaches for suppliers. Because many prefer to invest in experiences rather than luxury products. And more and more are deciding against marriage. Therefore, the classic diamond ring is increasingly losing significance. When Millennials do decide on jewelry, they prefer cheaper gemstones like sapphires or rubies.

Manufacturers of synthetic diamonds also benefit from this: What took nature millions of years, they produce in the laboratory within a few weeks. While synthetic stones were previously used primarily in industry, they are now increasingly entering the jewelry market: in 2015, they already represented 2% of the global supply. The attractive price (synthetic diamonds are up to 40% cheaper) and the “ethically impeccable” and “local” production, which manufacturers like to emphasize, are well received by young customers.

Although the supply of synthetic diamonds will continue to increase in the future, diamond producers have recognized the problem. The Diamond Producers Association (DPA) launched its first advertising campaign in 2015 under the slogan “Real Is Rare.” This way, the integrity and reputation of natural diamonds are more strongly marketed by emphasizing their emotional advantages – and they are distinguished from synthetic stones as a symbol of lasting relationships.

Overall, however, the prognosis for the diamond market is good. According to a Bain study, the supply and demand for rough diamonds will balance out by 2019. Based on positive signals for the US economy and an increase in middle incomes in China and India, demand growth of between 2 and 5% per year is expected from 2020 onwards. Since more old mines will be closed than new ones opened by 2030, a production decline of up to 2% annually is projected. This will have a positive impact on the price in the coming years.