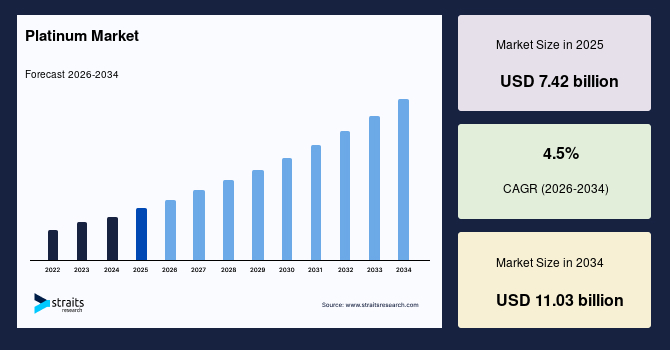

The global platinum market, valued at USD 7.42 billion in 2025, is projected to grow to USD 11.03 billion by 2034 at a CAGR of 4.5%, according to a new report. For jewelry buyers and supply-chain professionals, this signals sustained demand for platinum as a key material in rings, necklaces, and bridal collections, alongside its industrial uses. The report highlights shifts in sourcing, pricing, and regional production that directly impact procurement strategies for OEM/ODM partners and private-label brands.

Supply-chain impact

Platinum remains a critical material for jewelry manufacturing, particularly in high-end bridal and luxury collections. The market's growth, driven by automotive catalytic converters and emerging hydrogen fuel cell applications, may tighten supply for jewelry use. Buyers should monitor primary production from South Africa, Russia, and Zimbabwe, which dominate global output. Any disruption—from labor strikes to environmental regulations—could affect platinum availability and pricing for jewelry orders.

Regional sourcing dynamics

Asia Pacific held the largest market share at approximately 49% in 2021, driven by automotive giants in India, China, and Japan. This region is also a major hub for jewelry manufacturing and sourcing. Europe is expected to see the second-highest growth, with demand for diesel hybrid vehicles boosting platinum use. North America remains the third-largest market, with lower commodity prices creating investment opportunities. For jewelry importers, understanding regional production and regulatory shifts is key to optimizing sourcing from these areas.

What buyers should watch

Platinum prices have been volatile, declining from about USD 32,857.3 per kilogram in January 2020 to USD 18,904.2 in March 2020 due to the pandemic. While prices have stabilized, ongoing geopolitical and economic uncertainties may cause short-term fluctuations. Jewelry buyers should consider hedging strategies or locking in prices with suppliers. Additionally, the rise of hydrogen fuel cell vehicles could increase platinum demand, potentially raising costs for jewelry applications. Monitoring secondary platinum from recycling may offer alternative sourcing options.

Compliance and logistics signals

Stricter emission regulations, such as BS-VI in India and Euro standards in Europe, are driving platinum demand in automotive catalysts. This regulatory pressure may indirectly affect jewelry supply chains by competing for the same material. Buyers should ensure their suppliers comply with environmental and trade regulations, especially when sourcing from primary producers in South Africa or Russia. The report notes that secondary platinum from recycling is expected to grow fastest, offering a more sustainable and potentially cost-stable source for jewelry manufacturers.

China sourcing context

While the report does not specifically highlight China, the Asia Pacific region's dominance—including China's role as a major jewelry manufacturing and consuming market—underscores its importance. Chinese OEM/ODM suppliers may face increased competition for platinum from automotive and industrial sectors. Buyers working with Chinese partners should discuss platinum sourcing strategies, including potential use of recycled or alloyed forms, to manage costs and ensure supply chain stability.

Source: Read the original report | Published: June 03, 2026