Editor’s Note

This analysis highlights a pivotal shift in the diamond market, where consumption upgrades and diversified purchase scenarios are redefining demand. The data points to a resilient market foundation, with growth increasingly driven by non-marriage occasions.

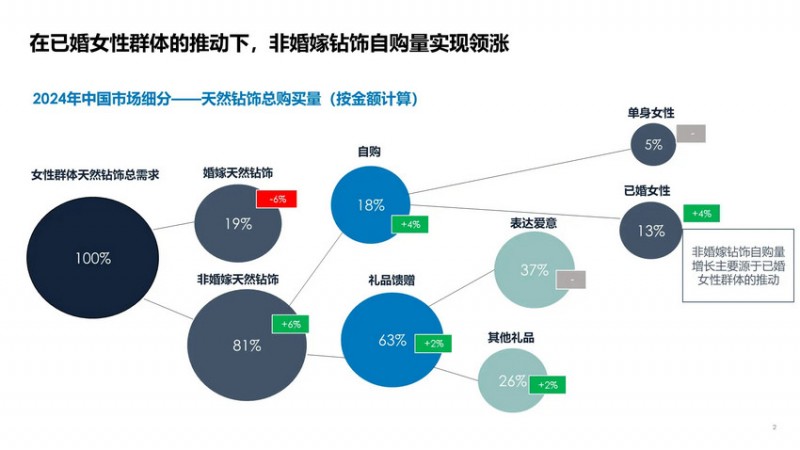

The report indicates that the value foundation of the natural diamond market remains solid, with a clear trend of consumption upgrade: the average price per piece increased by 1.8% against the trend, the average carat weight rose to 0.32 carats, and certified consumers’ demand for high-quality diamonds has strengthened. A more profound change is occurring in the consumption scenario domain: the share of non-marriage scenario consumption has reached 81%, achieving leapfrog growth from 52% in 2020, becoming the absolute market driver.

Among these, gift-giving and rewards account for 76% of non-marriage purchases, with holidays and anniversaries as the core scenarios; self-purchase demand driven by married women is rapidly leading the market, with the self-purchase ratio among women aged 30-45 reaching 54%. Notably, the share of romantic gift-giving scenarios remains stable at 37%, highlighting that the core value of diamonds as an emotional carrier remains unchanged.

Data paints a clear picture of the customer base: the share of Generation Z (aged 18-24) has surged to 10%, with the purchase rate rising from 3% in 2022 to 4% in 2024, and purchase intention for the next 12 months reaching 22%, ranking first among all age groups; consumers with a monthly income exceeding 10,000 yuan account for as high as 72%.

Generation X remains a key force, with a diamond ownership rate of 25%, accounting for nearly one-third of consumption value, and daily wear acceptance is significantly higher than the average level. Affluent groups with a household monthly income above 30,000 yuan constitute the value cornerstone, with per-piece spending 40% higher than the average, and future purchase intention is twice that of the overall consumer base, favoring non-marriage categories like necklaces and earrings.

The report reveals new purchase pathways: offline stores bear 58% of pre-sale consultations and 40% of actual purchases, confirming the irreplaceability of the physical experience; online channels are crucial in the research phase, with 51% of consumers obtaining information through social media, a proportion as high as 65% among married and first-tier city consumers.

Brand influence continues to strengthen, with branded diamond jewelry accounting for 98% of consumption value in 2024. Digital marketing shows significant effects: contributions from social media and live streaming platforms to sales increased by 9% and 4% respectively. Short videos have become the core information source for two-thirds of purchasers, with an average decision-making cycle from ad exposure to purchase of 29 weeks.

The report points out that China’s natural diamond market is undergoing a structural demand shift. The value connotation of natural diamonds is no longer confined to the “symbol of eternal love” but extends to a carrier for precious emotional bonds, personal milestone commemorations, and daily style expression. From the diverse purchase motivations of younger groups to the quality pursuit of affluent populations, and the daily expansion of consumption scenarios, natural diamonds are integrating into consumers’ lives in richer roles. As consumer groups evolve and demand upgrades, the potential of China’s natural diamond market will continue to be unleashed!